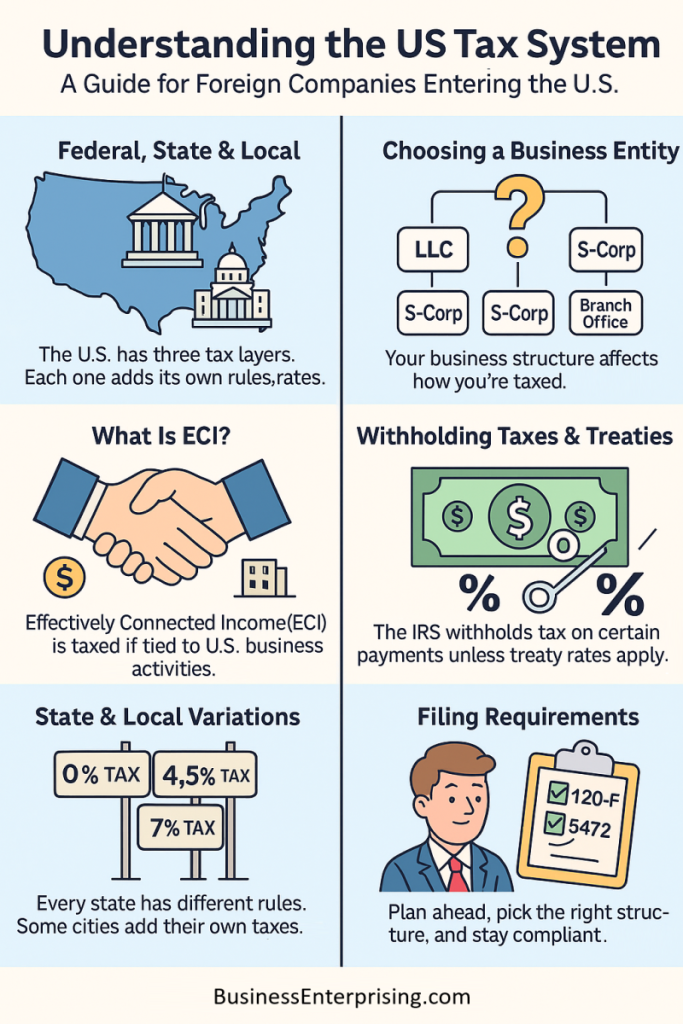

Expanding your business into the U.S. offers opportunity, but it also brings tax responsibilities. Understanding the US Tax System helps you avoid costly errors. Unlike some countries, the U.S. has separate tax rules at the federal, state, and local levels. Therefore, you need to prepare for more than just one set of obligations.

Expanding your business into the U.S. offers opportunity, but it also brings tax responsibilities. Understanding the US Tax System helps you avoid costly errors. Unlike some countries, the U.S. has separate tax rules at the federal, state, and local levels. Therefore, you need to prepare for more than just one set of obligations.

Additionally, your business structure affects how you’re taxed. Different rules apply to LLCs, corporations, and branch offices. Some entities pass income through to owners. Others pay corporate tax before issuing dividends. Therefore, choosing the right structure matters from the start.

Many foreign-owned businesses also face withholding tax on certain U.S. payments. However, tax treaties may reduce the rates. To claim a lower rate, you must file the right documents on time. Therefore, paperwork and planning are just as important as strategy.

State and local taxes can vary widely. Some states charge income tax. Others focus on sales, franchise, or property taxes. Additionally, many local governments add their own fees. These extra costs may affect your business location decision.

Filing deadlines and compliance requirements may feel overwhelming at first. However, missing them can lead to high penalties. It’s better to plan early and track obligations regularly. This helps you stay on good terms with tax authorities.

With the right approach, tax planning becomes part of your growth strategy. You don’t need to know every detail yourself. However, you do need to ask the right questions and seek the right help. That way, you can stay focused on building your business in the U.S.

Overview of the U.S. Tax Structure

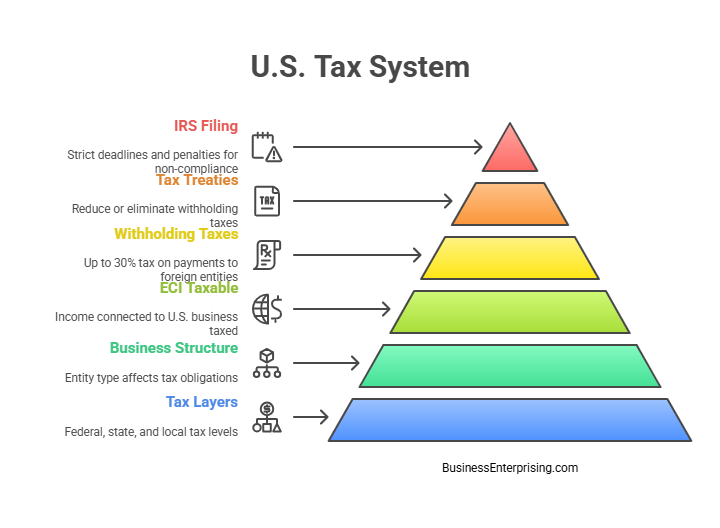

Understanding the US Tax System begins with knowing that taxes apply at three levels: federal, state, and local. Each layer adds its own set of rules. Unlike many countries that have one national tax system, the U.S. splits authority among different jurisdictions. This means your business might face several separate tax obligations at once.

At the federal level, most companies must pay income tax. The rate depends on your business type and profits. Additionally, the federal government may collect payroll taxes if you hire employees. These taxes help fund social programs such as Medicare and Social Security.

State taxes vary widely. Some states collect income tax, while others rely more on sales or franchise taxes. Therefore, where you choose to operate can significantly impact your total tax burden. Additionally, each state sets its own rules about what income is taxable and how it should be reported.

Local taxes add another layer. These can include city or county income taxes, property taxes, and even gross receipts taxes. While some locations keep local taxes low, others impose higher rates. Therefore, it pays to compare jurisdictions before forming your U.S. business entity.

Foreign companies are often surprised by this multi-layered approach. In many other countries, tax rules are centralized. However, in the U.S., you must comply with different authorities that may not coordinate with each other. This makes good planning even more important.

Although the system is complex, understanding it gives you more control. With careful setup and proper guidance, you can reduce your exposure to penalties. Additionally, you’ll be better prepared for growth and reporting. Understanding the US Tax System is an essential step toward operating legally and profitably in the American market.

Business Entity Types and Their Tax Implications

When forming a U.S. business, choosing the right structure affects how you’re taxed. Common options include LLCs, C-Corps, S-Corps, and branch offices. Each has pros and cons, depending on your goals and how you plan to operate. Understanding the US Tax System helps you avoid surprises and make informed choices.

An LLC, or Limited Liability Company, offers flexibility. By default, the IRS treats it as a pass-through entity. This means the profits pass to the owner and get taxed as personal income. However, you can elect corporate tax treatment if that suits your situation better. Many small businesses like this option due to the simpler setup and filings.

A C-Corp pays federal income tax on its profits. Then, shareholders pay tax again when they receive dividends. This double taxation can be a drawback. However, some foreign investors prefer C-Corps because ownership rules are broader and more flexible. Additionally, C-Corps can retain earnings for growth.

S-Corps are another type of pass-through entity, but they come with restrictions. Foreign owners generally cannot hold shares in an S-Corp. Therefore, most foreign companies avoid this option. Additionally, S-Corps have limits on the number and type of shareholders.

A branch office is not a separate legal entity. Instead, it operates as an extension of your foreign company. Therefore, the IRS taxes it on income effectively connected with a U.S. trade or business. Additionally, you may face a branch profits tax, which acts like a dividend tax.

Choosing a structure affects your tax filing, liability, and business flexibility. Therefore, take time to assess your needs and long-term plans. Understanding the US Tax System is not only about compliance. It also helps you make better decisions as you expand into the American market.

Federal Income Tax Obligations for Foreign-Owned Businesses

If your company is based outside the U.S. but does business within it, you may owe federal income tax. This depends on how your activities tie to income earned. The IRS taxes foreign companies only on what is considered effectively connected income, or ECI. Understanding the US Tax System starts with knowing what this means.

Effectively connected income refers to money made from business activities tied to a U.S. trade or business. This can include selling goods, providing services, or operating an office. Therefore, if your company has a strong presence in the U.S., it likely generates ECI. Additionally, ECI is taxed at the same rates as domestic companies.

However, passive income like dividends or royalties is not automatically considered ECI. These types of income often face a flat withholding tax instead. This rate depends on tax treaties between the U.S. and your home country. Therefore, you should review those agreements before making decisions.

If your company has ECI, you must file a federal tax return. This usually involves Form 1120-F. Additionally, the IRS expects accurate records of your income and expenses. Failing to report can lead to penalties or tax on gross income without deductions. Therefore, staying compliant is important for protecting your profits.

You may also face additional taxes, such as the branch profits tax. This tax applies if you operate as a branch instead of a U.S. subsidiary. Therefore, your business structure affects more than just paperwork.

Understanding the US Tax System helps you avoid mistakes and reduce risk. Additionally, it gives your company the ability to grow with more confidence. Proper planning helps you meet obligations without unexpected costs.

State and Local Tax Requirements

When expanding into the U.S., you must consider state and local taxes along with federal rules. Each state sets its own tax laws. Some states charge corporate income tax, while others rely more on sales or franchise taxes. Therefore, your location can significantly affect your costs.

Additionally, some states have no corporate income tax at all. However, these states may still collect other types of business taxes. Local governments can also impose taxes, including gross receipts or city income taxes. Therefore, the total tax burden varies widely from one area to another.

Understanding the US Tax System means knowing that your choice of state can impact profits. States like Delaware or Nevada attract businesses with friendly tax policies. However, other factors like workforce access and logistics also matter. You must weigh taxes against the full picture.

If you open offices or warehouses in multiple states, you may create tax obligations in each. This is called nexus. Therefore, tracking where you operate matters. Additionally, online sales may trigger tax rules in states where you have no physical presence.

Some localities add extra taxes on top of state requirements. These may include property taxes, licensing fees, or payroll-based taxes. Therefore, research your specific city or county before finalizing your location.

You can often reduce costs by choosing a tax-efficient state. However, tax rates are only one part of the decision. Additionally, state filing requirements vary. Some states require annual reports or estimated payments throughout the year.

Understanding the US Tax System helps you plan ahead and reduce risk. A thoughtful approach to location gives you a better foundation for growth. Additionally, it helps you avoid unexpected expenses later on.

Withholding Taxes and International Treaties

When a U.S. company pays a foreign business, it may need to withhold taxes from the payment. This typically applies to passive income. Common examples include dividends, royalties, and interest. By law, the default withholding rate is 30 percent. However, that rate can change under certain conditions.

The IRS expects the U.S. payer to withhold the correct amount. Therefore, you may not receive the full payment unless proper documentation is submitted. Additionally, the payer must report the payment and withholding to the IRS. Mistakes here can lead to penalties for both parties.

Fortunately, tax treaties between the U.S. and other countries can lower or eliminate this tax. These agreements set special rules for cross-border payments. Therefore, your withholding rate may drop to 15 percent, 5 percent, or even zero. However, the treaty benefit is not automatic.

To claim a reduced rate, you must submit the correct IRS forms. One common example is a W-8BEN or W-8BEN-E. These forms tell the IRS about your status and treaty eligibility. Additionally, the forms must be updated regularly to stay valid.

Understanding the US Tax System helps you keep more of what you earn. Withholding taxes can take a large bite out of revenue. Therefore, applying the right treaty terms can make a big difference. It also helps avoid delays and disputes with U.S. clients.

Additionally, some treaties offer more favorable terms than others. Where your business is based may impact your tax outcomes. Therefore, it’s worth checking how your home country treaty compares. Proper planning can help you avoid unnecessary tax costs from the start.

Filing Requirements and Common Compliance Challenges

When your foreign-owned company operates in the U.S., you must meet specific IRS filing rules. These requirements depend on your structure and activity. For example, if you form a U.S. entity with at least 25 percent foreign ownership, you may need to file Form 5472. This form reports certain transactions between the U.S. company and its foreign owner. Additionally, the IRS requires this form even if your company has no income.

If your business operates as a branch instead of a subsidiary, you may need to file Form 1120-F. This form applies to foreign corporations with income effectively connected to a U.S. trade or business. Therefore, your structure affects which forms you must submit. Filing deadlines usually follow the same calendar as domestic corporations. However, foreign businesses can request extensions in some cases.

Missing a deadline or filing incomplete information can trigger steep penalties. The IRS charges thousands of dollars for late or missing forms. Therefore, small filing errors can lead to big financial consequences. Additionally, the IRS may deny deductions or tax credits if you miss required forms.

Understanding the US Tax System helps you avoid these problems. Filing on time keeps your business in good standing. It also builds trust with U.S. clients and partners. Additionally, proper records make it easier to respond if the IRS asks questions.

Foreign companies often struggle with unfamiliar rules or miscommunication. Therefore, it’s smart to review filing requirements early in the year. That way, you’ll have time to collect the right data and avoid last-minute mistakes. Proper compliance helps you stay focused on growth, not paperwork.

Conclusion

Expanding into the U.S. brings opportunity, but it also adds complexity. Tax rules are not always easy to understand or apply. However, with the right approach, your business can stay compliant and avoid costly mistakes. Understanding the US Tax System is one of the first steps toward long-term success.

Additionally, each part of the system connects to another. Your business structure affects your tax filings. Your location changes what taxes you owe. Therefore, your early decisions shape your future costs. By thinking ahead, you can save money and reduce your risk of penalties.

Federal rules may seem clear, but state and local taxes can add extra layers. Therefore, it’s important to research before selecting your business address. Additionally, tax treaties may reduce your withholding obligations. However, you must file the right forms to benefit from them.

Filing requirements come with strict deadlines. Late submissions often lead to automatic penalties. Therefore, keeping good records and filing on time matters. You don’t want tax issues to distract you from running your business.

Understanding how taxes apply to foreign companies helps you plan better. Additionally, it helps you work more smoothly with clients, banks, and vendors. A good tax strategy supports both your growth and your credibility.

Although the system has many parts, you don’t have to handle it alone. Advisors and accountants can help you avoid common errors. Therefore, consider seeking help before tax problems arise. Doing so will save you time, money, and stress in the long run.