Starting your own business is an exciting endeavor. However, it requires careful planning and execution. By following these 10 steps to launching a startup, you can turn your innovative idea into a successful venture. This guide will walk you through each phase, providing practical advice to help you navigate the process. From developing a solid business plan to building your brand, we’ll cover the essential elements to set you on the path to success. Let’s explore these steps together and lay the groundwork for your entrepreneurial journey. Below are 10 steps to launching a startup.

Starting your own business is an exciting endeavor. However, it requires careful planning and execution. By following these 10 steps to launching a startup, you can turn your innovative idea into a successful venture. This guide will walk you through each phase, providing practical advice to help you navigate the process. From developing a solid business plan to building your brand, we’ll cover the essential elements to set you on the path to success. Let’s explore these steps together and lay the groundwork for your entrepreneurial journey. Below are 10 steps to launching a startup.

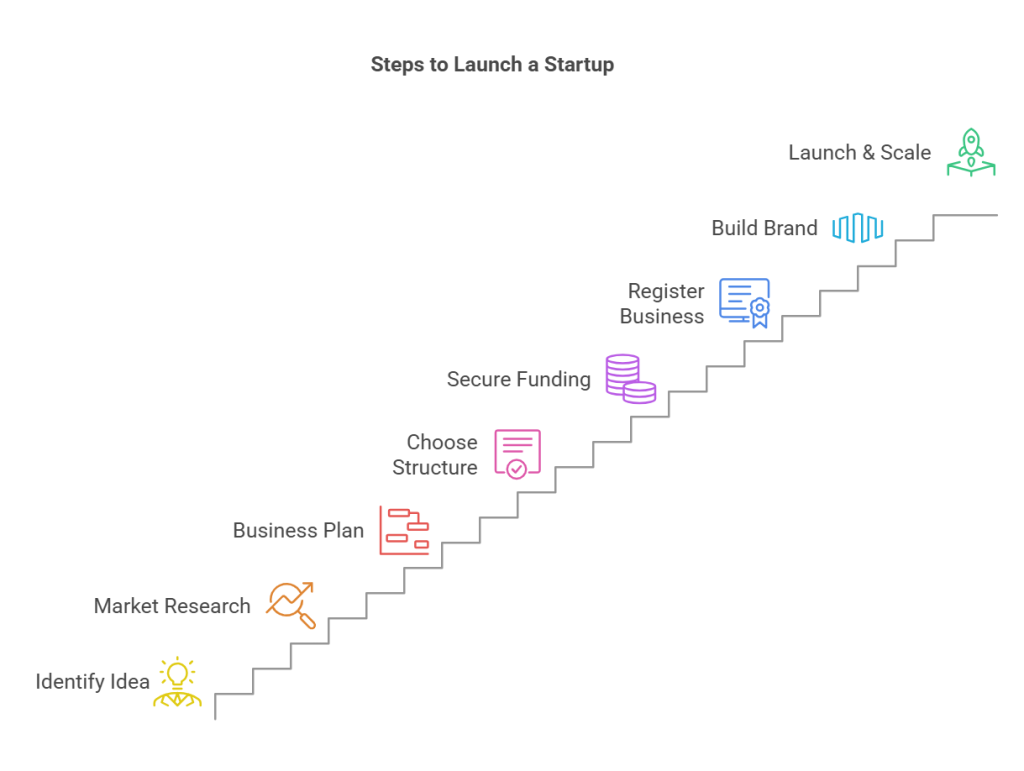

1. Identify a Profitable Business Idea

Among the 10 steps to launching a startup is identifying a profitable business idea is a fundamental step in the process of launching a startup. To begin, focus on problems that many people face. A successful business often provides solutions to common issues, making daily life easier or more efficient. For instance, consider how certain apps have simplified transportation or food delivery.

Next, assess current market trends. By staying informed about what’s gaining popularity, you can align your idea with consumer interests. This approach increases the likelihood of your business resonating with potential customers. However, it’s essential to distinguish between fleeting fads and sustainable trends to ensure long-term viability.

Additionally, identify gaps in the market. Look for areas where demand exceeds supply or where existing products lack certain features. By addressing these unmet needs, your business can stand out and attract a dedicated customer base. Engaging with potential customers through surveys or interviews can provide valuable insights into these gaps.

Furthermore, consider your personal strengths and passions. Aligning your business idea with what you excel at and enjoy can lead to greater commitment and resilience. This alignment not only enhances your satisfaction but also increases the chances of your startup’s success.

In conclusion, a profitable business idea emerges from solving common problems, leveraging market trends, filling unmet needs, and aligning with your strengths. By carefully evaluating these factors, you can develop a concept that lays a strong foundation for your startup’s success.

2. Conduct Market Research

One of the most important aspects of the 10 steps to launching a startup is conducting thorough market research is a key step in the process of launching a startup. Begin by validating the demand for your product or service. Engage directly with potential customers through surveys, interviews, or focus groups to gather insights into their needs and preferences. This direct engagement helps confirm that there is a genuine market need for your offering.

Next, analyze your competitors to understand their strengths and weaknesses. By examining their products, pricing, and customer feedback, you can identify areas where your startup can offer a distinct advantage. This analysis not only highlights opportunities but also informs your strategy to differentiate your business in the market.

Additionally, it’s essential to understand your target audience deeply. Develop detailed profiles that encompass demographics, behaviors, and purchasing patterns. This understanding enables you to tailor your marketing efforts effectively, ensuring your message resonates with those most likely to become customers.

By conducting comprehensive market research, you lay a solid foundation for your startup’s success. This approach ensures that your business decisions are informed by real-world data and insights.

3. Develop a Solid Business Plan

Developing a solid business plan is a key step in the process of launching a startup. Begin by clearly defining your mission statement, which articulates your company’s purpose and core values. This statement guides your strategic decisions and communicates your vision to stakeholders.

Next, establish specific, measurable goals that align with your mission. These objectives provide direction and benchmarks for success. For example, you might aim to achieve a certain revenue target within the first year. Setting clear goals helps you focus your efforts and track progress.

Additionally, outline your revenue model to detail how your business will generate income. Consider various streams, such as product sales, service fees, or subscription plans. Understanding your revenue model is essential for financial planning and attracting investors.

Furthermore, develop an operational strategy that describes the day-to-day functions of your business. This includes processes for production, delivery, and quality control. A well-defined operational plan ensures that your business runs efficiently and effectively.

By crafting a comprehensive business plan, you create a roadmap that guides your startup toward its goals. This plan not only clarifies your strategy but also serves as a valuable tool for communicating your vision to potential investors and partners.

4. Choose a Business Structure

Selecting the appropriate legal structure is a key step in the process of launching a startup. Your choice impacts taxes, liability, and operational complexity. The main options include sole proprietorship, limited liability company (LLC), and corporation.

A sole proprietorship is the simplest form, where you and the business are the same legal entity. This simplicity means you have complete control. However, it also means personal liability for business debts. Therefore, if your business faces legal issues, your personal assets are at risk.

An LLC offers a balance between simplicity and protection. It provides limited liability, separating your personal assets from business obligations. Additionally, LLCs offer flexibility in taxation, allowing profits to pass through to your personal tax return. However, they require more paperwork and fees than a sole proprietorship.

Corporations, such as C-corps and S-corps, are more complex structures. They offer strong liability protection and can raise capital through stock issuance. However, they are subject to stricter regulations and potential double taxation, especially C-corps. Therefore, if you plan to seek significant investment, a corporation might be suitable.

Consider your business goals, risk tolerance, and tax implications when choosing a structure. Consulting with legal and financial advisors can provide personalized guidance. By carefully selecting the right entity, you set a solid foundation for your startup’s success.

5. Secure Funding and Financial Planning

Securing funding and establishing a solid financial plan are key steps in the process of launching a startup. Begin by evaluating bootstrapping, which involves using your personal savings or funds from friends and family. This approach allows you to maintain full control over your business. However, it also means bearing all financial risks personally.

Alternatively, consider seeking investors such as angel investors or venture capitalists. Angel investors are individuals who provide capital in exchange for equity or convertible debt. Venture capitalists are firms that invest in startups with high growth potential. While these options can provide substantial funding, they often require giving up a portion of ownership and decision-making control.

Additionally, explore grants offered by government agencies, private foundations, or corporations. Grants provide funds that do not require repayment, making them an attractive option. However, they are highly competitive and often come with specific requirements and conditions.

Furthermore, small business loans from banks or online lenders can be a viable option. These loans require repayment with interest but allow you to retain full ownership of your company. It’s important to have a strong credit history and a solid business plan to qualify.

By carefully considering these funding options and developing a comprehensive financial plan, you can secure the necessary resources to launch and grow your startup successfully. Each option has its advantages and trade-offs, so align your choice with your business goals and risk tolerance.

6. Register Your Business and Obtain Licenses

Registering your business and obtaining the necessary licenses are key steps in the process of launching a startup. First, choose a unique business name and register it with your state’s Secretary of State office. This registration establishes your business as a legal entity. Additionally, if you plan to operate under a different name, file a “Doing Business As” (DBA) name.

Next, apply for an Employer Identification Number (EIN) through the IRS. This federal tax ID is essential for tax filings and opening a business bank account. However, sole proprietors without employees may use their Social Security Number instead.

After obtaining your EIN, register your business with state and local agencies. Requirements vary by location and industry, so consult your state’s business bureau for specific guidelines. Additionally, some businesses may need to register for state taxes or workers’ compensation insurance.

Furthermore, determine which licenses and permits your business needs. These can range from general business licenses to industry-specific permits. For example, restaurants often require health department permits. Therefore, check with local authorities to identify applicable requirements.

By completing these steps, you ensure your startup operates legally and is well-prepared for success. Compliance with regulations not only avoids legal issues but also builds trust with customers and partners.

7. Build Your Brand and Online Presence

Building a strong brand and establishing an online presence are key steps in the process of launching a startup. Begin by defining your brand identity, which includes your mission, values, and unique selling points. This foundation guides your visual elements, such as logo design and color schemes, ensuring consistency across all platforms.

Next, create a professional website that serves as your business’s digital home. Your website should clearly communicate who you are, what you offer, and how customers can engage with you. Additionally, optimize it for mobile devices and search engines to enhance accessibility and visibility.

Furthermore, establish social media channels on platforms where your target audience is active. Regularly share content that reflects your brand’s voice and values, fostering engagement and building community. However, avoid spreading yourself too thin; focus on platforms that align with your audience’s preferences.

By thoughtfully developing your brand identity, designing an informative website, and engaging on relevant social media channels, you create a cohesive and compelling online presence. This approach not only attracts potential customers but also builds trust and loyalty, setting the stage for your startup’s success.

8. Develop Your Product or Service

Developing your product or service is a key step in the process of launching a startup. Begin by creating a prototype that embodies your concept. This initial model allows you to explore design elements and functionality. Additionally, it serves as a tangible representation of your idea, facilitating further development.

Once your prototype is ready, conduct thorough testing to identify strengths and weaknesses. Gathering feedback during this phase is essential. By observing how users interact with your product, you can pinpoint areas needing improvement. This iterative process ensures that your offering aligns with user expectations.

After testing, refine your product based on the insights gained. Implement necessary adjustments to enhance usability and performance. However, remain open to ongoing feedback, as continuous improvement is vital. By embracing this cycle of prototyping, testing, and refining, you increase the likelihood of delivering a product that resonates with your target audience.

Incorporating customer feedback throughout development not only improves your product but also fosters trust with your audience. Engaging users in this manner demonstrates your commitment to meeting their needs. Therefore, prioritize open communication and be willing to adapt. This approach lays a strong foundation for your startup’s success.

9. Implement a Marketing and Sales Strategy

Implementing an effective marketing and sales strategy is a key step in the process of launching a startup. Begin by optimizing your website for search engines (SEO) to increase visibility. By incorporating relevant keywords and creating quality content, you can attract organic traffic. Additionally, ensure your site is user-friendly to enhance visitor engagement.

Next, consider investing in targeted advertising campaigns. Platforms like Google Ads and social media channels allow you to reach specific demographics. By analyzing performance metrics, you can adjust your approach to maximize return on investment. However, monitor your budget closely to avoid overspending.

Networking also plays a significant role in customer acquisition. Attend industry events, join professional groups, and engage in online forums to build relationships. These connections can lead to referrals and partnerships, expanding your customer base. Therefore, allocate time regularly for networking activities.

Furthermore, develop a compelling value proposition that clearly communicates the benefits of your product or service. This message should resonate with your target audience and differentiate you from competitors. By understanding your customers’ needs, you can tailor your offerings to meet their expectations.

By integrating SEO, targeted advertising, and strategic networking, you create a comprehensive approach to attract and convert customers. This multifaceted strategy not only drives sales but also fosters brand loyalty, setting the foundation for your startup’s success. Out of the 10 steps to launching a startup, marketing should not be overlooked.

10. Launch and Scale Your Business

The last of the 10 steps to launching a startup is execution. Executing your go-to-market strategy is a key step in the process of launching a startup. Begin by introducing your product or service to your target audience through the channels you’ve identified. This may include online platforms, physical locations, or a combination of both. Ensure that your messaging aligns with your brand identity and resonates with potential customers.

Next, actively track your business’s performance using key metrics such as sales figures, customer acquisition costs, and website traffic. Regularly monitoring these indicators allows you to assess the effectiveness of your strategy. Additionally, gather customer feedback to gain insights into their experiences and satisfaction levels.

Based on the data collected, identify areas for improvement and implement necessary adjustments to optimize growth. This may involve refining your marketing tactics, enhancing your product features, or exploring new distribution channels. By remaining adaptable and responsive to market dynamics, you position your startup for sustained success.

Scaling your business requires careful planning and resource management. Consider strategies such as expanding your product line, entering new markets, or increasing production capacity. However, ensure that growth initiatives align with your overall business objectives and that you have the infrastructure to support them.

By diligently executing your go-to-market strategy, monitoring performance, and optimizing for growth, you lay a strong foundation for your startup’s success. This proactive approach enables you to navigate challenges effectively and capitalize on opportunities as they arise.

Conclusion

Embarking on the journey of launching a startup involves a series of deliberate steps. By identifying a profitable business idea, you lay the foundation for your venture. Conducting thorough market research validates demand and informs your strategy. Developing a solid business plan outlines your mission, goals, and operational approach.

Choosing the appropriate business structure ensures legal and financial alignment. Securing funding and meticulous financial planning provide the necessary resources for growth. Registering your business and obtaining required licenses ensure compliance with regulations.

Building a strong brand and establishing an online presence enhance visibility and customer engagement. Developing your product or service through prototyping and testing ensures market fit. Implementing a targeted marketing and sales strategy attracts and converts customers.

Finally, executing your go-to-market strategy, monitoring performance, and optimizing operations facilitate scaling your business. By following these 10 steps to launching a startup, you position your venture for success in a competitive landscape.