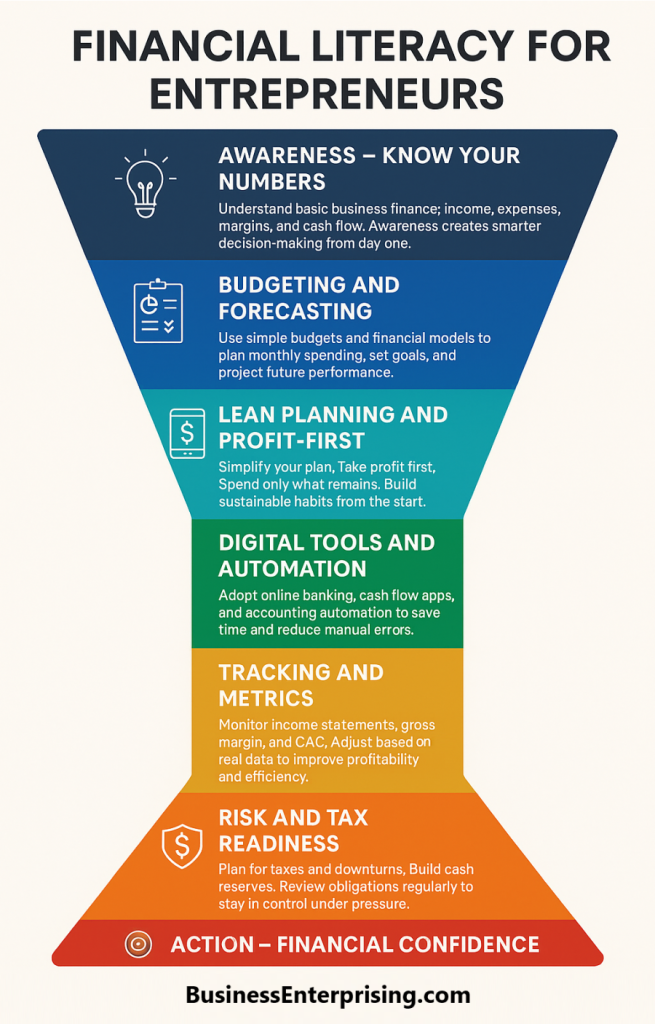

Running a business without financial literacy puts you at a disadvantage. You may bring in revenue, but struggle to keep profit. Many entrepreneurs focus on growth and ignore the numbers. That can lead to stress, debt, or missed opportunities. Understanding your finances helps you stay ahead and make better decisions.

Running a business without financial literacy puts you at a disadvantage. You may bring in revenue, but struggle to keep profit. Many entrepreneurs focus on growth and ignore the numbers. That can lead to stress, debt, or missed opportunities. Understanding your finances helps you stay ahead and make better decisions.

Additionally, money habits shape your success. When you set budgets, track results, and plan for taxes, you avoid common setbacks. These habits reduce guesswork and help you use resources wisely. Therefore, it makes sense to treat your finances like any other part of your business strategy.

You do not need to become an accountant. However, you do need to know what your numbers mean. Your income, costs, and margins tell you what to fix or improve. That kind of insight supports steady growth. It also helps you stay calm during busy or slow seasons.

Financial tools have also improved. You can now use apps to monitor spending, automate tasks, and spot trends early. Additionally, you can outsource parts of the process without losing visibility. When your systems are clear, you stay focused on what matters most. If you take time to build better habits, the benefits last. With the right approach, you can grow your business and protect your peace of mind.

Budgeting, Forecasting, and Financial Modeling for Online Business

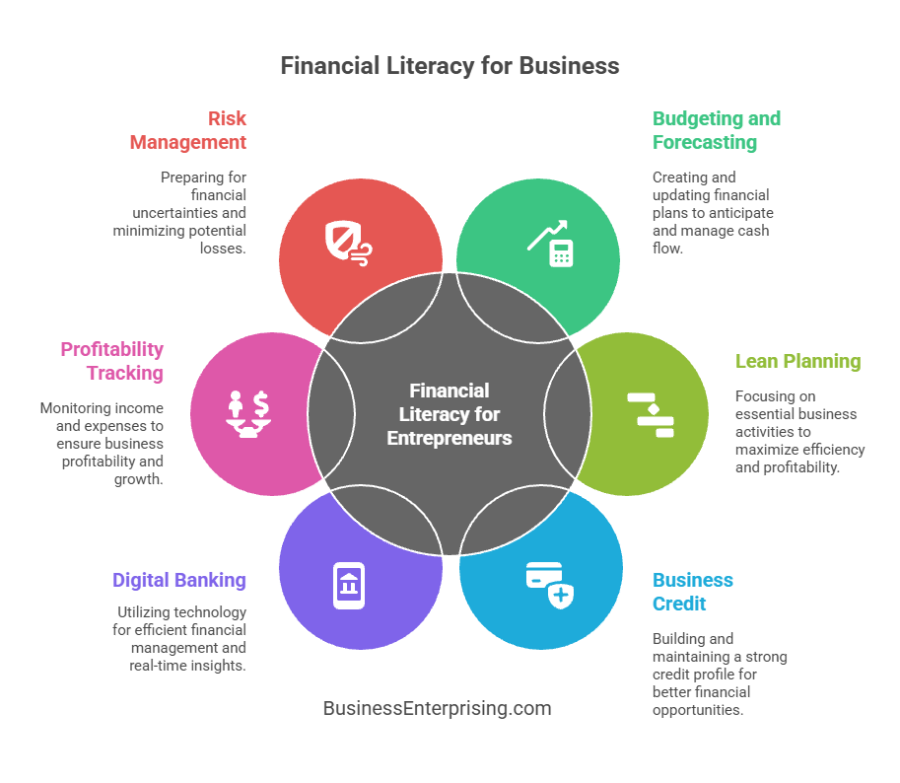

Running an online business means tracking numbers that change fast. Sales shift, costs rise, and platforms update without warning. That makes budgeting and forecasting essential. You need clear projections to make smart spending decisions and avoid cash problems. Your plan doesn’t have to be perfect, but it does need to stay current.

Additionally, forecasting helps you prepare for seasonal trends and product cycles. You can set sales goals based on real data instead of guessing. When you update your forecasts often, you stay flexible. That flexibility helps you adjust your plans without losing momentum.

Financial models give you a broader view of what’s working. They combine revenue, costs, and growth into one clear picture. Therefore, you can test new ideas before spending money. A solid model helps you make smarter moves with less risk. It also shows what’s possible if key numbers change.

Budgeting ties it all together. You assign every dollar a purpose and track how well you stick to it. This helps you stay focused on goals instead of chasing trends. Additionally, you can review where you over- or under-spend. Those reviews guide better choices moving forward.

Financial literacy means more than reading spreadsheets. It’s about knowing what your numbers mean and how they shape your business decisions. With the right tools and a consistent process, you can stay ahead without feeling overwhelmed.

Lean Planning and the Profit-First Mindset

Running lean means staying focused on what matters. You plan based on real numbers, not wishful thinking or long reports. Lean business planning helps you cut the noise and keep your goals clear. You write down what you offer, how you make money, and what it costs to operate.

Additionally, a lean plan helps you move fast. You can test ideas without overcommitting time or money. When something works, you build on it. When it fails, you pivot without losing control. That flexibility helps you adapt and stay competitive without burning through your resources.

The profit-first mindset flips the usual formula. Instead of income minus expenses equaling profit, you take profit first. Therefore, you limit what you can spend and keep your margins protected. This approach creates healthy habits early. It also forces you to rethink where your money goes.

You don’t need complex software to do this. You can start with separate accounts for profit, taxes, and operating costs. Additionally, you can review those balances each month. That process shows you how your business is really doing, not how it feels.

Financial literacy helps you apply both models with confidence. When you understand your numbers, you make better decisions. You also avoid the trap of chasing revenue without real gain. Lean planning and a profit-first mindset help you grow without chaos.

Understanding Business Credit and Funding Options

Building business credit gives you more financial options. It separates your business from your personal credit profile. That separation protects you as your business grows. You start by opening business accounts and paying bills on time. Over time, you build a score lenders can trust.

Additionally, strong business credit helps you qualify for better terms. You can access lines of credit, loans, or vendor financing without relying on personal guarantees. That flexibility supports your operations without adding risk. However, you still need to review each funding offer carefully.

Each tool works differently. Some loans offer quick access but carry higher interest. Others require strong credit but offer longer terms. Therefore, you should compare total repayment costs, not just the monthly payment. Make sure the funding helps your business grow, not stall it.

Also, think about timing. You do not want to borrow when your cash flow is already tight. Instead, plan ahead so funds are available when needed. Additionally, consider how each loan affects ownership. Some financing options may require equity, while others keep you in full control. Financial literacy helps you use credit wisely. When you understand your terms and plan your spending, debt becomes a tool, not a problem. Credit can support growth, but only if you treat it like a strategy.

Using Digital Banking and Fintech for Business Finance

Managing business money takes more than a spreadsheet. You need real-time tools that keep up with daily transactions and decisions. Digital banking platforms help by offering accounts built for business owners. These platforms work online and give you fast access to your balances, payments, and transfers.

Additionally, many fintech tools connect directly to your bank accounts. You can use cash flow apps to track income and expenses automatically. This gives you better visibility without manual work. Therefore, you spend more time running your business and less time fixing your books.

Automation also plays a key role. You can schedule recurring payments, set alerts, and categorize expenses without lifting a finger. That makes month-end reviews faster and more accurate. It also helps prevent missed bills or late fees. When your systems talk to each other, your records stay current.

Fintech also supports better forecasting. You can track trends, compare months, and review margins at any time. Additionally, some platforms offer dashboards that summarize everything in one view. These snapshots help you make quick, informed choices. That kind of speed matters when cash flow gets tight.

Financial literacy now includes knowing how to use digital tools. If you understand how each platform fits into your process, you reduce errors and save time. Small steps in automation add up fast. Over time, they make your financial systems more stable and efficient.

Tracking Profitability and Operational Efficiency

Profitability shows whether your business actually makes money. To track it well, you need to review your income statement regularly. This report shows your total revenue, cost of goods sold, and expenses. Each number tells a story about how your business performs.

Gross margin is one key number. It shows the percentage of revenue left after subtracting direct costs. Therefore, a strong margin means your business has room to cover overhead and still profit. Additionally, you should track your variable costs. These rise or fall with sales, so they affect your bottom line every month.

Customer acquisition cost, or CAC, is another useful metric. It tells you how much you spend to get each new customer. When CAC is lower than the revenue from that customer, you are on the right track. However, if CAC keeps rising, you may need to adjust your marketing or pricing.

Operational efficiency comes from cutting waste and simplifying your process. That does not mean doing everything yourself. It means reviewing each step for value. Additionally, you should look at fulfillment times, software use, and labor costs. Small changes here often create big savings over time.

Financial literacy helps you connect the numbers to daily decisions. When you know where your money goes and how your efforts pay off, you lead with purpose. Profit isn’t a mystery. It’s a result of clear thinking and regular review.

Financial Risk Management and Tax Planning

Tax planning should not be an afterthought. You need to plan for tax obligations throughout the year, not at the last minute. Set aside a percentage of your income each month to avoid surprises. This simple habit can prevent cash flow issues and penalties.

Additionally, managing financial risk helps you stay stable during slow periods. Every business faces unexpected expenses or seasonal drops. Therefore, you should build a reserve fund to cover at least one or two slow months. These savings give you more control when revenue dips or costs spike.

You can also reduce tax liability with careful tracking. Keep accurate records of business expenses, tools, and subscriptions. Many of these can lower your taxable income. Therefore, reviewing your numbers often helps you make better decisions before year-end. Planning early gives you more options and less stress.

Financial literacy means understanding how taxes and risk affect your operations. If you treat taxes like a monthly bill, you stay prepared. Additionally, regular reviews of your cash flow help you adjust spending as needed. This kind of planning protects your margins and avoids unnecessary debt. No business avoids risk, but you can prepare for it. With the right systems, your taxes and reserves become part of your long-term strategy. Small habits like saving and tracking lead to big improvements over time.

Conclusion

Running a business requires more than selling a product or service. You also need to understand how your money works. When you track income, manage costs, and plan for taxes, you avoid many common setbacks. These habits give you more room to grow without extra stress.

Additionally, financial systems help you scale without confusion. Budgeting, automation, and forecasting create structure behind the scenes. That structure supports clear decisions and fewer surprises. Therefore, you stay focused on your goals instead of reacting to problems. Small adjustments in your process often lead to bigger results over time.

Your financial tools should match your business size and needs. You don’t need complicated software to start. However, you do need consistency. Monthly reviews and simple reports can show you what’s working. They also highlight where you can save or reinvest. That feedback supports stronger planning in the months ahead.

Financial literacy gives you control. It helps you see what’s ahead and adjust before problems grow. Additionally, it keeps your focus on what matters most—profit, sustainability, and growth. The more you understand your numbers, the easier it becomes to lead with clarity. Business success comes from knowing how to manage your resources. When you work with a clear system and steady mindset, progress follows.