Starting a business is exciting, but addressing legal requirements early is essential to avoid future challenges. A clear legal checklist for startups can guide you through the key steps needed to establish a strong foundation. From selecting a business structure to protecting intellectual property, each decision impacts your operations.

Starting a business is exciting, but addressing legal requirements early is essential to avoid future challenges. A clear legal checklist for startups can guide you through the key steps needed to establish a strong foundation. From selecting a business structure to protecting intellectual property, each decision impacts your operations.

Navigating legal responsibilities helps you stay compliant with regulations while building trust with employees, partners, and customers. Understanding requirements for taxes, employment laws, and contracts also reduces the risk of legal disputes. Taking the time to handle these aspects now can save you significant costs and stress later.

Creating a legal checklist for startups allows you to approach challenges with confidence. By being proactive, you can focus more energy on growing and developing your business. Starting on the right path sets your business up for long-term success.

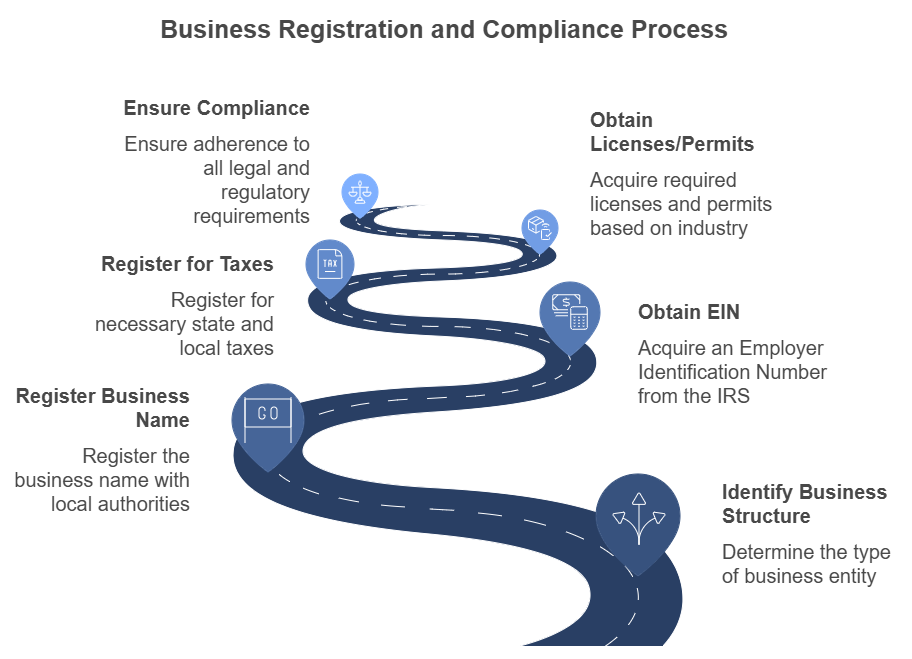

Choosing the Right Business Structure

Selecting the appropriate business structure is a fundamental step in your startup’s legal checklist. Each structure offers distinct advantages and drawbacks, impacting your legal responsibilities and tax obligations.

A sole proprietorship is the simplest form, where you and the business are legally the same. This means you have complete control but also bear unlimited personal liability for business debts. Tax-wise, profits and losses pass through to your personal tax return, simplifying filing but potentially increasing personal risk.

A partnership involves two or more individuals sharing ownership. It allows for shared decision-making and resources. However, partners are personally liable for business obligations, which can pose significant risks. Like sole proprietorships, partnerships benefit from pass-through taxation, with income and losses reported on individual tax returns.

Forming a corporation creates a separate legal entity, providing limited liability protection; your personal assets are generally shielded from business debts. Corporations can raise capital through stock issuance, facilitating growth. However, they face double taxation: the corporation pays taxes on profits, and shareholders pay taxes on dividends. Additionally, corporations require more extensive record-keeping and regulatory compliance.

A Limited Liability Company (LLC) combines elements of partnerships and corporations. It offers limited liability protection while allowing profits and losses to pass through to your personal tax return, avoiding double taxation. LLCs provide flexibility in management and fewer formalities than corporations. However, they may face self-employment taxes, and regulations can vary by state.

Understanding these structures helps you make informed decisions about your startup’s legal and financial framework.

Registering Your Business and Securing Licenses

Registering your business is a key step in establishing your startup’s legitimacy and compliance. The process varies depending on your location and chosen business structure. You need to register your business name, often referred to as a “Doing Business As” (DBA) name, with the appropriate state or local agency. This step formalizes your business and prevents others from using the same name in your area.

Next, obtain an Employer Identification Number (EIN) from the IRS if required. This number is essential for tax purposes, especially if you plan to hire employees or operate as a corporation or partnership. State and local governments may also require additional registration for sales tax, payroll tax, or income tax obligations. Following these steps carefully keeps your business compliant with federal and state regulations.

You also need the proper licenses or permits based on your industry and location. For instance, food businesses require health department permits, while professional services often need specific certifications. Research your local regulations to determine the necessary licenses for your operations. Failing to obtain permits can result in fines or business closures.

Compliance with local, state, and federal rules protects your business from legal and financial penalties. Staying organized and following the legal checklist for startups will help you operate smoothly. Additionally, being registered and licensed gives your business credibility with customers and partners, helping you build trust and professionalism.

Protecting Intellectual Property

Protecting your intellectual property is essential for safeguarding your startup’s ideas and innovations. Trademarks protect your brand name, logo, or slogan, helping you maintain a unique identity in the market. Registering a trademark with the U.S. Patent and Trademark Office (USPTO) or a similar authority provides legal rights and deters others from using your brand.

Copyrights protect original works like content, designs, or software code, giving you control over how they are used. Filing a copyright strengthens your ability to defend your ownership if disputes arise. Patents protect inventions, processes, or designs, granting exclusive rights for a set period. Filing a patent requires detailed documentation and adherence to legal processes, but it can secure your competitive edge.

Non-disclosure agreements (NDAs) are key tools for protecting ideas when collaborating with others. These agreements legally bind parties to confidentiality, reducing the risk of sensitive information being shared without permission. Using NDAs is especially important when working with contractors, investors, or potential partners.

Staying compliant with local, state, and federal regulations is also part of protecting intellectual property. Failure to follow registration requirements or renewal deadlines could weaken your legal claims. Intellectual property can also have tax implications, as some assets may qualify for deductions or impact valuations during audits or funding rounds.

Adding intellectual property protection to your legal checklist for startups helps create a solid foundation for growth. Securing your rights early avoids conflicts and keeps your business competitive and professional.

Drafting Founders’ Agreements

Drafting a founders’ agreement is essential for establishing clarity and fairness among co-founders. This agreement outlines roles, responsibilities, and ownership stakes in the business. Without it, disagreements can arise, leading to disputes that harm your startup’s progress and reputation.

A well-constructed founders’ agreement addresses equity splits, ensuring all parties understand their share of the company. It also defines decision-making authority, making it easier to avoid conflicts over control. These agreements help you allocate responsibilities, ensuring each co-founder understands their duties and contributions to the business.

Including dispute resolution mechanisms in the agreement prepares you for potential disagreements. These mechanisms outline steps to address conflicts, such as mediation or arbitration, before taking legal action. This proactive approach saves time and money while preserving relationships.

Adding a founders’ agreement to your legal checklist for startups strengthens your business foundation. It ensures transparency and reduces uncertainty among co-founders. Establishing these terms early helps you build trust and stay focused on growing your startup.

Understanding Employment Laws

Understanding employment laws is a key part of building a compliant and effective startup team. Hiring employees or contractors involves legal obligations that protect your business and your workforce. Creating clear offer letters and employment contracts helps outline expectations, compensation, and terms of employment. These documents provide clarity and reduce misunderstandings.

Proper worker classification is another essential legal consideration. Misclassifying employees as contractors can lead to penalties, fines, and legal disputes. Employees are subject to payroll taxes, while contractors are responsible for their tax obligations. Accurate classification ensures compliance with tax laws and prevents regulatory scrutiny.

Workplace compliance also plays a significant role in hiring. You must adhere to labor laws, including wage requirements, anti-discrimination policies, and workplace safety standards. Keeping detailed employee records and maintaining a compliant work environment protects your business from potential lawsuits or fines.

Including employment laws in your legal checklist for startups safeguards your business and supports long-term growth. Following these laws builds trust with your team and sets the stage for a productive and lawful work environment.

Compliance with Tax and Financial Regulations

Compliance with tax and financial regulations is a fundamental part of running a startup. Proper bookkeeping and timely tax filings keep your business on solid legal ground. Maintaining accurate financial records helps you track income, expenses, and profits while meeting reporting requirements. Filing taxes on time also avoids penalties and keeps you in good standing with regulatory agencies.

Payroll obligations are another critical area to manage. Paying employees and contractors accurately and on time builds trust and prevents legal issues. You also need to withhold and remit payroll taxes to the appropriate authorities. Failure to comply with payroll laws can result in fines or audits, which could disrupt your operations.

Mismanagement of funds or missing deadlines can lead to serious legal risks for your startup. To avoid these risks, set up reliable systems for tracking expenses, paying bills, and handling taxes. Using accounting software or hiring a professional can help you stay organized and meet your obligations.

Adding tax and financial compliance to your legal checklist for startups protects your business and supports long-term growth. Staying on top of these responsibilities avoids unnecessary risks and keeps your focus on scaling your operations.

Conclusion

Creating a comprehensive legal checklist for startups is a practical step in building a stable and compliant business. Addressing legal considerations early can prevent costly mistakes and protect your operations. From choosing a business structure to managing taxes, every decision impacts your success.

Paying attention to key areas like employment laws, intellectual property, and financial compliance reduces legal risks. Clear agreements and proper registrations establish trust and professionalism with employees, partners, and customers. Taking these steps helps you stay focused on growing your business without unnecessary distractions.

Following your legal checklist for startups also supports long-term planning. By staying organized and proactive, you create a strong foundation for scaling your operations. Keeping up with legal responsibilities allows you to focus on innovation and building value.