Starting a business is exciting, but handling the legal steps for startups is essential for success. From choosing a structure to managing taxes, legal compliance is key. Taking the right steps protects your business and sets the foundation for growth. Without proper planning, you risk complications that could slow your progress.

Starting a business is exciting, but handling the legal steps for startups is essential for success. From choosing a structure to managing taxes, legal compliance is key. Taking the right steps protects your business and sets the foundation for growth. Without proper planning, you risk complications that could slow your progress.

Understanding legal requirements helps you navigate challenges and avoid mistakes. Whether registering your business, drafting contracts, or protecting intellectual property, each step supports your operations. By staying informed and proactive, you can focus on building your business with confidence.

Legal steps for startups may seem complex, but they’re manageable with the right approach. By addressing these early, you reduce risks and create opportunities for long-term success. Starting your business on solid legal ground ensures you’re ready to grow and thrive.

Choosing the Right Business Structure

Choosing the right business structure is one of the first legal steps for startups. Each structure offers unique benefits and challenges. Common options include sole proprietorships, LLCs, corporations, and partnerships. Sole proprietorships are simple and cost-effective but leave you personally liable for business debts. LLCs offer limited liability protection while keeping operations relatively simple.

The right structure depends on your goals, industry, and risk tolerance. If you plan to scale quickly or seek outside investors, a corporation may be the best fit. Corporations separate your personal assets from business liabilities and make raising funds easier. Partnerships allow you to share responsibilities and profits but require clear agreements to avoid disputes.

Tax and liability implications are critical when making this decision. Sole proprietors report income through personal taxes, but they lack protection from liability. LLCs and corporations offer liability shields, but they involve more regulatory requirements. Corporations face double taxation unless structured as an S-Corp. Considering these factors is essential when deciding on the right structure for your startup. Taking time to evaluate your options helps you build a strong foundation for future success.

Registering Your Business

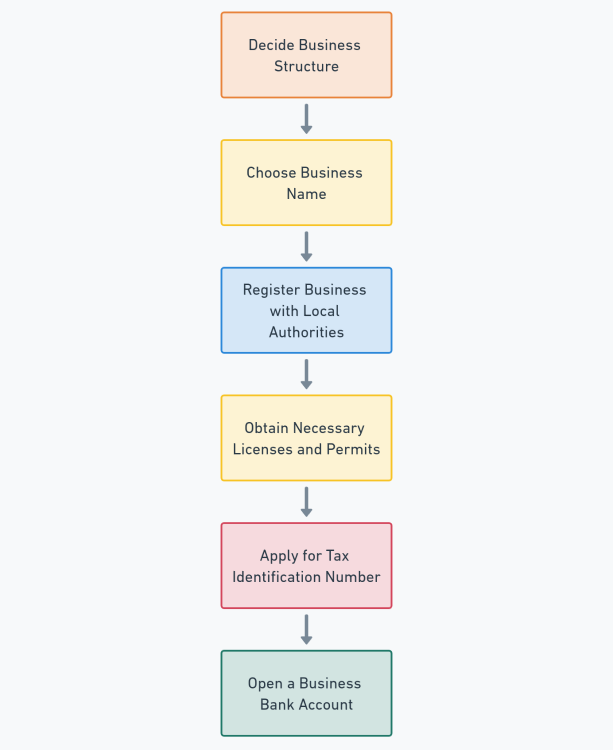

Registering your business is one of the most important legal steps for startups. It begins with choosing a unique business name. After selecting a name, you need to check for its availability in your state or region. Registering the name protects your brand and also prevents others from using it.

Registration requirements vary depending on your business location and activities. Local registration may involve obtaining a business license or permit from your city or county. State registration typically includes filing formation documents, such as articles of incorporation or an LLC application. At the federal level, you may need an Employer Identification Number (EIN) for tax purposes or other permits if your business is regulated by federal laws.

Compliance with jurisdiction-specific regulations is essential to avoid fines or legal complications. Operating without the required registrations or permits can delay your progress and harm your reputation. Understanding these legal steps for startups ensures you meet all requirements and start your business on a solid legal foundation. Taking the time to register correctly helps you focus on growth with peace of mind.

Drafting Essential Contracts

Drafting essential contracts is a critical part of the legal steps for startups. Contracts provide clarity and protection in business relationships. Common agreements include partnership contracts, client agreements, and non-disclosure agreements (NDAs). Partnership agreements outline roles, responsibilities, and profit-sharing among co-founders. Client contracts specify deliverables, payment terms, and timelines to prevent disputes. NDAs protect sensitive business information from being shared or misused.

Including key clauses in your contracts safeguards your business interests. Clear definitions of terms, confidentiality obligations, and dispute resolution methods help avoid misunderstandings. Termination clauses specify conditions under which a contract can end, providing flexibility if circumstances change. Indemnification clauses protect you from liability in specific situations. These provisions are essential for reducing risks and establishing trust with stakeholders.

Engaging legal counsel ensures your contracts are thorough and legally enforceable. Lawyers can identify potential risks, customize templates, and ensure compliance with local laws. This professional guidance is invaluable when navigating the legal steps for startups. Well-drafted contracts set a strong foundation for growth and prevent costly legal issues down the road. Investing in quality agreements protects your business and strengthens your relationships.

Protecting Intellectual Property

Protecting intellectual property is an essential part of the legal steps for startups. Intellectual property includes trademarks, copyrights, and patents, each serving a specific purpose. Trademarks protect your brand name, logo, or slogan, ensuring no one else can use them. Copyrights cover original works like text, images, and software, granting you control over their use. Patents secure your inventions, giving you exclusive rights to produce and sell them.

Registering intellectual property strengthens your legal protection and also helps you enforce your rights. To trademark a name or logo, file an application with the appropriate authority. Copyright registration is often automatic but can be formalized for stronger protection. Patents require detailed applications outlining the uniqueness of your invention. Regular monitoring and enforcement prevent unauthorized use and help maintain your competitive advantage.

Avoiding infringement is equally important for startups. Conduct thorough research to ensure your brand, products, or content don’t violate existing intellectual property. Using clearance searches and legal advice reduces risks of disputes. Understanding these legal steps for startups allows you to safeguard your assets and operate confidently. Protecting intellectual property ensures your ideas and innovations remain secure, supporting long-term growth as well as success.

Complying with Employment Laws

Complying with employment laws is a critical step in the legal steps for startups. When hiring employees or contractors, you need to meet key legal requirements. These include verifying work eligibility, classifying workers correctly, and adhering to minimum wage and overtime laws. Misclassifying an employee as a contractor can lead to fines or disputes.

Understanding employee rights and contracts helps you build a compliant workplace. Employment contracts should clearly outline job roles, compensation, and also termination terms. Providing benefits, such as health insurance or leave, may be legally required depending on your location and employee count. Transparent policies ensure fairness and help you avoid misunderstandings.

Common workplace mistakes, such as failing to document policies or ignoring anti-discrimination laws, can result in legal challenges. Creating clear workplace policies and training your team on compliance reduces these risks. Following these legal steps for startups helps you establish a strong and lawful foundation for your business. By respecting employment laws, you create a safe and professional environment that supports your team as well as protects your business.

Understanding Tax Obligations

Understanding tax obligations is a key part of the legal steps for startups. Taxes exist at local, state, and federal levels, each with unique requirements. Local taxes may include business licenses or specific fees, while state taxes often involve sales tax and income tax filings. Federal taxes cover employment taxes, corporate income taxes, and also other obligations based on your business structure.

Obtaining an Employer Identification Number (EIN) is a necessary step for most businesses. This number is required for filing taxes, opening a business bank account, and hiring employees. You can apply for an EIN online through the IRS, and it also simplifies your tax filings. Staying tax-compliant involves understanding deadlines, filing forms accurately, and paying taxes on time.

Keeping accurate financial and tax records is essential for managing your startup. Records should include receipts, invoices, as well as payroll information to support tax filings and audits. Organized records help you track expenses, identify deductions, and avoid penalties. Incorporating these legal steps for startups into your operations builds a strong foundation and reduces risks. Proactively managing taxes helps you focus on growing your business with confidence.

Conclusion

Following the right legal steps for startups lays a solid foundation for your business. From choosing a structure to managing taxes, every step matters. Addressing these requirements helps you avoid legal complications and focus on growth. Staying compliant also builds trust with customers, employees, and also investors.

Understanding contracts, employment laws, as well as intellectual property ensures you protect your business and its assets. These steps reduce risks and strengthen your operations. By staying organized and seeking professional advice when needed, you prepare your startup for long-term success. Taking time to handle these details now saves you from potential challenges later.

Starting a business involves navigating many legal responsibilities. Proactively managing these legal steps for startups helps you operate with confidence and focus on achieving your goals.