Applying for business loans can be an important step in achieving your company’s goals. Whether you need funds for expansion, equipment, or cash flow management, understanding the process is key. With many options available, choosing the right loan requires careful planning and research.

Applying for business loans can be an important step in achieving your company’s goals. Whether you need funds for expansion, equipment, or cash flow management, understanding the process is key. With many options available, choosing the right loan requires careful planning and research.

Preparation is essential to increasing your chances of approval. Lenders often evaluate factors like creditworthiness, cash flow, and business plans. By organizing your financial documents and defining your borrowing needs, you can create a compelling application that stands out.

Navigating the loan process may seem challenging, but knowing what to expect can make it manageable. With the right approach, you can secure funding to support your business’s growth and success. Taking the time to prepare will help you find the best option for your specific needs.

Understanding Different Types of Business Loans

Understanding the different types of business loans is essential when you’re exploring funding options for your company. Term loans are one of the most common types. These loans provide you with a lump sum of money that you repay over time with interest. They are a great choice if you need funds for long-term investments like expansion or equipment.

SBA loans are another popular option, especially for small businesses. These loans are backed by the U.S. Small Business Administration, offering lower interest rates and longer repayment terms. They are ideal if you’re looking for affordable financing and meet the eligibility criteria. SBA loans, however, often require more documentation and a longer approval process.

A line of credit gives you flexible access to funds up to a specified limit. This type of loan works well for managing cash flow or covering short-term expenses. You can borrow only what you need and repay it, often with lower interest than credit cards. This flexibility makes it a popular choice for businesses that experience seasonal fluctuations.

Equipment financing is specifically for purchasing or leasing equipment. The equipment itself usually serves as collateral for the loan. This option is useful if you want to preserve working capital while upgrading tools or machinery. When applying for business loans, understanding which loan type fits your needs helps you make informed decisions and choose the best option for your situation.

Key Factors Lenders Consider When Reviewing Loan Applications

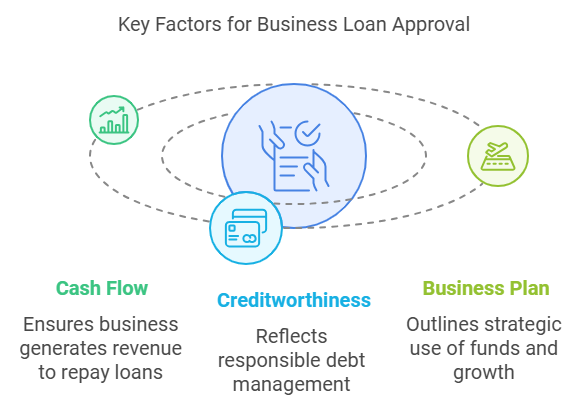

When applying for business loans, understanding what lenders consider can improve your chances of approval. One key factor is cash flow. Lenders review your financial statements to ensure your business generates enough revenue to repay the loan. Maintaining consistent cash flow demonstrates financial stability and reassures lenders about your ability to meet obligations.

Creditworthiness is another important aspect. Both your personal and business credit scores play a role in the approval process. A strong credit history shows that you manage debt responsibly and reduces the risk for lenders. Paying bills on time and minimizing outstanding debts can improve your credit score before applying.

A clear and detailed business plan is also essential. Lenders want to see how you plan to use the funds and achieve your goals. A well-prepared plan outlines your business model, target market, and projected growth. It also shows lenders that you’ve thought through your strategy and have a path to success.

By addressing these factors, you can present a strong case when applying for business loans. Preparing your financial documents, improving your credit, and crafting a solid business plan all demonstrate reliability. These steps help build confidence with lenders and increase the likelihood of securing funding.

Preparing Your Business for a Loan Application

Preparing your business for a loan application is essential to improving your chances of approval. Start by organizing your financial documents. Lenders often request tax returns, profit and loss statements, and balance sheets. Having these records ready helps streamline the application process and demonstrates your professionalism.

Improving your credit score is another important step. Lenders review both your business and personal credit scores to assess risk. Paying down outstanding debts and resolving any errors on your credit report can make a significant difference. A higher credit score increases the likelihood of getting favorable terms.

Assessing your borrowing needs is also critical before applying for business loans. Clearly define the purpose of the loan, whether it’s for expansion, equipment, or working capital. Understanding how much funding you need prevents overborrowing and helps you choose the right loan type. This clarity also shows lenders that you have a well-thought-out plan.

By taking these steps, you present yourself as a reliable borrower and increase your chances of approval. Preparing in advance saves time and reduces stress during the loan process. When you’re ready, you can confidently move forward with applying for business loans that support your goals.

How to Choose the Right Lender for Your Business

Choosing the right lender is a key step when applying for business loans. Different types of lenders offer unique benefits, so it’s important to evaluate them carefully. Banks are often a good choice if you want competitive interest rates and long-term stability. However, their approval processes can be more time-consuming and may require a strong credit history.

Credit unions are another option to consider. They often provide lower fees and a more personalized approach to lending. This makes them appealing if you value customer service and flexibility. Credit unions may also have less stringent requirements compared to traditional banks, which can benefit smaller or newer businesses.

Online lenders offer speed and convenience, making them a popular choice for businesses needing quick access to funds. Many online platforms have streamlined applications with faster approvals. While their interest rates may be higher than those of banks or credit unions, they often serve borrowers who may not qualify for traditional loans.

When applying for business loans, consider how each lender aligns with your business goals and financial situation. Compare interest rates, repayment terms, and fees to find the best fit. Taking the time to evaluate your options ensures that you choose a lender who supports your success.

Tips for Writing a Strong Loan Application

Writing a strong loan application is essential when applying for business loans. Start by clearly stating the purpose of the loan. Explain how the funds will be used to grow or stabilize your business. Whether it’s for new equipment, expansion, or working capital, providing a detailed explanation shows lenders your commitment and planning.

Include a realistic repayment strategy that aligns with your cash flow. Lenders want to see how you intend to manage repayments without straining your business. Providing clear projections and repayment timelines demonstrates your financial awareness. Highlighting consistent revenue or growth trends can further reassure lenders of your ability to repay.

A professional and well-organized application leaves a positive impression. Double-check all submitted documents for accuracy, including financial statements and credit reports. Include a compelling business plan that outlines your goals, market strategy, and expected outcomes. This adds depth to your application and shows you’ve thoroughly considered how the loan will impact your business.

When applying for business loans, crafting a strong application sets you apart from other applicants. A clear purpose and repayment strategy, combined with organized documentation, create a persuasive case. Taking the time to prepare your application carefully increases your chances of approval and builds trust with lenders.

Common Challenges and Mistakes to Avoid

When applying for business loans, it’s important to avoid common challenges that can delay or derail your application. One of the biggest mistakes is overborrowing. Asking for more than you need can lead to higher monthly payments and unnecessary financial strain. Carefully calculate how much funding is required to achieve your goals without taking on excessive debt.

Misunderstanding loan terms is another frequent issue. It’s essential to review interest rates, repayment schedules, and any fees associated with the loan. Neglecting to read the fine print can result in unexpected costs or penalties. If you’re unsure about the terms, take the time to ask questions and clarify details with your lender.

Failing to prepare thoroughly for the approval process can also hurt your chances. Lenders often request financial documents, credit histories, and business plans to assess your application. Submitting incomplete or inaccurate information can delay approval or even lead to rejection. Preparing these materials in advance helps you present a strong and organized application.

By recognizing these pitfalls and taking steps to avoid them, you improve your chances of a smooth loan process. Applying for business loans successfully requires careful planning, clear communication, and a thorough understanding of the terms. Avoiding these mistakes helps you secure the funding you need to grow your business with confidence.

Conclusion

Applying for business loans can be a valuable step in growing or stabilizing your business. By understanding loan options, preparing thoroughly, and choosing the right lender, you improve your chances of success. A well-organized application with a clear purpose and repayment strategy shows lenders you’re serious and reliable.

Avoiding common mistakes like overborrowing or misunderstanding terms helps you secure funding without unnecessary risks. Taking the time to prepare financial documents and assess your needs builds confidence during the approval process. These efforts ensure your application stands out and meets lender expectations.

By following these strategies, you can approach the loan process with confidence. Applying for business loans doesn’t have to be overwhelming when you’re informed and prepared. With careful planning, you can secure the funding your business needs to achieve its goals and thrive.