Finding the right small business funding options can be a key step in helping your business grow and succeed. With various choices available, from traditional loans to modern crowdfunding, each option brings unique benefits and challenges. The right funding choice depends on your business’s specific needs, goals, and growth plans.

Finding the right small business funding options can be a key step in helping your business grow and succeed. With various choices available, from traditional loans to modern crowdfunding, each option brings unique benefits and challenges. The right funding choice depends on your business’s specific needs, goals, and growth plans.

Whether you’re looking for quick access to cash or long-term financial support, understanding your options can make a difference. In this guide, you’ll learn about different funding sources and how they align with different business needs. By exploring these options, you can make informed decisions that support your business’s financial health and future growth.

Traditional Bank Loans

Traditional bank loans are one of the most common small business funding options. Banks provide loans with fixed interest rates and clear repayment terms. To qualify, your business will typically need a solid credit history, financial documentation, and sometimes collateral. Banks may also review your business plan to assess the loan’s potential for return. This thorough review process often makes bank loans an option for established businesses with a reliable financial track record.

Interest rates on traditional bank loans are generally lower than alternative financing options, which can save your business money in the long run. Additionally, these loans come with longer repayment terms, which can help manage cash flow by keeping monthly payments lower. However, because of the strict requirements and lengthy application process, it can take weeks or even months to receive approval and funding. This may not suit businesses that need fast access to capital.

On the downside, bank loans require a significant amount of documentation and a high credit score. For newer or smaller businesses, meeting these requirements can be challenging. If your business lacks collateral, securing a bank loan may also be difficult. Despite these limitations, traditional bank loans offer stability and predictable costs, making them a strong option for businesses with established credit and clear growth plans.

Online Lenders and Alternative Financing

Online lenders and alternative financing options offer flexibility and speed, making them appealing small business funding options. Unlike traditional banks, online lenders have streamlined applications and faster approval processes. Many online lenders can provide funding within days, which helps if you need quick access to capital for pressing needs.

Peer-to-peer lending is one alternative financing method where individual investors fund loans through online platforms. This approach can offer more lenient credit requirements and competitive interest rates. With peer-to-peer lending, your business may access funds without going through a traditional bank’s lengthy review process. Similarly, non-bank financing, such as merchant cash advances or invoice factoring, provides cash flow solutions by leveraging future sales or accounts receivable.

Alternative financing options typically offer flexible terms and repayment schedules. However, these options may come with higher interest rates or fees than traditional loans, so it’s essential to review terms carefully. Despite this, online lenders and alternative financing offer accessible options for businesses that may not qualify for traditional bank loans. If speed and flexibility are priorities, online and alternative lending can be practical solutions for your funding needs.

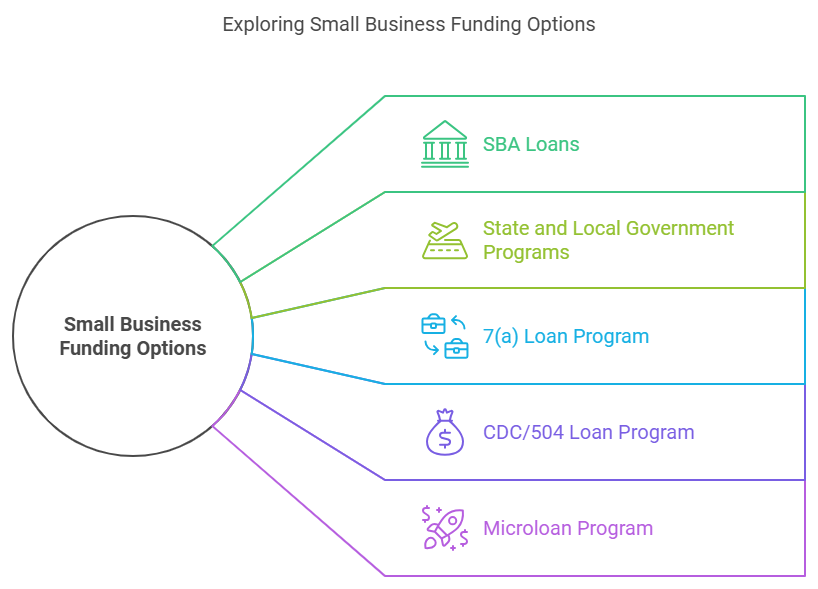

SBA Loans and Government Programs

SBA loans are a popular choice among small business funding options because they offer favorable terms and government-backed support. The Small Business Administration (SBA) partners with approved lenders to reduce risks, making loans more accessible for small businesses. With lower interest rates and longer repayment periods, SBA loans provide manageable financing that helps businesses maintain healthy cash flow.

To apply for an SBA loan, your business must meet specific requirements, including size standards, a strong credit history, and, in some cases, collateral. Common SBA loans include the 7(a) loan program, which supports general business needs, and the CDC/504 loan, which focuses on major assets like equipment or real estate. Additionally, the SBA microloan program offers smaller loans for startups and businesses with limited capital needs.

Government programs beyond SBA loans also support small businesses. Many state and local governments offer grants, subsidies, or other funding to stimulate local economic growth. These programs may not require repayment, which can be highly advantageous for your business. However, the application process for both SBA loans and other government programs can be lengthy and detailed. For businesses that meet the qualifications, these options offer valuable support, making them ideal for steady growth.

Business Credit Cards

Business credit cards are a flexible small business funding option that can help you cover short-term expenses and manage cash flow. With easy access to credit, these cards allow you to make purchases, pay bills, or handle emergency costs. Many business credit cards also offer rewards programs, allowing you to earn points, cashback, or other perks on regular purchases. These rewards can offset expenses, making credit cards a valuable tool for day-to-day business needs.

One of the main advantages of business credit cards is their convenience. Approval processes are often faster than traditional loans, and they require less documentation. Additionally, business credit cards help you track expenses by keeping business and personal finances separate, which simplifies bookkeeping. Many cards also come with features like spend tracking, making it easier to monitor and manage your spending.

However, relying on business credit cards can carry risks. Interest rates on credit cards are often higher than those on traditional loans, which means carrying a balance can become costly. Overspending or missing payments can also impact your business credit score, which may limit future funding options. Used wisely, however, business credit cards are a practical addition to your small business funding options, providing flexibility and rewards for managing everyday expenses.

Angel Investors and Venture Capital

Angel investors and venture capital are popular small business funding options for companies aiming for rapid growth. Both offer equity financing, meaning you exchange a portion of your business ownership for funding. Angel investors are typically individuals who invest their own money in startups or early-stage companies. They provide funding in exchange for equity, often bringing valuable mentorship and industry connections along with their investment.

Venture capital, on the other hand, involves investment firms pooling funds from multiple investors to support high-potential businesses. Venture capitalists usually seek companies with significant growth potential and a scalable business model. They often invest in later stages, as the business starts to show traction, though some firms focus on earlier rounds. This type of financing is suitable for businesses planning to scale quickly and willing to give up partial ownership.

Both angel investors and venture capital come with pros and cons. While you gain significant funding and guidance, you also cede some control and ownership. This trade-off is often ideal for businesses in competitive industries, where rapid growth is necessary to succeed. For companies seeking strategic partnerships and substantial funding, equity financing through angel investors or venture capital can be a valuable step forward.

Crowdfunding and Community-Based Funding

Crowdfunding and community-based funding are small business funding options that allow you to raise capital directly from your supporters. Through crowdfunding platforms like Kickstarter or Indiegogo, you can present your business idea or project to a wide audience. Supporters contribute small amounts that add up, providing you with necessary funding while also building a base of loyal customers.

These platforms allow businesses to offer rewards or pre-sales to incentivize support. This method is ideal for product-based businesses looking to validate ideas before launching. For instance, supporters may receive early versions of a product, creating both capital and initial demand. This approach reduces financial risk by securing funding from people who believe in your business.

Community-based funding works similarly but often focuses on local engagement. This method can connect you with people in your community who want to support small, local businesses. Both crowdfunding and community funding can help you test market interest while building a sense of loyalty and awareness. If traditional financing is out of reach, these options provide accessible ways to fundraise and grow your business.

Conclusion

Exploring small business funding options can open valuable opportunities for growth, stability, and innovation. From traditional bank loans to crowdfunding, each option offers unique advantages. By understanding these choices, you can align your financing approach with your business’s needs and goals. Whether you need quick access to funds or strategic guidance, there is likely a solution that fits.

Consider factors like cost, flexibility, and repayment terms when choosing the right funding method. The right financing can help you meet immediate needs while setting a strong foundation for the future. Ultimately, selecting the best funding option allows you to focus on what matters—building and growing your business successfully.