Finding the right funding is one of the biggest decisions you’ll make as a business owner. A Comprehensive Guide to Business Funding helps you understand your options before making a commitment. You need money to grow, launch, or solve short-term problems. However, not all funding sources work the same way.

Finding the right funding is one of the biggest decisions you’ll make as a business owner. A Comprehensive Guide to Business Funding helps you understand your options before making a commitment. You need money to grow, launch, or solve short-term problems. However, not all funding sources work the same way.

Therefore, it’s important to choose carefully based on your goals, stage, and risk tolerance. Some options require repayment with interest. Others involve giving up equity or offering collateral. Additionally, timelines and requirements vary depending on the lender or investor.

You may need fast access to cash or long-term support for expansion. Each situation calls for a different approach. Therefore, it helps to compare options like loans, grants, or investor backing. Additionally, your credit score and business history will affect what’s available to you.

However, even startups with no revenue still have funding opportunities. These may require more effort to secure, but they do exist. Therefore, planning ahead can save time and improve your chances. Additionally, having the right documents prepared makes the process smoother.

Some funding sources offer more flexibility than others. Others may come with higher costs or more oversight. Therefore, know what you’re trading in return for support. A good funding decision supports your long-term plans without putting you in a bind.

This guide walks you through the most common questions and choices. Additionally, it gives you practical tips you can apply right away. With clear information and realistic goals, you’ll be better prepared to choose the funding path that fits your needs.

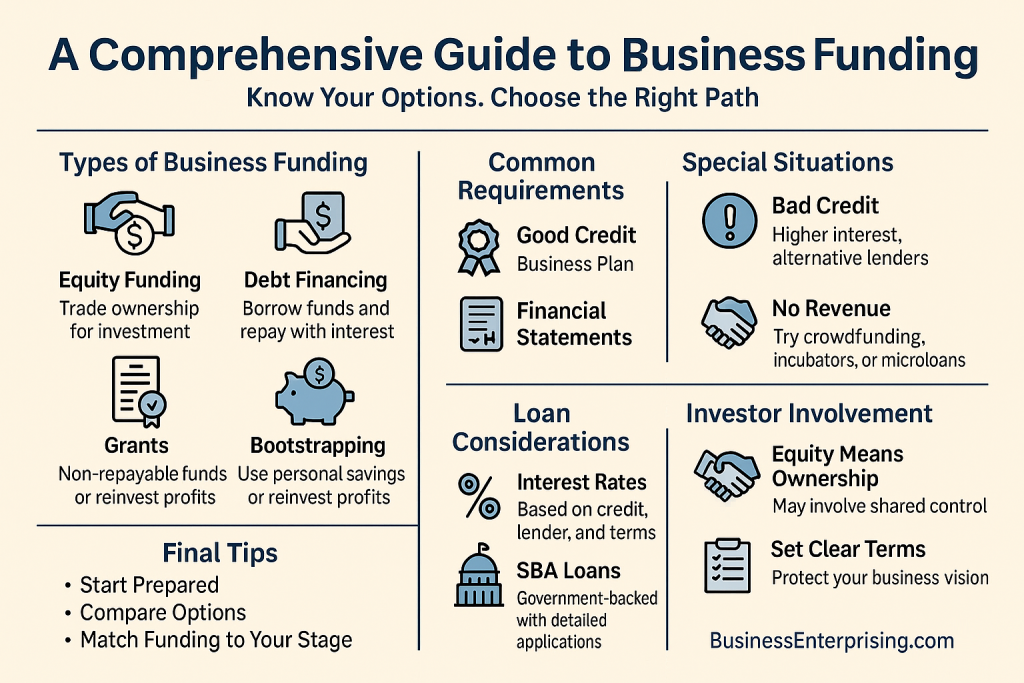

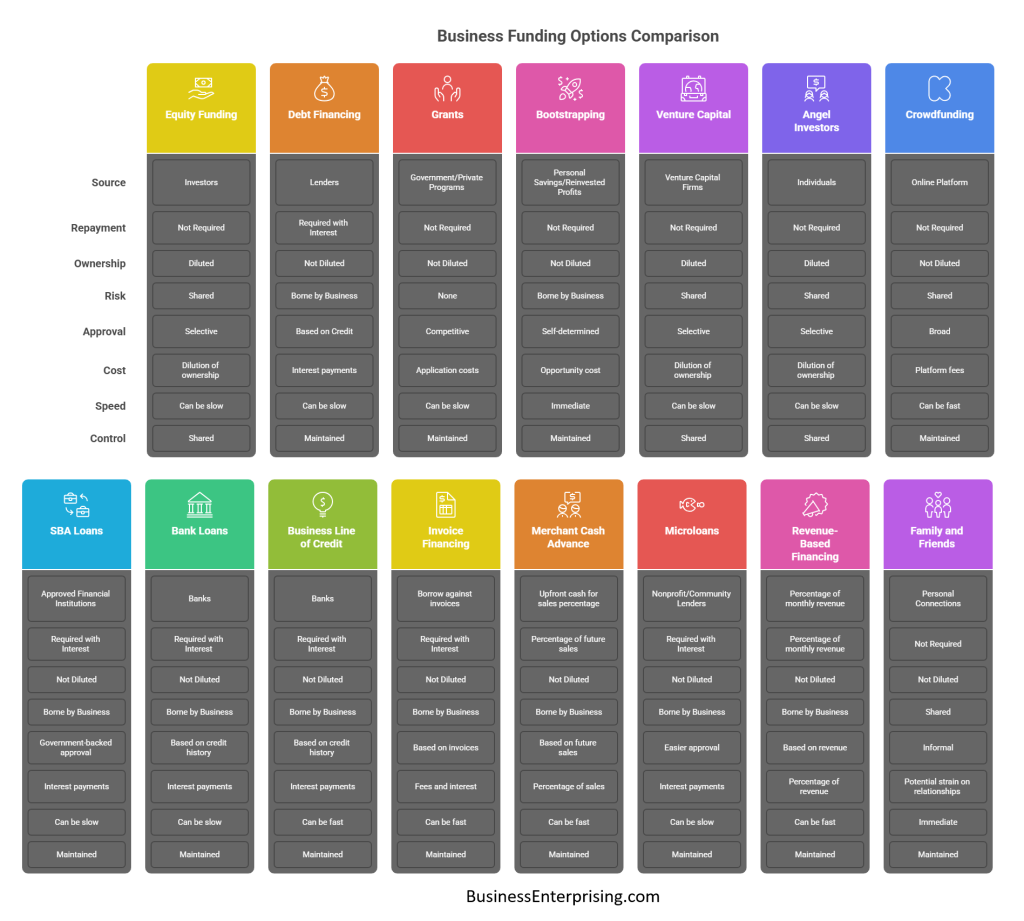

What are the main types of business funding?

Equity funding, debt financing, grants, and bootstrapping are the most common types.

Finding the right funding option can shape how your business grows. You have several choices, and each one works differently. Equity funding involves giving up ownership in exchange for capital. Investors get a share of your business and often bring experience or connections. However, they usually expect long-term returns and involvement in major decisions.

Debt financing is another common option. You borrow money and repay it over time, usually with interest. Banks and online lenders often offer business loans. This lets you keep full ownership, but you must stay on top of payments. Additionally, you’ll need decent credit and strong financials to qualify.

Grants offer another path. These funds don’t need to be repaid. They often come from government programs or private organizations. However, the application process can be time-consuming, and approval rates are low. Therefore, it’s wise to apply only if you meet all the requirements.

You might also consider bootstrapping. This means using your own money or reinvesting profits to grow the business. It keeps you in control but can slow growth. Additionally, you take on all the risk yourself, which can be stressful.

Altogether, these are the main options most businesses consider. Each has pros and cons depending on your goals and stage of growth. A Comprehensive Guide to Business Funding should explain how these choices compare in real terms.

Before deciding, think about how much control you want to keep. Also consider how quickly you need money and how confident you are in your revenue projections. You don’t need to rush the decision. Choosing the right type of funding can make future planning much easier.

How do I qualify for a small business loan?

You typically need good credit, a solid business plan, and proof of steady income or revenue.

Getting approved for a small business loan depends on several key factors. Most lenders start by checking your credit score. A higher score shows that you manage debt well. Therefore, it increases your chances of approval and lowers your interest rate. However, a lower score doesn’t always mean you’ll be denied. Some lenders offer loans based on other criteria.

Additionally, lenders want to see a clear business plan. It should explain what your business does and how you plan to repay the loan. You don’t need it to be fancy. However, it must include projected income, expenses, and growth expectations. Therefore, be honest and realistic about your numbers.

Proof of steady revenue also matters. Lenders prefer businesses with consistent cash flow. Bank statements or tax returns usually support this. If your income varies each month, explain why. Additionally, it helps to show a pattern of growth or repeat customers.

Collateral may also come up. This means offering an asset the lender can take if you default. It could be equipment, inventory, or a personal guarantee. Not all loans require this. However, having collateral often improves your terms or chances of approval.

A Comprehensive Guide to Business Funding would recommend reviewing your finances before you apply. That means checking your credit, gathering paperwork, and improving any weak spots. Additionally, compare loan options to find one that matches your business needs.

Don’t rush the process. Take time to prepare so you look strong on paper. A solid application helps you get better terms and long-term results.

What documents are needed to apply for business funding?

Common documents include tax returns, financial statements, business licenses, and a business plan.

When you apply for business funding, you’ll need to provide documents that support your request. Lenders or investors want to see proof. Therefore, having your paperwork ready can speed things up and help your application stand out. You don’t need to submit everything at once, but most applications start with a few core items.

Tax returns are usually at the top of the list. They help verify income, expenses, and past financial performance. Therefore, most lenders ask for at least two years of business and sometimes personal returns. Additionally, your financial statements matter. These include your profit and loss report, balance sheet, and cash flow statement. They show how your business manages money.

You may also need a copy of your business license. This proves that your business is legally registered and operating within the rules. Some lenders also ask for articles of incorporation or partnership agreements. However, this depends on your business structure. Therefore, it’s helpful to keep these documents updated and easy to access.

A strong business plan is another important document. It outlines your goals, expected revenue, and repayment strategy. Lenders want to know how you’ll use the funds. Additionally, they want to feel confident in your ability to repay them. A clear plan improves your chances.

A Comprehensive Guide to Business Funding would recommend keeping these documents organized year-round. That way, you’re ready when funding opportunities come up. Additionally, review everything for accuracy before you apply. Mistakes can delay approval or cause a denial.

Taking time to gather the right documents shows lenders you’re serious. It also gives them what they need to make a quick decision.

Can I get funding with bad credit?

Yes, but options may be limited to high-interest loans, alternative lenders, or collateral-backed financing.

Getting business funding with bad credit isn’t impossible, but it does come with trade-offs. Traditional banks may turn you down quickly. However, alternative lenders often offer options for borrowers with lower credit scores. These might include short-term loans, merchant cash advances, or revenue-based financing.

Additionally, you can still apply if you have valuable collateral. Assets like property, equipment, or inventory may help you secure funding. Lenders feel more comfortable taking a risk when they have something to fall back on. Therefore, secured loans can work even if your credit score is weak.

Some lenders also consider your current cash flow. If you have steady revenue, you may qualify for limited funding. However, you’ll likely pay higher interest and fees. Therefore, always read the terms carefully before signing anything. Compare offers and avoid lenders who seem too aggressive or vague.

You can also look into microloans or community programs. These often support businesses that can’t meet standard lending rules. Additionally, personal loans from friends or family might be an option. Just make sure to put the agreement in writing. That protects both sides and avoids confusion later.

A Comprehensive Guide to Business Funding would tell you to clean up your finances before applying. Pay off small debts, correct errors, and prepare clear financial records. Additionally, build relationships with lenders over time. Some offer better terms after a few successful payments.

Bad credit doesn’t mean you’re out of options. It just means you’ll need to be more careful and strategic when applying for funding.

How much funding can I get for my business?

It depends on your creditworthiness, business revenue, funding source, and loan type.

The amount of funding you can get depends on several factors. Lenders and investors look at your business as a whole. They evaluate your credit, annual revenue, and time in business. Therefore, stronger financials usually lead to higher offers and better terms.

However, not all funding sources use the same criteria. Banks tend to offer larger loans, but their standards are strict. Alternative lenders may provide smaller amounts with easier qualifications. Additionally, grant programs may cap funding based on your project size or industry.

You should also consider the type of funding you apply for. A line of credit works differently than a term loan. Therefore, the maximum you can borrow varies with each type. Equipment loans, for example, are often based on the cost of the item.

Additionally, lenders usually offer between 10% and 30% of your annual revenue. So if your business makes $100,000 per year, expect funding in that range. However, having strong cash flow and consistent sales may help you get more.

A Comprehensive Guide to Business Funding would advise calculating how much you actually need before applying. Asking for too much can raise red flags. Additionally, overborrowing may lead to financial stress later on.

Therefore, review your business plan and financial forecasts. Use real numbers to figure out your funding goal. Lenders like borrowers who know what they’re asking for and why.

The more organized and realistic you are, the better your chances. Funding is available, but how much you get depends on your preparation and current performance.

What’s the difference between a loan and a grant?

Loans must be repaid with interest, while grants are non-repayable funds typically tied to specific criteria.

Understanding the difference between a loan and a grant can help you choose the right funding for your business. A loan is borrowed money you repay over time, usually with interest. However, a grant is money you don’t have to repay, as long as you meet the terms.

Grants are often tied to specific programs, industries, or business types. Therefore, you usually need to meet strict requirements to qualify. Additionally, grant applications can be time-consuming and competitive. Still, many business owners apply because grants don’t add debt to their books.

Loans come from banks, credit unions, and online lenders. You receive the money upfront and repay it in fixed installments. Therefore, loans may work better if you need flexible use of funds. However, you must be ready for regular payments, even during slower business months.

Additionally, your credit score plays a bigger role with loans. Strong credit can lead to lower interest rates and better terms. With grants, the focus is more on purpose and eligibility. Therefore, both funding types require different preparation and strategy.

A Comprehensive Guide to Business Funding would help you compare options based on your goals. It’s not always about what’s easier to get. Sometimes, it’s about what makes more sense for your business. Additionally, you should think about how each option affects your cash flow.

Before applying, decide how much risk you’re comfortable with. Loans bring financial responsibility, while grants require compliance. Both can help your business grow, but only if you use them wisely.

Are there funding options for startups with no revenue?

Yes, some investors, incubators, and crowdfunding platforms fund promising pre-revenue startups.

Getting funding for a startup with no revenue can feel difficult, but it’s not impossible. Some funders focus on potential, not sales. Therefore, they may support your idea if you present it well. These options often include angel investors, business incubators, and crowdfunding campaigns.

However, you’ll need to show something in return. A clear business plan, strong team, and working prototype help build trust. Additionally, your pitch should explain why your idea stands out. Many investors look for originality and market demand, not just early profits.

Crowdfunding can also be a useful option. You raise money by getting small contributions from many people. Therefore, you’ll need a strong campaign and clear messaging. Additionally, it helps to offer rewards or future products in exchange. This builds interest and trust with your audience.

You may also find opportunities through incubators or pitch contests. These programs offer funding, support, or workspace in exchange for equity. However, competition is strong, and selection can be tough. Therefore, polish your application and be ready to pitch in person.

A Comprehensive Guide to Business Funding would encourage startups to look beyond banks. Traditional lenders often want steady income and credit history. However, early-stage investors may care more about your long-term potential. Additionally, some government programs offer limited support to pre-revenue businesses.

If you don’t get funding right away, keep building traction. Each step forward can help you look more fundable next time. Persistence matters when revenue is still out of reach.

How long does it take to get business funding?

It can take anywhere from a few days to several months, depending on the funding source.

The time it takes to get business funding depends on the type of funding you pursue. Some online lenders approve applications quickly. You might receive funds within a few days. However, traditional banks can take several weeks or even longer.

Additionally, grant programs and venture capital deals often involve multiple steps. These can take months from start to finish. Therefore, it’s important to plan ahead and leave time for delays. If you need fast funding, you may need to accept higher rates or fees.

Loan approval timelines vary by lender and loan size. Smaller loans usually move faster. However, large loans often require deeper review. Therefore, keep your paperwork organized and respond quickly to lender requests. That helps speed up the process.

You should also consider how prepared you are before applying. If your documents are incomplete, expect delays. Additionally, any errors or missing items will slow things down. Therefore, double-check everything before you submit your application.

A Comprehensive Guide to Business Funding would recommend starting early, even before you need the money. That gives you time to explore all your options. Additionally, it helps you avoid settling for terms that don’t support your goals.

Set realistic expectations based on the funding source you choose. Grants take longer than loans. Venture capital deals take longer than crowdfunding. However, good preparation can shorten your wait. Your timing may also improve with stronger credit or steady revenue.

Funding doesn’t always come fast, but with the right approach, you can avoid unnecessary delays.

What is venture capital and how does it work?

Venture capital is equity investment from firms or individuals in exchange for ownership and growth potential.

Venture capital is money invested into startups in exchange for ownership. The goal is to support businesses with high growth potential. However, this type of funding usually comes with expectations. Investors want a strong return when your business succeeds or exits.

Additionally, venture capitalists often take an active role. They may offer advice, set conditions, or help make key decisions. Therefore, you must be comfortable sharing control. Some founders benefit from this guidance. Others prefer to keep more independence.

Getting venture capital is competitive. You’ll need a strong pitch, a scalable business model, and a capable team. Additionally, your product should solve a real problem. Most investors want to see early traction before they invest.

The process can take months. Meetings, due diligence, and legal steps all require time. However, the results can be worth it. A single investment can fund product development, marketing, and hiring. Therefore, many startups view venture capital as a path to fast growth.

A Comprehensive Guide to Business Funding would explain how venture capital compares to other types. Unlike loans, you don’t repay the money. Instead, you give up equity. Additionally, success means your investors also profit, usually when the company is sold or goes public.

Before pursuing venture capital, consider your long-term goals. If fast growth is the focus, it may be a good fit. However, if you prefer full control, other funding sources might work better. The right choice depends on your vision and your willingness to share ownership.

Do I need a business plan to secure funding?

Yes, most lenders and investors require a detailed business plan to evaluate risk and potential.

Most lenders and investors expect to see a business plan before offering funding. It shows that you’ve thought through your goals. Additionally, it explains how you plan to grow and repay what you borrow. A clear plan helps reduce the risk in their eyes.

However, not every plan needs to be long or formal. You can write a simple one that still covers the key points. It should include your product, target market, sales strategy, and financial projections. Therefore, focus on clarity and real numbers.

Additionally, your plan should show how funding will be used. Lenders want to know how their money will support your business. Therefore, be specific about your expenses. Include inventory, marketing, staffing, or any other major use of funds.

Investors often use your plan to judge potential returns. If you want equity funding, your numbers need to make sense. However, even if you’re applying for a small loan, a plan helps build trust. It shows that you’re prepared and serious.

A Comprehensive Guide to Business Funding would suggest tailoring your plan to your audience. A bank may look for stability. An investor may look for growth. Therefore, adjust your tone and content based on who will read it.

Your business plan can also help you stay focused. Additionally, it gives you a roadmap as your company grows. Writing it may feel like extra work, but it’s a key part of getting funded.

What is the interest rate on business loans?

Interest rates vary widely based on credit score, lender, loan type, and repayment terms.

Interest rates on business loans can vary quite a bit. They depend on your credit score, lender type, and loan structure. Therefore, your rate might be very low or surprisingly high. Traditional banks often offer better rates to borrowers with strong credit.

However, if your credit is lower or your business is new, expect to pay more. Online lenders often approve faster but charge higher rates. Additionally, some loans include fees that act like added interest. Always read the full terms before accepting an offer.

Rates can also change based on the loan’s purpose. Equipment loans may cost less than unsecured working capital loans. Therefore, it’s smart to match your funding type with your need. Additionally, shorter-term loans often have higher rates, even if the total repayment seems low.

Lenders also look at your time in business and annual revenue. If you’re new, they see more risk. Therefore, you may only qualify for loans with higher rates or stricter repayment terms. However, building strong business credit can lower your rates over time.

A Comprehensive Guide to Business Funding would advise comparing multiple offers. Don’t accept the first rate you see. Additionally, check if the rate is fixed or variable. A fixed rate stays the same, while a variable one can rise.

Even small differences in interest can affect your total cost. Therefore, factor the rate into your monthly budget before borrowing. Make sure the loan still helps your business grow. Borrowing with a plan keeps your debt manageable and your business on track.

Is crowdfunding a viable way to fund my business?

Yes, if you can create a compelling campaign and promote it effectively to potential backers.

Crowdfunding can be a practical way to raise money for your business. It works by collecting small contributions from many backers. However, you’ll need a clear message and a strong reason for people to support you. Therefore, your campaign must explain what you’re building and why it matters.

Additionally, offering something in return helps attract support. Many campaigns promise early access to a product or exclusive rewards. This builds trust and interest. However, you must deliver what you promise. Failing to follow through can damage your reputation.

Success depends on how well you promote your campaign. Therefore, plan to market it before and during the launch. Use social media, email lists, and personal outreach. Additionally, videos or product demos can help people connect with your idea. Backers want to feel part of something meaningful.

Crowdfunding also gives you more than just funding. It helps you test your idea and gather early feedback. Therefore, it can be a good way to validate your product before full production. However, competition is high, and not every campaign gets funded. That’s why preparation is so important.

A Comprehensive Guide to Business Funding would point out that crowdfunding isn’t easy money. It takes planning, effort, and communication. Additionally, you must budget for platform fees, production costs, and marketing. Still, for the right product, it can work well.

If you’re confident in your pitch and have time to promote it, crowdfunding could be a smart move. Just treat it like a real launch.

Can I use personal savings as business funding?

Yes, self-funding (bootstrapping) is common, especially in the early stages of a business.

Using personal savings to fund your business is common, especially when you’re just starting out. Many entrepreneurs begin this way. It gives you full control and avoids debt. However, it also puts your personal finances at risk.

Therefore, it’s important to decide how much you can afford to spend. Set a limit before you invest. Additionally, keep your business and personal accounts separate. That helps you track expenses more clearly and stay organized.

Bootstrapping allows you to move quickly without waiting on outside approval. You can test ideas, build products, and market directly. However, without extra capital, growth may take longer. Therefore, you must be careful about how you spend each dollar.

A Comprehensive Guide to Business Funding would suggest using personal savings wisely. Start small and scale based on real demand. Additionally, avoid putting all your money into one area of the business. Keep some reserves in case plans change or revenue falls short.

You may also combine self-funding with other methods. For example, you can use savings to start, then apply for grants or pitch to investors. This approach shows that you believe in your idea enough to invest in it. That can make others more willing to back you.

Using your own money gives you freedom but also adds pressure. Therefore, make each decision with both short-term needs and long-term goals in mind. Your business should grow at a pace that doesn’t put your personal stability at risk.

What is an SBA loan and how do I apply?

An SBA loan is a government-backed loan available through approved lenders, requiring detailed application and documentation.

An SBA loan is a small business loan partially backed by the government. You apply through approved lenders, not the SBA itself. Therefore, the lender handles your application and makes the final decision. However, the SBA reduces the lender’s risk by guaranteeing part of the loan.

These loans often come with favorable terms. You may get lower interest rates and longer repayment periods. Therefore, they’re a good option for businesses that qualify. However, approval requires a detailed application and strong financial records.

You’ll need to submit several documents. These usually include a business plan, tax returns, and financial statements. Additionally, you may need to provide information about collateral and ownership. Each lender may have slightly different requirements. Therefore, ask in advance what you need to prepare.

The process can take several weeks or longer. Therefore, it’s best to apply before you urgently need funds. Additionally, SBA loans are often used for working capital, equipment, or real estate. Some programs are designed for startups, while others serve established businesses.

A Comprehensive Guide to Business Funding would help you decide if an SBA loan fits your needs. If your business is stable and you have good credit, it may be a smart choice. Additionally, SBA loans can help you avoid high-interest options.

Before applying, review your credit, update your financials, and organize your paperwork. Preparation can make the process smoother and faster. With the right documents and timing, an SBA loan can support steady, affordable business growth.

Do investors take control of my business?

Investors may seek partial control or input, depending on the deal structure and ownership stake.

When you accept funding from investors, you give up some ownership in your business. That ownership comes with certain rights. However, how much control they gain depends on the deal structure and the size of their investment.

Equity investors often want input on big decisions. These may include financial moves, hiring leadership, or selling the company. Therefore, you’ll want to review each investor agreement carefully. Some investors stay hands-off, while others want active involvement.

Additionally, early-stage investors may ask for board seats or voting rights. These requests help them protect their investment. However, they also affect how you run your business. Therefore, you need to decide how much control you’re comfortable sharing.

The more equity you give away, the less control you keep. Therefore, it’s important to balance funding needs with ownership goals. You may choose to bring in multiple investors with smaller stakes. That can reduce the influence of any one party.

A Comprehensive Guide to Business Funding would suggest discussing terms early in the process. Additionally, use a lawyer to help you understand long-term impacts. Clear terms now prevent conflict later.

If you want full control, other funding methods may be better. However, the right investor can also bring value. They may offer experience, networks, or strategic support. Just make sure the benefits outweigh the loss of autonomy.

Conclusion

Finding the right funding for your business takes time, research, and preparation. You have many options, each with pros and cons. However, not every funding type fits every business. Therefore, it helps to understand what you need and what you’re willing to give up.

Additionally, lenders and investors want to see that you’ve thought things through. A clear plan and solid financials make a strong impression. Therefore, prepare your documents, review your goals, and be ready to explain your next steps.

A Comprehensive Guide to Business Funding can help you weigh your options. It offers details that support better decision-making. However, even the best information won’t replace your own judgment. You know your business better than anyone else.

Therefore, choose funding that supports your goals without adding unnecessary risk. Additionally, take time to review terms carefully. Ask questions and get advice when needed. It’s better to wait than to take a deal that causes problems later.

If you’re just starting, personal savings or grants may make sense. If you’re growing fast, equity or loans might help. Therefore, match your funding to your current stage and your future plans.

Regardless of which path you choose, stay focused on results. Additionally, check in often on your progress and adjust when needed. A well-funded business still needs discipline to succeed.

With clear thinking and a realistic approach, you can find the right funding path. Use what you’ve learned and take the next step with confidence.