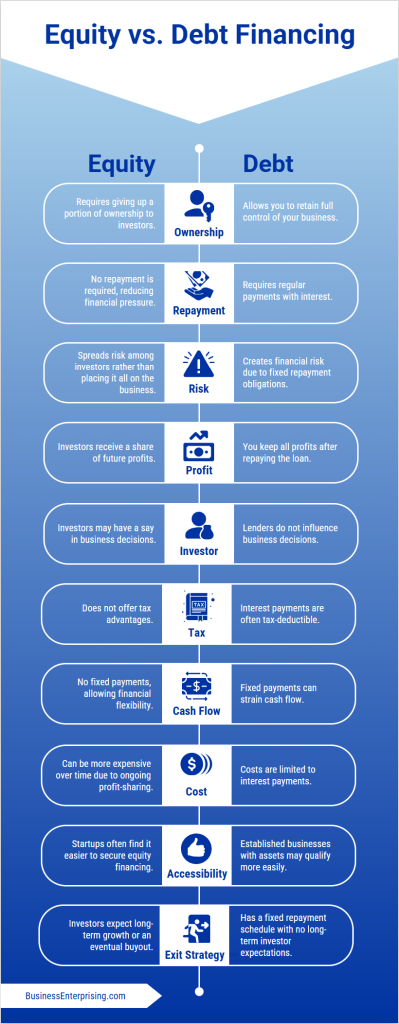

Navigating the financial landscape of your business often involves choosing between equity vs. debt funding. Understanding the differences between these financing options is crucial for informed decision-making. Equity financing involves raising capital by selling shares of your company. This approach doesn’t require repayment, reducing immediate financial pressure. However, it dilutes ownership and may lead to shared control with investors. Conversely, debt financing entails borrowing funds that must be repaid over time, typically with interest. While this preserves your ownership stake, it introduces fixed obligations that can strain cash flow.

Navigating the financial landscape of your business often involves choosing between equity vs. debt funding. Understanding the differences between these financing options is crucial for informed decision-making. Equity financing involves raising capital by selling shares of your company. This approach doesn’t require repayment, reducing immediate financial pressure. However, it dilutes ownership and may lead to shared control with investors. Conversely, debt financing entails borrowing funds that must be repaid over time, typically with interest. While this preserves your ownership stake, it introduces fixed obligations that can strain cash flow.

Each funding method impacts your business differently. Equity financing can provide valuable investor expertise but may compromise autonomy. Debt financing maintains control but increases financial risk due to mandatory repayments. Therefore, assessing your company’s financial health, growth prospects, and risk tolerance is essential when considering equity vs. debt funding.

Understanding Equity and Debt Funding

Understanding the distinctions between equity and debt funding is essential for making informed financial decisions in business. Equity financing involves raising capital by selling ownership stakes in your company to investors. In return, these investors receive shares, entitling them to a portion of future profits. This approach means you don’t have to repay funds or pay interest. However, it results in shared control and diluted ownership.

In contrast, debt financing entails borrowing money that you must repay over time, typically with interest. Common forms include loans and bonds. This method allows you to retain full ownership of your business. However, it obligates you to regular repayments regardless of your company’s profitability. Failure to meet these obligations can lead to financial distress or bankruptcy.

When considering equity vs. debt funding, it’s crucial to assess how each option impacts your business’s ownership structure and financial responsibilities. Equity financing reduces personal financial risk but requires sharing profits and decision-making authority. Debt financing preserves your control but adds fixed financial obligations that can strain cash flow. Therefore, aligning your funding choice with your company’s financial health, growth prospects, and risk tolerance is vital.

Pros and Cons of Equity Financing

Equity financing offers distinct advantages and disadvantages for businesses seeking capital. Understanding these can help you decide between equity vs. debt funding.

One significant advantage of equity financing is the absence of repayment obligations. Unlike loans, you don’t need to make monthly payments, freeing up cash flow for operations and growth. This can be especially beneficial for startups without immediate revenue streams. Additionally, equity investors often bring valuable expertise and networks to your business. Their insights can guide strategic decisions and open doors to new opportunities. This mentorship can be as valuable as the capital itself.

However, equity financing also has notable disadvantages. By selling shares, you dilute your ownership stake, potentially losing some control over business decisions. Investors may seek input on company direction, which could conflict with your vision. Moreover, equity investors are entitled to a portion of your profits. This profit-sharing can reduce the earnings you retain, impacting your personal financial returns. Therefore, it’s essential to weigh these factors carefully when considering equity financing.

In summary, equity financing provides capital without the burden of debt but requires sharing ownership and profits. Assessing your business’s needs and goals will help determine if this funding route aligns with your long-term objectives.

Pros and Cons of Debt Financing

Debt financing allows you to raise capital by borrowing funds, which you repay over time with interest. A key benefit is that you maintain full ownership of your business, as lenders don’t acquire equity or control. Additionally, interest payments on debt are often tax-deductible, reducing your taxable income and overall tax liability. This tax advantage can make debt an attractive financing option.

However, debt financing has its drawbacks. You must make regular interest payments, which can strain cash flow, especially during periods of low revenue. Failure to meet these obligations can lead to financial distress or even bankruptcy. Moreover, taking on debt increases your financial risk, as you’re obligated to repay regardless of your business’s performance. Therefore, it’s crucial to carefully assess your company’s ability to manage debt before proceeding.

When evaluating equity vs. debt funding, consider how debt financing aligns with your business goals and risk tolerance. While it preserves ownership and offers tax benefits, the associated repayment obligations and increased financial risk require thorough consideration. Balancing these factors is essential to determine the most suitable financing strategy for your business’s long-term success.

How to Determine the Right Funding Option for Your Business

Determining the right funding option for your business requires careful consideration of various factors, including your company’s stage, cash flow, and risk tolerance. Early-stage startups often lack substantial revenue, making equity financing appealing. This approach provides capital without immediate repayment obligations, allowing focus on growth. However, established businesses with steady cash flow might prefer debt financing to maintain ownership while leveraging predictable income to meet repayment schedules.

Cash flow stability plays a crucial role in this decision. If your business generates consistent revenue, debt financing can be manageable, offering tax-deductible interest payments and preserving equity. Conversely, if cash flow is unpredictable, equity financing reduces the pressure of fixed repayments, though it entails sharing future profits with investors.

Risk tolerance also influences the choice between equity and debt funding. Risk-averse entrepreneurs may favor equity financing to avoid the obligation of debt repayment, especially during uncertain market conditions. On the other hand, those comfortable with calculated risks might opt for debt financing to retain full control over their business operations.

Industry norms and preferences further guide this decision. For instance, technology startups often lean towards equity financing due to high initial costs and uncertain revenue streams. In contrast, industries with tangible assets, like manufacturing, may find debt financing more suitable, as assets can serve as collateral, reducing lender risk.

Ultimately, assessing your business’s unique circumstances and aligning them with the characteristics of each funding option is essential. This strategic approach ensures that your choice between equity and debt financing supports your company’s long-term success and stability.

Common Sources of Equity and Debt Funding

When exploring funding options for your business, it’s essential to understand the various sources of equity and debt financing available. Each option has unique characteristics that can impact your company’s financial strategy.

Equity Financing

Equity financing involves raising capital by selling shares of your company, thereby sharing ownership with investors. Common sources include:

Venture Capital: Venture capitalists invest in startups with high growth potential, providing substantial funds in exchange for equity. They often offer strategic guidance to help scale the business.

Angel Investors: These are affluent individuals who invest personal funds into early-stage companies. Beyond capital, they may provide valuable industry expertise and networking opportunities.

Crowdfunding: Platforms enable businesses to raise small amounts of money from a large number of people, typically via the internet. This approach can also serve as a marketing tool, increasing brand visibility.

Private Equity: Private equity firms invest in established companies, often aiming to improve profitability before selling their stake. This source is suitable for businesses seeking significant capital for expansion or restructuring.

Debt Financing

Debt financing entails borrowing funds that must be repaid over time, usually with interest. Common sources include:

Bank Loans: Traditional bank loans provide a lump sum that businesses repay over a fixed period. They often require collateral and have stringent approval processes.

Lines of Credit: Banks offer lines of credit, allowing businesses to borrow up to a certain limit as needed. This flexible option helps manage short-term cash flow needs.

Bonds: Companies can issue bonds to investors, promising to pay back the principal along with periodic interest payments. This method is typically used by larger corporations.

Alternative Lenders: Non-bank lenders, such as private credit funds, offer various loan products, often with more flexible terms than traditional banks. They have become significant players in the lending market, providing options for businesses that may not qualify for conventional loans.

Understanding these funding sources is crucial when evaluating equity vs. debt funding for your business. Each option carries distinct implications for ownership, control, and financial obligations. Carefully assessing your company’s needs and strategic goals will help determine the most appropriate financing mix.

Real-World Examples of Businesses Using Equity and Debt Financing

Understanding how companies utilize equity and debt financing provides valuable insights into their strategic decisions. Examining real-world cases highlights both successful applications and potential pitfalls associated with each funding method.

Successful Use of Equity Financing

A notable example of effective equity financing is Brookfield Asset Management’s recent initiative. The firm raised approximately $1 billion to support smaller infrastructure companies. This approach allows Brookfield to inject capital into growing businesses without burdening them with debt obligations. Consequently, these companies can expand operations while maintaining financial flexibility.

Challenges with Debt Financing

Conversely, reliance on debt financing can lead to significant challenges. The collapse of SunEdison serves as a cautionary tale. The company amassed over $11 billion in debt due to rapid expansion and aggressive acquisitions. This debt-fueled growth strategy ultimately led to bankruptcy in 2016, underscoring the risks associated with excessive leverage.

Similarly, Parmalat’s downfall illustrates the dangers of mismanaged debt. The company engaged in questionable accounting practices to hide its mounting liabilities, leading to a €14.3 billion debt revelation and insolvency. This case emphasizes the importance of transparency and prudent debt management.

Lessons Learned

These examples highlight the critical importance of aligning funding strategies with a company’s operational realities and market conditions. While equity financing can provide growth capital without immediate repayment pressures, it may dilute ownership. Conversely, debt financing allows owners to retain control but introduces fixed obligations that can strain cash flow. Therefore, a balanced approach, considering the specific context and long-term goals, is essential when evaluating equity vs. debt funding options.

Conclusion

Choosing between equity and debt financing is a pivotal decision for your business. Each option offers distinct benefits and potential drawbacks. Equity financing provides capital without immediate repayment obligations, which can be advantageous for startups lacking steady cash flow. However, it often requires relinquishing a portion of ownership and control. Conversely, debt financing allows you to retain full ownership but introduces mandatory interest payments, impacting cash flow. Therefore, assessing your company’s financial health, growth prospects, and risk tolerance is essential when considering equity vs. debt funding. Additionally, aligning your choice with industry norms and investor expectations can enhance your business’s financial strategy. By carefully evaluating these factors, you can select a funding approach that supports your long-term objectives and fosters sustainable growth.