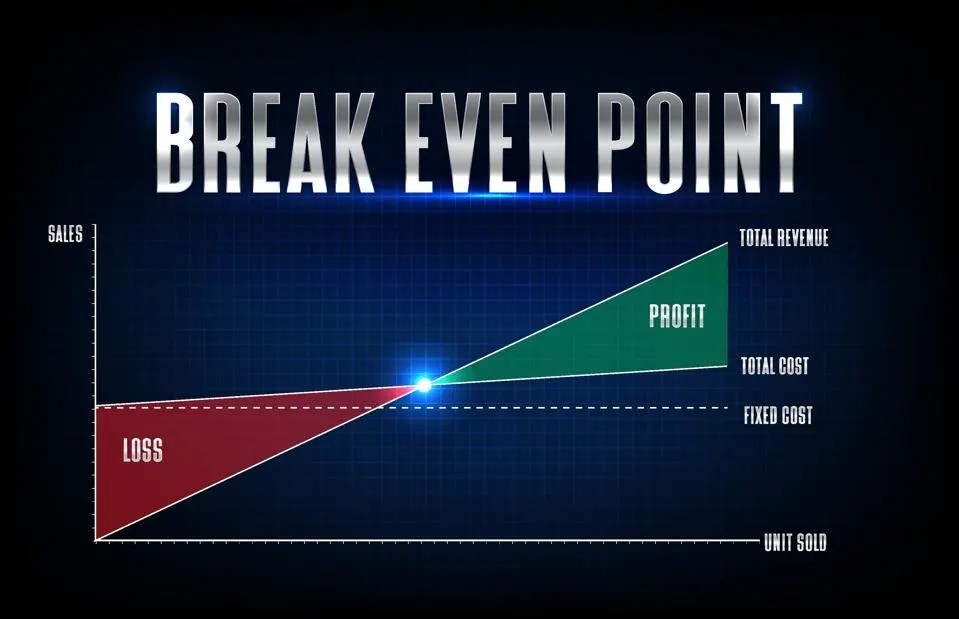

Conducting a break-even analysis is crucial for businesses to evaluate financial health, set goals, and plan for growth. The break-even point, where total revenue equals total costs, indicates when a business moves from loss to profit. This analysis helps businesses determine the minimum performance needed to cover costs, aiding in better decision-making.

What is Break-Even Analysis?

A break-even analysis is the process of determining the sales volume or revenue needed to cover both fixed and variable costs. Fixed costs, such as rent, salaries, and utilities, remain constant regardless of production or sales volume. Variable costs, including raw materials and labor, fluctuate based on output. By conducting a break-even analysis, a business can assess how many units it must sell or how much revenue it needs to break even and avoid losses.

This method is commonly used by businesses to evaluate pricing strategies, determine profit margins, and forecast financial sustainability. It’s a critical part of the financial planning process, whether you’re launching a new product, expanding your operations, or reevaluating your pricing model. Understanding how to apply break-even analysis helps businesses stay ahead of financial pitfalls.

The Importance of Conducting a Break-Even Analysis

Conducting a break-even analysis provides businesses with valuable insights that influence key decision-making. One of the main reasons to conduct this analysis is to gauge financial feasibility. By understanding exactly how many sales are required to cover costs, businesses can avoid underpricing products or overestimating market demand. For new businesses or startups, this analysis is crucial in setting realistic expectations about profitability.

Additionally, break-even analysis helps businesses make informed decisions about product pricing. For instance, if a business is unsure whether its pricing model is viable, it can perform a break-even analysis to ensure that the price covers all costs and contributes to profit. Without this analysis, companies may risk setting prices too low, leading to financial losses, or too high, alienating potential customers.

How to Calculate Break-Even Point

The break-even point can be calculated using a straightforward formula:

The break-even point is calculated by dividing the total fixed costs by the difference between the selling price per unit and the variable cost per unit. In other words, it shows how many units a business needs to sell for the revenue from sales to exactly cover all fixed and variable costs. Any sales beyond this point result in profit, while sales below this point result in a loss.

![]()

This formula divides fixed costs by the contribution margin, which is the difference between selling price and variable cost. The result shows how many units must be sold to break even. For example, if fixed costs are $20,000, the selling price is $100, and variable costs are $40, selling 333 units will break even.

This formula can also calculate break-even revenue instead of units. Multiply the break-even units by the selling price to find the break-even revenue. This approach helps businesses selling services or products with varying prices.

Using Break-Even Analysis to Set Pricing Strategies

One of the primary applications of break-even analysis is setting and adjusting pricing strategies. Pricing is one of the most critical factors in a business’s success, and conducting a break-even analysis ensures that the price charged to customers will cover all associated costs. When experimenting with new prices or discounts, the break-even point can help businesses decide if the adjusted pricing will still lead to profitability.

For example, a business may want to test the effects of lowering prices to attract more customers. Conducting a break-even analysis helps determine if the lower price would require significantly more units to be sold to cover the same costs. This insight allows businesses to adjust pricing while balancing sales volume and profitability.

Forecasting Profitability and Planning Growth

Break-even analysis is invaluable when businesses are planning to expand or introduce new products. By understanding the break-even point, businesses can set realistic sales targets and revenue goals. This tool provides a clear financial picture, allowing companies to plan for scaling operations or entering new markets with a solid grasp of the required sales volume to cover additional costs.

Moreover, break-even analysis helps businesses identify areas where they can reduce costs. If the break-even point is too high, it may signal that the business needs to lower fixed or variable costs to achieve profitability. By continuously evaluating cost structures through break-even analysis, businesses can improve efficiency and focus on profitable growth.

Scenarios for Conducting a Break-Even Analysis

Several business scenarios benefit from conducting a break-even analysis:

Launching a New Business or Product: When starting a new business, understanding the break-even point ensures that entrepreneurs know how much they need to sell to cover initial costs. This analysis also guides them in setting a competitive price for their products.

Expanding into New Markets: If a business is considering expansion, it will face new fixed and variable costs. Break-even analysis helps businesses determine how much additional revenue they need to generate to cover these costs and assess expansion feasibility.

Adjusting Business Models: Businesses may choose to shift their operational model, such as moving from retail to e-commerce. Conducting a break-even analysis helps forecast the impact of these changes on profitability by identifying new costs and sales requirements.

Evaluating Discounts or Promotions: Before launching promotions or discounts, businesses can use break-even analysis to evaluate whether the reduced price will still cover the cost of production and overhead.

Optimizing Costs and Improving the Break-Even Point

If a break-even analysis shows that a business needs to sell more units than is feasible, there are two ways to improve the break-even point. One option is to reduce fixed or variable costs. For example, finding more affordable suppliers or improving production processes can lower the variable cost per unit. By reducing expenses, businesses can lower the number of sales required to break even.

The other option is to raise prices, though businesses must do this carefully to avoid alienating customers. Raising the price reduces the number of units required to reach the break-even point, but it may lower sales volume. Businesses must balance these adjustments carefully, considering customer expectations and market demand.

Conducting a break-even analysis is a vital practice for any business, whether it is just starting or looking to expand. It offers insights into pricing, sales targets, and cost management, allowing businesses to make data-driven decisions. Understanding the break-even point helps businesses avoid financial pitfalls, manage resources effectively, and achieve sustainable profitability.

By mastering break-even analysis, businesses can confidently set prices, plan expansions, and optimize costs. As markets evolve and competition increases, this tool remains indispensable for business owners seeking long-term financial success.