Running a business requires constant problem-solving and adaptability. From managing finances to attracting customers, each challenge demands attention. However, identifying the most common business challenges early can help you find effective solutions before they disrupt operations. Taking a proactive approach allows you to stay ahead of potential setbacks.

Running a business requires constant problem-solving and adaptability. From managing finances to attracting customers, each challenge demands attention. However, identifying the most common business challenges early can help you find effective solutions before they disrupt operations. Taking a proactive approach allows you to stay ahead of potential setbacks.

Competition, customer expectations, and economic changes create ongoing pressure. Additionally, balancing growth while maintaining quality can be difficult. Technology, hiring, and financial management all play a role in long-term success. However, recognizing patterns in these challenges can help you develop better strategies. Small adjustments to processes and priorities can make a big difference over time.

Adapting to change is necessary for business growth. Relying on outdated methods limits progress and slows success. However, focusing on efficiency and customer needs helps keep your business relevant. Streamlining operations and improving internal systems can create better outcomes. Additionally, investing in strong relationships with customers and employees can provide long-term stability.

Each business faces unique challenges, but many obstacles are avoidable. By learning from common difficulties, you can strengthen your business and improve decision-making. With the right approach, overcoming challenges becomes an opportunity for growth. Staying flexible, informed, and prepared allows your business to succeed despite unexpected changes.

Client Acquisition & Retention

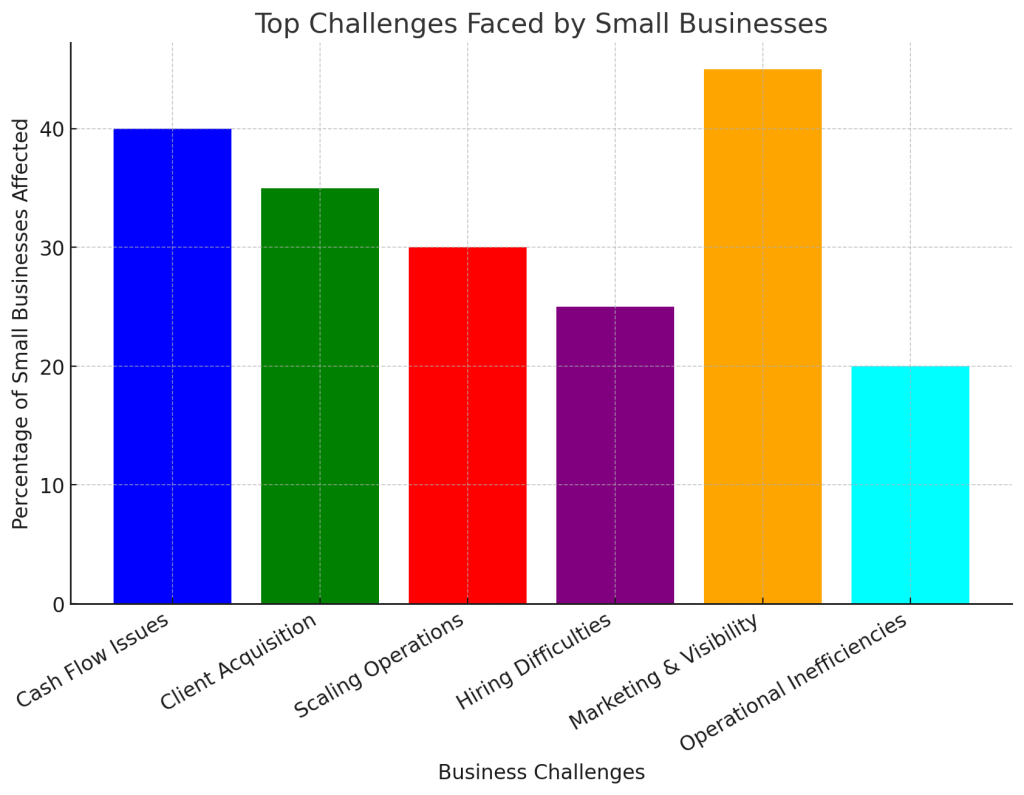

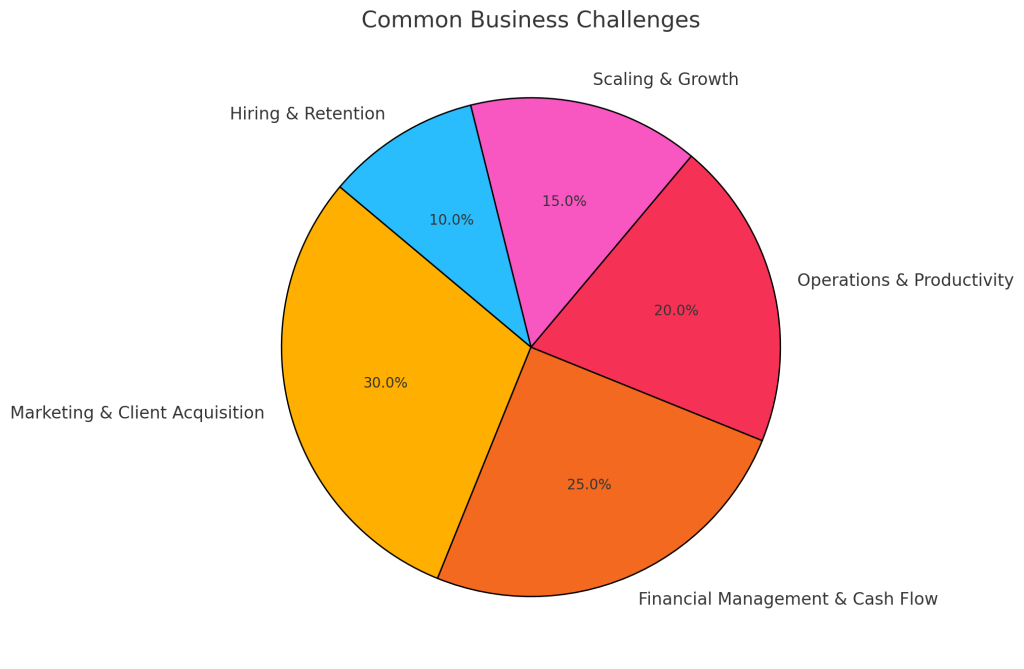

Attracting and retaining customers is among the most common business challenges. Many small businesses struggle to stand out in crowded markets, often due to limited marketing budgets and ineffective strategies. This can lead to poor sales conversion rates and hinder growth.

To overcome these obstacles, it’s essential to understand your target audience thoroughly. Conducting market research can provide insights into customer preferences and behaviors, allowing you to tailor your offerings accordingly. Additionally, building a strong online presence is crucial. A professional, user-friendly website optimized for search engines can increase visibility and attract potential customers. Engaging with audiences on social media platforms further amplifies your reach and fosters community.

Implementing cost-effective marketing strategies can also make a significant difference. Utilizing email marketing to communicate with existing customers keeps them informed about new products or promotions, encouraging repeat business. Offering exceptional customer service enhances satisfaction and loyalty, prompting positive word-of-mouth referrals. Moreover, establishing referral programs incentivizes current customers to introduce your business to others, expanding your client base without substantial financial investment.

Improving sales conversion rates involves analyzing and refining your sales process. Identifying bottlenecks or areas where potential customers lose interest allows you to make necessary adjustments. Providing clear value propositions and addressing customer pain points directly can persuade prospects to choose your products or services over competitors. Regularly seeking and acting upon customer feedback ensures your offerings align with market demands, enhancing overall satisfaction and retention.

By focusing on these strategies, small businesses can navigate the challenges of client acquisition and retention more effectively, leading to sustained growth and success.

Limited Marketing & Online Presence

Limited marketing resources and an inconsistent online presence are among the most common business challenges. These issues often lead to low search engine rankings, minimal social media engagement, and a heavy reliance on paid advertising. To address these challenges, consider implementing a multifaceted approach.

First, focus on enhancing your website’s search engine optimization (SEO). Conduct thorough keyword research to understand what your target audience is searching for. Incorporate these keywords naturally into your website content, meta descriptions, and titles. Additionally, ensure your website is mobile-friendly and has fast load times, as these factors significantly impact search rankings.

Next, develop a consistent and engaging social media strategy. Regularly post content that resonates with your audience, such as informative articles, behind-the-scenes glimpses, or customer testimonials. Engage with your followers by responding to comments and messages promptly. Utilizing scheduling tools can help maintain a steady online presence without overwhelming your team.

Consistency in branding and messaging across all platforms is also crucial. Ensure that your brand’s voice, colors, and logos are uniform across your website, social media profiles, and marketing materials. This uniformity helps build brand recognition and trust among your audience.

While paid advertising can drive immediate traffic, it’s essential to build organic lead generation channels. Creating valuable content, such as blog posts or videos, can attract visitors to your site over time. Encourage satisfied customers to leave reviews and refer others, leveraging word-of-mouth as a powerful marketing tool.

By implementing these strategies, you can enhance your online presence, engage more effectively with your audience, and reduce dependence on paid advertising.

Cash Flow & Financial Management

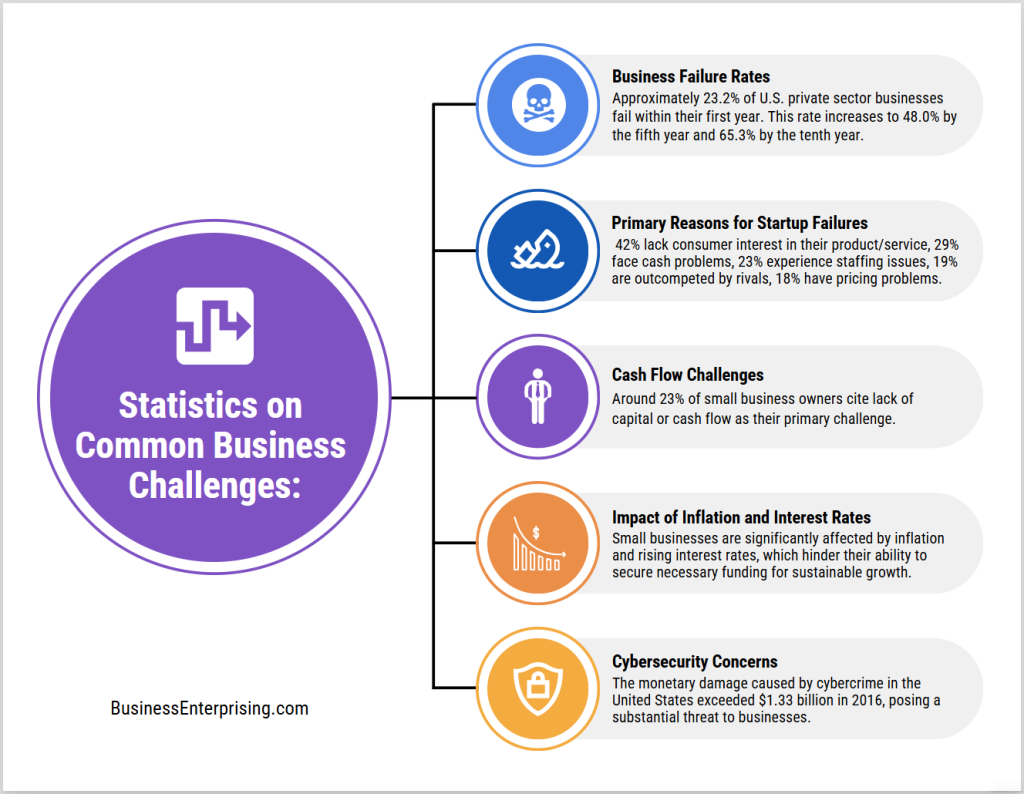

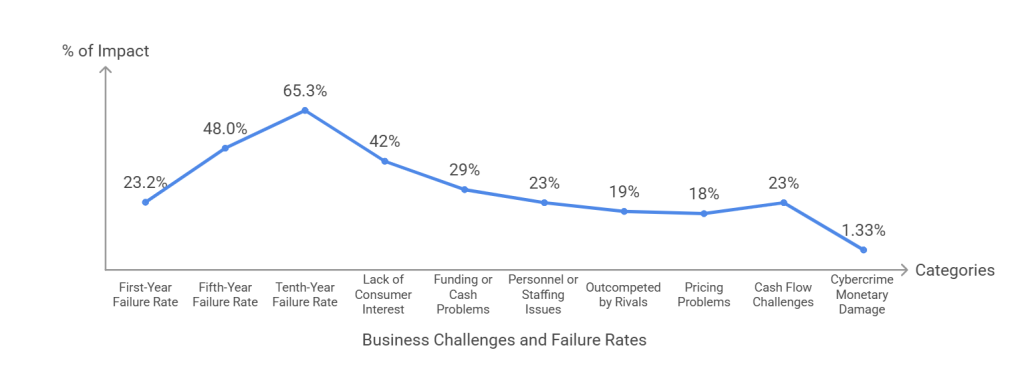

Managing cash flow and financial stability ranks among the most common business challenges. Irregular cash flow, high operational costs, and low profit margins can hinder growth. Additionally, managing debt and securing funding pose significant concerns. Pricing products or services competitively while maintaining profitability adds to these complexities.

To address irregular or insufficient cash flow, consider implementing effective expense management. Review your expenses regularly to identify and eliminate unnecessary costs. Negotiating better terms with suppliers can also improve your cash flow. Additionally, offering discounts for early payments can encourage customers to pay promptly, enhancing your cash inflow.

High operational costs and low profit margins require a strategic approach. Streamlining operations can reduce expenses, thereby increasing profit margins. Investing in technology can automate repetitive tasks, leading to cost savings. Regularly reviewing your pricing strategy ensures that your prices reflect market conditions and cover your costs adequately.

Managing debt and securing funding are critical aspects of financial management. Maintaining a healthy level of debt is essential to avoid overburdening your finances. Exploring options like debt consolidation can lower monthly payments, easing cash flow pressures. Establishing a business line of credit provides a safety net for unforeseen expenses, offering flexibility in financial planning.

Pricing products or services competitively while remaining profitable involves understanding your market and costs. Conducting market research helps in setting prices that attract customers without compromising profits. Regularly assessing your cost structure ensures that your pricing remains sustainable. Offering value-added services can justify pricing adjustments, enhancing customer satisfaction and loyalty.

By focusing on these strategies, you can navigate financial challenges effectively, leading to improved cash flow and business growth.

Time Management & Productivity

Managing time and maintaining productivity are among the most common business challenges. As a small business owner, you often juggle multiple roles, from sales and marketing to operations and finance. This multitasking can lead to burnout and decreased efficiency. To address this, it’s essential to prioritize tasks and delegate responsibilities effectively. Identifying critical activities that directly impact your business’s growth allows you to focus your energy where it matters most. Additionally, delegating less critical tasks to capable team members or outsourcing can free up valuable time, enabling you to concentrate on strategic decision-making.

However, delegating tasks can be challenging if you lack reliable staff. Building a trustworthy team requires investing in hiring and training processes. Clearly defining roles and responsibilities ensures that team members understand expectations and can perform their duties effectively. Regular communication and feedback foster a supportive work environment, enhancing overall productivity. Moreover, offering professional development opportunities can improve employee retention and reliability, reducing the burden on you as the business owner.

Inefficient systems and processes can also hinder productivity. Implementing streamlined workflows and utilizing technology can significantly improve efficiency. For instance, adopting project management tools helps in organizing tasks and tracking progress. Automating repetitive tasks reduces manual workload, allowing you and your team to focus on more strategic activities. Regularly reviewing and refining your business processes ensures they remain effective and aligned with your goals. By addressing these areas, you can enhance time management and boost productivity, leading to sustainable business growth.

Competition & Market Differentiation

Competing with larger companies is among the most common business challenges. Their extensive resources can make it difficult for smaller businesses to stand out. However, focusing on your unique strengths can level the playing field. Emphasizing personalized customer service, for instance, can create a loyal customer base that values individualized attention. Additionally, highlighting specialized products or services that cater to specific needs can differentiate your business from larger competitors.

Identifying a unique value proposition is essential in attracting customers. Understanding what sets your offerings apart allows you to communicate this effectively to your target audience. Conducting market research can provide insights into customer preferences and gaps in the market. This information enables you to tailor your products or services to meet those needs uniquely. Moreover, clearly articulating the benefits and distinct features of your offerings in your marketing materials can attract and retain customers.

Keeping up with industry trends and adapting to changes is vital for sustained success. Regularly monitoring market developments helps you stay informed about emerging technologies and shifts in consumer behavior. Attending industry events and engaging with professional networks can provide valuable insights and foster innovation. Furthermore, being open to change and willing to adjust your business strategies ensures you remain competitive in a dynamic market.

By leveraging your unique strengths, clearly defining your value proposition, and staying abreast of industry trends, you can effectively navigate the challenges posed by larger competitors. These strategies not only enhance your market position but also foster customer loyalty and business growth.

Talent Acquisition & Retention

Attracting and retaining skilled employees on a small business budget is among the most common business challenges. To compete with larger companies, consider adopting skills-based hiring practices. This approach focuses on candidates’ competencies rather than formal qualifications, widening your talent pool. Additionally, offering flexible work arrangements can make your business more appealing to prospective employees. While you may not match the salaries of larger firms, providing a supportive work environment and opportunities for growth can attract dedicated individuals.

High turnover rates and employee dissatisfaction can significantly impact your business’s stability and morale. To address this, prioritize open communication and actively seek employee feedback. Implementing regular check-ins allows you to identify and resolve issues promptly, fostering a sense of value and belonging among staff. Moreover, recognizing and rewarding employees’ contributions can boost morale and reduce turnover. Even simple acknowledgments of hard work can enhance job satisfaction and loyalty.

A lack of proper training and development programs often leads to decreased productivity and engagement. Investing in employee development doesn’t have to be costly. Utilize online resources and in-house expertise to create training opportunities that enhance your team’s skills. Encouraging continuous learning not only improves performance but also demonstrates your commitment to employees’ professional growth. This investment can lead to increased retention and a more skilled workforce, driving your business’s success.

By focusing on these strategies, you can effectively navigate the challenges of talent acquisition and retention, even with limited resources. Building a positive workplace culture, offering growth opportunities, and maintaining open communication are key to attracting and keeping the right talent for your small business.

Scaling & Business Growth

Scaling your business without compromising quality is among the most common business challenges. Rapid expansion can often lead to diminished product or service standards. To prevent this, it’s essential to implement scalable processes and maintain rigorous quality control measures. Documenting standard operating procedures ensures consistency as your team grows. Additionally, investing in employee training fosters a culture of excellence, enabling your staff to uphold quality standards during periods of growth.

An unclear roadmap for business growth and sustainability can impede progress. Developing a strategic plan with defined goals and milestones provides direction and measurable objectives. Regularly reviewing and adjusting this plan allows your business to adapt to market changes and emerging opportunities. Engaging with mentors or industry experts can offer valuable insights, helping you refine your growth strategies and avoid common pitfalls.

The lack of automation or scalable processes often results in inefficiencies and increased workloads. Implementing automation tools can streamline repetitive tasks, freeing up time for strategic activities. For example, adopting project management software enhances collaboration and keeps teams aligned. Moreover, automating customer relationship management ensures consistent and personalized interactions, improving customer satisfaction. By embracing technology, your business can scale operations efficiently while maintaining high-quality standards.

By focusing on these strategies, you can navigate the complexities of scaling your business, ensuring sustainable growth without sacrificing quality.

Technology & Digital Transformation

Operating with outdated technology is among the most common business challenges, as it can significantly hinder efficiency and productivity. Legacy systems often lead to frequent downtimes and incompatibility with newer applications, disrupting daily operations. To address this, consider conducting a comprehensive technology audit to identify obsolete equipment and software. Investing in modern, energy-efficient devices and up-to-date software not only enhances performance but can also reduce long-term operational costs. Additionally, integrating smart assistants and cloud services can automate manual tasks, further boosting productivity.

Implementing digital tools for operations and marketing presents another layer of complexity. The vast array of available technologies can be overwhelming, making it challenging to select the right solutions. Begin by clearly defining your business needs and objectives. Research and choose user-friendly tools that align with these goals and offer scalability as your business grows. Providing adequate training for your team ensures smooth adoption and maximizes the benefits of these digital tools. Regularly evaluating the effectiveness of the implemented technologies allows for timely adjustments and improvements.

Security concerns, including data breaches and cyber threats, are prevalent among small businesses. Limited resources often result in inadequate cybersecurity measures, making these businesses attractive targets for cybercriminals. To mitigate these risks, establish strong internal controls by implementing clear policies around financial management and inventory control. Limiting employee access to sensitive information and enforcing regular password changes can further enhance security. Additionally, adopting multi-factor authentication and restricting administrative privileges serve as effective deterrents against unauthorized access.

By proactively updating technology, thoughtfully integrating digital tools, and strengthening cybersecurity measures, small businesses can overcome these common challenges. These steps not only improve operational efficiency but also position your business for sustainable growth in an increasingly digital marketplace.

Customer Service & Satisfaction

Managing customer complaints and negative reviews is among the most common business challenges. Effectively addressing these issues is crucial for maintaining a positive reputation. Begin by responding promptly and professionally to all feedback, demonstrating empathy and a genuine desire to resolve concerns. This approach not only appeases the dissatisfied customer but also showcases your commitment to service excellence to potential clients. Additionally, view negative feedback as an opportunity to identify areas for improvement within your operations. Implementing changes based on constructive criticism can enhance overall customer satisfaction.

A lack of streamlined customer service processes often leads to inefficiencies and frustrated customers. To combat this, consider adopting an omnichannel support system that consolidates various communication platforms into a single interface. This integration allows your team to manage inquiries more effectively, reducing response times and improving the customer experience. Implementing AI-powered chatbots can also handle routine queries, freeing up human agents to focus on more complex issues. Regularly reviewing and optimizing these processes ensures they remain effective and aligned with customer expectations.

Slow response times can result in lost business and diminished customer trust. To enhance responsiveness, invest in advanced communication tools such as virtual phone systems and live chat functionalities. These technologies enable real-time interactions, addressing customer needs promptly. Additionally, training your staff to prioritize inquiries and manage time efficiently can significantly reduce wait times. Establishing clear guidelines for response times and monitoring performance metrics helps maintain high standards of service. By proactively improving your customer service framework, you can foster loyalty and drive business growth.

Adapting to Economic & Market Changes

Adapting to economic and market changes is among the most common business challenges. Inflation and rising costs can significantly impact your operations, squeezing profit margins and increasing expenses. To mitigate these effects, consider conducting a thorough review of your operational costs to identify areas where you can reduce expenses without compromising quality. Implementing energy-efficient technologies and optimizing resource usage can lead to substantial savings. Additionally, exploring alternative suppliers or negotiating better terms with existing ones can help manage costs effectively. Regularly updating your pricing strategy to reflect increased costs ensures that your business remains profitable while maintaining customer trust.

Changes in consumer behavior and preferences require businesses to stay agile and responsive. To keep pace, invest time in market research to understand evolving customer needs and expectations. Utilizing digital tools and analytics can provide insights into purchasing patterns, enabling you to tailor your products or services accordingly. Engaging with customers through social media platforms fosters a sense of community and allows for real-time feedback. Offering personalized experiences and adapting your offerings based on customer input can enhance satisfaction and loyalty. Flexibility in your business model, such as introducing new product lines or services, can also cater to shifting demands and open new revenue streams.

Supply chain issues affecting product availability pose significant challenges to maintaining consistent operations. To address this, consider diversifying your supplier base to reduce dependency on a single source. Building strong relationships with multiple suppliers can provide alternatives when disruptions occur. Implementing inventory management systems helps monitor stock levels in real-time, allowing for proactive reordering and minimizing shortages. Exploring local sourcing options can reduce lead times and transportation costs, enhancing reliability. Additionally, investing in technology to forecast demand accurately enables better planning and reduces the risk of overstocking or stockouts.

Conclusion

Running a business comes with constant challenges, but each obstacle presents an opportunity for growth. Addressing the most common business challenges requires a proactive approach and a willingness to adapt. By refining your strategies and staying flexible, you can improve efficiency and build long-term success.

However, overcoming these issues takes time and effort. Focusing on sustainable solutions instead of quick fixes helps create stability. Regularly reviewing your operations and adjusting to market demands allows your business to remain competitive. Additionally, investing in your team and improving customer relationships strengthens your foundation for continued growth.

Technology, customer expectations, and industry trends will always evolve. Staying informed and open to change keeps you ahead of challenges. Leveraging data and market insights can help you make smarter business decisions. Building strong relationships with suppliers, employees, and customers also contributes to long-term success.

While obstacles may slow progress, persistence leads to results. Small improvements over time create lasting impacts. By focusing on efficiency, adaptability, and innovation, you can strengthen your business and navigate uncertainty with confidence. The right strategies and mindset can help you turn challenges into opportunities and build a more resilient company.