Running a business comes with rules that must be followed. Whether simple or complex, staying in compliance with regulatory requirements takes effort. These rules affect how you handle operations, finances, employees, and customer data. Therefore, ignoring them can lead to serious problems over time.

Running a business comes with rules that must be followed. Whether simple or complex, staying in compliance with regulatory requirements takes effort. These rules affect how you handle operations, finances, employees, and customer data. Therefore, ignoring them can lead to serious problems over time.

Additionally, regulations can change without much notice. What worked last year might not be enough now. That’s why keeping up with updates is important. You want to stay ahead instead of fixing mistakes after they happen. Regular checks and clear systems make it easier to manage.

However, compliance is not only about avoiding penalties. It also helps build trust with customers, vendors, and business partners. When people know you follow the rules, they feel more confident working with you. That kind of trust can help you win more business and improve your reputation.

Building a compliance program takes planning, but it doesn’t have to be complicated. Start small and improve each part over time. Additionally, make sure your team understands the expectations. People can’t follow rules they don’t know about.

You’ll also benefit from using tools that track your progress. These tools save time and reduce errors. Therefore, technology can play a big role in making compliance more manageable.

A strong approach to compliance makes your business safer and more efficient. It supports growth and protects what you’ve built. By focusing on clear steps and consistent habits, you’ll stay prepared for whatever comes next.

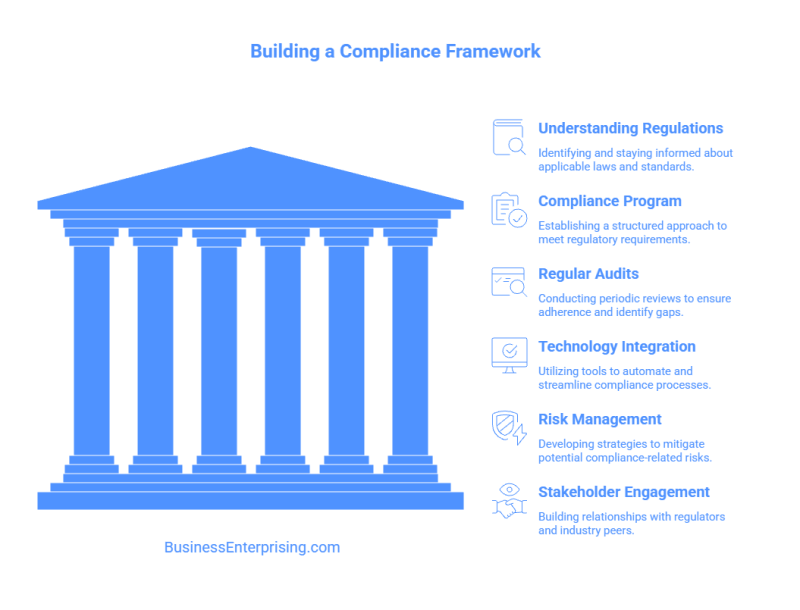

Understanding the Regulatory Landscape

Understanding the regulatory landscape is essential if you want to avoid costly mistakes. Every industry has rules that guide how business gets done. These rules may come from federal agencies, state laws, or local codes. Therefore, you need to stay informed about which ones apply to your operations.

Additionally, regulatory changes can happen often. Laws may shift based on new technologies, economic trends, or policy updates. If you don’t keep up, you risk penalties or forced corrections. Therefore, reviewing your compliance practices regularly can protect your business and reduce surprises.

You don’t need to be a legal expert, but you do need a system. Start by identifying the top regulations that impact your field. Then track any updates that affect those areas. This gives you a basic plan for staying in compliance with regulatory requirements.

Additionally, build good habits across your team. Everyone needs to understand the rules that relate to their roles. You can do this through regular training or by keeping documentation easy to access. When everyone knows the basics, mistakes happen less often.

Some businesses also work with outside professionals to stay on track. Accountants, legal advisors, and compliance consultants can help you check your work. These services often save time and money by catching problems early. However, they should support your process, not replace it.

Staying compliant is part of running a healthy business. It gives you more freedom to grow without distraction. When you understand the rules, you can focus more on progress and less on repair.

Establishing a Robust Compliance Program

Creating a strong compliance program starts with clarity. You need to know the rules, your risks, and how to manage both. A good program should reflect your specific business model, not a one-size-fits-all checklist. Therefore, begin by identifying the main regulations that apply to your operations.

Additionally, define roles and responsibilities clearly. Everyone should know what they’re expected to follow and report. Training is a key part of the process. However, it must be ongoing, not a one-time event. New hires, role changes, and policy updates all require fresh attention.

You’ll also want to document your policies in a simple and accessible format. This helps avoid confusion and makes it easier to spot gaps. Therefore, review your policies at least once a year to make sure they still reflect your current practices.

Monitoring and reporting are equally important. You need to track performance and correct issues before they grow. Automated systems can help, but human oversight still matters. Additionally, create a way for employees to report concerns without fear of backlash.

Some companies also perform internal audits or work with compliance professionals. These reviews can reveal weak points and improve results. If done regularly, they support long-term strength and reduce future risks.

Most importantly, your compliance program should match your values. If it’s only about checking boxes, it won’t work for long. When done right, it supports trust, efficiency, and staying in compliance with regulatory requirements.

Conducting Regular Compliance Audits

Conducting regular compliance audits helps you stay on top of your legal and operational responsibilities. These audits highlight what’s working and where problems may develop. Therefore, they play a key role in maintaining accountability and reducing risks over time.

Additionally, audits give you a clear view of your team’s actions. They reveal whether your internal controls are working as intended. If gaps appear, you can adjust your systems before those issues grow into larger problems. This proactive approach supports both stability and performance.

However, the value of an audit depends on preparation. Start by setting clear objectives and timelines. Then review policies, procedures, and documentation against current laws and standards. It’s also helpful to include interviews or spot checks to see how well policies are followed in real situations.

After the review, take time to document and share your findings. Additionally, assign follow-up actions with specific deadlines. This helps turn observations into real progress. Teams that track improvements after each audit tend to build better long-term habits.

Some businesses use outside auditors to bring fresh perspective. These audits often surface things internal staff might overlook. However, even internal reviews can be effective with the right structure and frequency.

Regular audits also show regulators and partners that your business takes compliance seriously. They demonstrate your commitment to staying in compliance with regulatory requirements. That credibility matters when you face inspections, grow into new markets, or deal with unexpected issues.

Leveraging Technology for Compliance Management

Technology can make compliance easier to manage across your business. Manual tracking takes time and leaves more room for error. However, with the right tools in place, you can automate routine tasks and reduce risk at the same time.

Many businesses now use software to manage documents, track deadlines, and run checks automatically. These tools give you clear records and alerts when something needs attention. Therefore, you spend less time chasing paperwork and more time fixing actual problems.

Additionally, digital platforms help you stay consistent. They apply the same rules every time, without relying on memory or guesswork. This keeps your team aligned and makes training simpler. You can also create logs that show what was done, when, and by whom.

Compliance software often includes dashboards or reports that give you real-time insight. You can see where issues might develop before they grow. Therefore, regular use of these tools helps you avoid surprises and stay ahead of audits.

Some tools also help with policy updates, reporting, or internal reviews. If your regulations change often, technology can keep your documents and procedures current. Additionally, you can grant access based on roles, keeping sensitive information protected.

By using the right tools, you make staying in compliance with regulatory requirements more reliable and less stressful. Technology won’t replace good judgment, but it will support your process. That support helps you move faster, make better decisions, and reduce overall risk.

Developing a Risk Management Framework

Developing a risk management framework helps you prepare for problems before they cause damage. Every business faces different types of risk. These may involve finance, operations, reputation, or legal exposure. Therefore, building a structure to identify and respond to risk is essential.

Start by listing the most common threats to your business. Then assess how likely they are and what they could cost you. This step helps you decide which risks need more attention. Additionally, clear planning allows your team to respond faster and more effectively.

Once you’ve defined the risks, assign responsibility for monitoring and response. Each risk should have an owner who tracks it over time. However, risk management is not a one-person task. It requires cross-team cooperation and regular reviews.

You should also build policies to reduce exposure. These might include internal controls, backup systems, or training programs. Additionally, set up alerts or early warning signs that show when a risk is starting to build.

Some risks will require outside help, especially those involving compliance or legal matters. Therefore, having advisors ready to support your response can save time and money. It also helps you stay focused when pressure is high.

A strong risk framework supports long-term growth. It helps protect your brand, your team, and your customers. Most importantly, it supports your efforts in staying in compliance with regulatory requirements. When risk is managed well, your business is more stable and easier to grow.

Engaging with Regulatory Authorities and Industry Peers

Building relationships with regulatory authorities and peers can support your long-term success. These relationships offer useful insight and shared experience. Therefore, staying connected helps you keep pace with changing expectations.

Additionally, direct communication with regulators can reduce confusion. When you ask questions early, you avoid missteps later. Most agencies welcome proactive contact and provide resources for clarification. However, the quality of the relationship depends on mutual respect and timely responses.

Industry peers are another important source of knowledge. Many face similar challenges and can offer advice based on lived experience. Therefore, joining industry groups or trade associations gives you access to discussions, updates, and collective action.

You can also gain value by attending forums, roundtables, or compliance workshops. These events often highlight trends or policy shifts before they become formal rules. Additionally, they give you a space to share concerns and propose solutions.

Some industries benefit from self-regulatory groups. These groups often work closely with agencies to raise standards across the board. Participating in them shows commitment and builds trust with both customers and regulators.

By staying visible and involved, you demonstrate accountability and build goodwill. These actions support your reputation and open doors when help is needed. Most importantly, this engagement supports staying in compliance with regulatory requirements.

When you stay informed and collaborative, you make smarter choices. Your policies will reflect current standards, and your team will feel better supported. Over time, this approach leads to fewer surprises and stronger results.

Conclusion

Regulatory compliance is not something you can ignore or put off. It affects every part of your business, from operations to reputation. Therefore, building a system that supports compliance will help you work with fewer disruptions and more confidence.

Additionally, compliance is not a one-time task. It requires ongoing attention, clear communication, and smart planning. You need tools, training, and regular reviews to keep everything in check. These efforts help you stay ahead of problems before they turn into fines or delays.

However, the benefits of good compliance go beyond risk reduction. They also include stronger relationships with customers, regulators, and business partners. When people trust that you follow the rules, they are more likely to work with you.

Therefore, focus on small steps that build over time. Review your policies, improve your tracking, and involve your team in the process. Ask questions when needed and keep your documents up to date.

Additionally, keep learning from your peers and industry groups. Their insight may help you avoid mistakes or spot new requirements early. Sharing knowledge helps everyone move forward.

You don’t need perfection to make progress. What matters is consistency and a willingness to adjust. With the right structure, you’ll improve performance across the board. Most importantly, you’ll strengthen your position by staying in compliance with regulatory requirements. Clear systems, good habits, and honest effort make a difference. When you take compliance seriously, you protect your business and open more doors for growth.