Running a business involves more than providing a product or service. It also means managing risk. Business insurance helps protect you when something goes wrong. Whether it’s a lawsuit, property damage, or employee injury, coverage can keep your business from losing everything.

Running a business involves more than providing a product or service. It also means managing risk. Business insurance helps protect you when something goes wrong. Whether it’s a lawsuit, property damage, or employee injury, coverage can keep your business from losing everything.

Additionally, many clients, landlords, and lenders require proof of insurance before doing business with you. Therefore, carrying the right policy makes you more credible. It shows you’re serious about protecting your operation and those you work with.

However, choosing insurance is not always simple. Different business types need different coverage. What works for one company might not fit another. Therefore, you need to understand what applies to your industry, location, and size.

The goal is to protect your time, income, and assets. That means asking the right questions and reviewing your policies often. Additionally, knowing which coverage types matter can help you avoid overspending. It also helps you prepare for the unexpected.

Many owners put off buying insurance until they face a loss. By then, it’s too late. Planning ahead gives you more options and fewer surprises. Therefore, taking the time to review your risk and compare policies makes a real difference.

This guide breaks down what you need to know. You’ll learn which types of coverage matter most, how to assess your needs, and when to make updates. With the right plan, you can focus on growth instead of guessing what might go wrong.

Why Business Insurance Is Non-Negotiable

Running a business comes with risks. Property damage, lawsuits, and employee injuries are all possibilities. Without protection, a single event could wipe you out. That is why having business insurance is necessary for even the smallest operation. It helps you absorb shocks that would otherwise derail your entire company.

Additionally, many industries require insurance to remain compliant. Local laws, contracts, and client agreements often demand specific coverage. Therefore, skipping insurance can lead to fines or lost deals. Even if no one asks for proof, the risk of operating without it is still too high.

Some owners believe they are too small to be sued or impacted. However, claims can happen regardless of size. A slip-and-fall on your property or a missed service deadline could lead to a costly dispute. Business insurance gives you the resources to respond without draining your savings.

Furthermore, lenders and landlords often require proof of insurance. They want to know that your operation can survive setbacks. Without coverage, they may not do business with you. That can slow growth and limit your opportunities.

Each year brings new changes to how you work. As your company grows, so do your risks. Therefore, keeping the right insurance in place protects everything you’ve built. Business insurance is not a luxury. It is a basic part of staying operational and financially stable. Skipping it is not worth the risk.

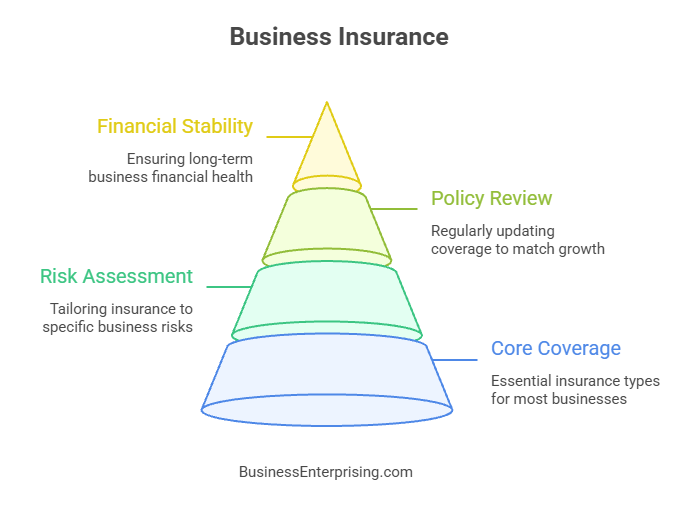

The Core Types of Business Insurance Every Owner Should Know

There are several types of business insurance, but five are considered essential for most small businesses. Each serves a different purpose and covers specific risks. Understanding what they do can help you choose the right protection for your company.

General liability insurance protects you when someone claims your business caused injury or property damage. For example, a customer slipping in your store could lead to a lawsuit. This type of coverage helps pay for legal costs and damages.

Property insurance covers damage to your building, equipment, or inventory. If a fire, theft, or storm hits, this coverage helps you recover. Therefore, it’s important even if you work from a small office or own little inventory.

Workers’ compensation insurance supports your employees if they get injured on the job. It helps with medical bills and lost wages. Additionally, many states require this coverage as soon as you hire staff.

Professional liability insurance, also called E&O, is useful for service-based businesses. If a client claims your advice or services caused them harm, this coverage applies. Therefore, it’s helpful for consultants, agencies, and professionals offering expertise.

Cyber insurance covers losses related to data breaches and cyberattacks. If your systems are hacked or customer data is exposed, this can help pay for recovery. Additionally, it helps cover notification costs and legal fees that may follow a breach. Each of these policies plays a part in keeping your business stable. Therefore, choosing the right business insurance mix protects your time, money, and reputation.

How to Assess Your Insurance Needs Based on Your Business Model

Every business carries risk, but not all businesses face the same kind. That is why you need to tailor your insurance decisions. Start by thinking about what type of work you do. A service-based business faces different threats than a company that sells physical products.

For example, if you offer professional advice, a client might sue over a mistake. Therefore, professional liability coverage should be a priority. On the other hand, if you sell goods, you may need product liability insurance. A defect or recall can lead to claims that are expensive to settle.

Additionally, your size matters. A business with one person needs less coverage than a company with several employees. If you have staff, then workers’ compensation is likely required. It also protects you from paying directly for work-related injuries.

Your location also affects your risk. Some areas have a higher chance of natural disasters, theft, or legal claims. Therefore, your zip code might influence your coverage choices. Business interruption insurance can also be useful in places where long closures are more likely.

Handling customer data adds another layer. If you store sensitive information, cyber insurance should be part of your plan. Even one data breach can result in major financial loss. Additionally, many clients expect data security measures, including insurance. Business insurance should match your real exposure, not a generic checklist. Therefore, take time to review how your business operates. That approach leads to smarter coverage decisions and fewer surprises later.

What Business Owners Often Overlook (and Regret Later)

Many business owners buy basic coverage but skip important policies they think they won’t need. That decision often leads to regret. One commonly missed type is business interruption insurance. If a fire or storm forces you to shut down, this coverage helps replace lost income. Without it, you might struggle to cover rent, payroll, or other bills while closed.

Product liability is another blind spot. If something you sell causes harm, you could face a lawsuit. Even if the product worked as designed, claims still happen. Therefore, any business that makes, sells, or distributes goods should consider this coverage. Settlements can be large and often aren’t covered by general liability policies.

Additionally, many owners ignore employment practices liability insurance. EPLI helps if an employee sues over discrimination, harassment, or wrongful termination. These claims are expensive to defend and can damage your reputation. As you grow your team, the risk grows with it.

Therefore, the coverage you skip often ends up being the one you need. Business insurance should address what might go wrong, not just what seems likely. Also, contract requirements and client expectations change over time. That makes it even more important to fill any gaps.

No policy can cover everything, but missing the right ones creates bigger problems. Reviewing your coverage regularly helps avoid those gaps. Therefore, look beyond the basics and think about where your risks really lie. Planning ahead protects more than your money. It protects your ability to keep going.

How to Choose the Right Provider and Policy Without Overpaying

Choosing the right business insurance provider can save you money and protect you from surprises. Start by comparing quotes from several companies. Price matters, but so does what each policy actually covers. A low premium may leave out key protections you need.

Additionally, review the exclusions. These are the situations your policy won’t cover. Many business owners skip this part and find out too late. Therefore, always read the fine print. If you don’t understand something, ask for a clear explanation before you sign.

Working with a licensed broker or agent can help, especially if you run a complex business. However, not all brokers offer the same value. Some work for specific insurers while others are independent. Ask how they get paid and who they represent before taking advice.

Also, check the financial strength and customer service record of the company. You want a provider that pays claims fairly and on time. If they are hard to reach now, they might be worse when you need them later.

Therefore, take your time and compare not just cost but also reputation and coverage. Additionally, revisit your policy once a year. Business needs change and your coverage should keep up. A little homework now can prevent big problems later.

Smart planning starts with asking the right questions. Business insurance is not all the same, and the wrong choice can be expensive. Make sure the policy you pick protects your business without wasting money on coverage you don’t need.

When to Review and Update Your Coverage

Your business is not the same year after year. As you grow, your risk changes too. Therefore, your insurance needs regular attention. A policy that worked last year might not cover you now.

For example, if you hire employees, add new services, or move locations, that’s a clear signal to review coverage. Each change can affect your exposure. Additionally, buying new equipment or expanding your space might require updates to property protection.

Business insurance should reflect your current operations, not your original business plan. If you added digital tools or started collecting customer data, cyber coverage might now be necessary. Therefore, staying current with your policies protects you from costly gaps.

Conducting an annual insurance audit is a smart habit. Set a time each year to meet with your agent or broker. During that review, ask questions, confirm coverage limits, and discuss any planned changes. Also, request a copy of your policy and read it with care.

Small changes can lead to major claims. For example, hiring your first employee without adding workers’ comp could become a legal problem. Therefore, never assume a policy still fits without checking. Growth is good, but protection must grow with it. Keeping your business insurance updated helps you stay ready for whatever comes next. Additionally, it shows lenders and clients that you run a responsible operation. Take the time to review before you need to file a claim.

Conclusion

Running a business comes with responsibilities, and protecting what you build should be part of your plan. Business insurance gives you a safety net when things go wrong. It also shows your clients and partners that you take your work seriously.

Additionally, the right policy can help you avoid major financial loss. One incident, claim, or disaster can set you back for years. Therefore, it makes sense to treat your insurance coverage as part of your business operations, not an afterthought.

Reviewing your risks, choosing the right provider, and updating your coverage are all steps that support long-term stability. Many owners only think about insurance when they need it. However, by then it may be too late to fix the problem. Taking a proactive approach protects your money, time, and reputation.

Each year, set aside time to review your coverage. Ask yourself what changed and what needs more protection. Additionally, speak with an advisor if you feel unsure. A good conversation today can prevent a major headache tomorrow.

Business insurance does more than check a box. It supports your ability to stay open and keep growing. Therefore, think of it as an investment in the future of your company. With the right plan in place, you’ll have fewer worries and more control.