Expanding your business often requires outside funding, and many owners turn to small business loans for expansion to support their plans. These loans can help you grow without giving up ownership or control. However, not every business is ready to borrow. You should first evaluate your financial position and long-term goals.

Expanding your business often requires outside funding, and many owners turn to small business loans for expansion to support their plans. These loans can help you grow without giving up ownership or control. However, not every business is ready to borrow. You should first evaluate your financial position and long-term goals.

Additionally, it helps to understand the types of loans available. Each option has different terms, rates, and approval requirements. Therefore, knowing what lenders look for can improve your chances of approval. You’ll also need a clear plan for how the funds will be used. That plan should show a direct link between the loan and your growth goals.

Many owners rush the process, but careful planning matters. Taking time to compare lenders helps you avoid expensive mistakes. Additionally, reading the fine print on interest rates and fees protects your business from surprise costs. The more informed you are, the better decisions you’ll make.

Before you apply, check your credit and gather your financial documents. You may need to present a business plan, tax records, or cash flow statements. Therefore, being organized can make the process smoother. The right loan can move your business forward, but only if you use it wisely.

Every business grows at its own pace. By asking the right questions and reviewing all your options, you can find a loan that fits your needs. Small loans or large ones—what matters most is how you use the money. Your approach will shape the results.

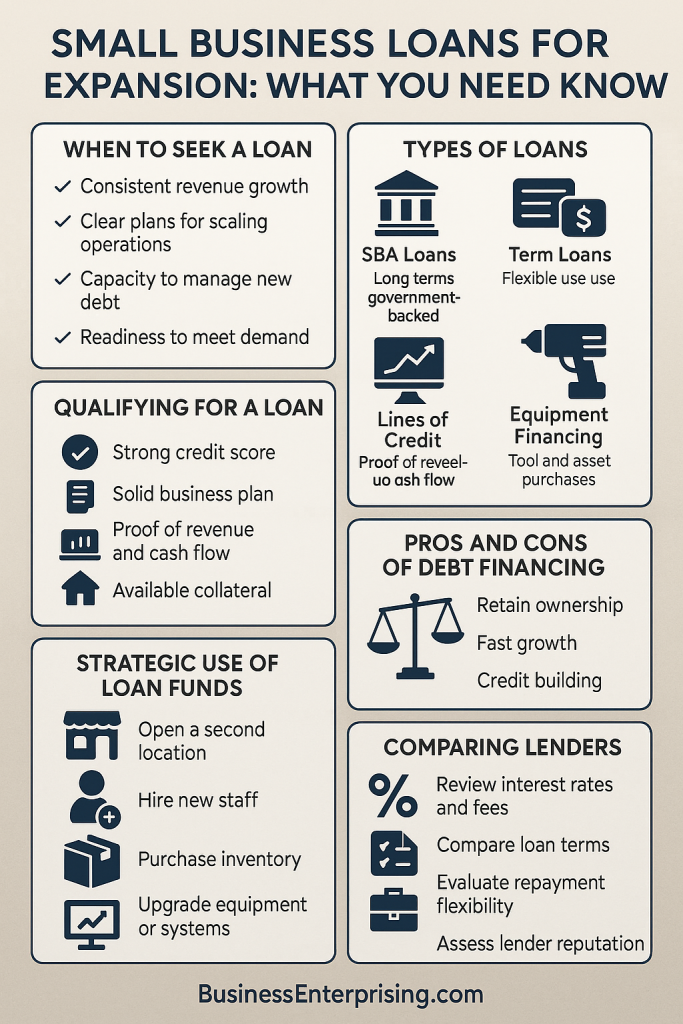

When Is the Right Time to Seek a Business Expansion Loan?

Determining when to seek a business expansion loan depends on several key factors that signal your business is ready for growth. One of the main indicators is consistent revenue growth. If your business has seen steady increases in sales and profits over a period of time, it may be the right moment to seek additional funding for expansion. However, you should also consider your capacity to handle the demands of scaling up.

Another sign that it’s time for a loan is when you have a clear plan for how to use the funds. If your business is ready to expand to new locations, hire additional staff, or purchase inventory to meet growing demand, small business loans for expansion could be a strategic option. Additionally, if you’re facing increasing customer demand that your current operations can’t support, it’s important to act quickly before potential growth opportunities are missed.

Finally, your business’s creditworthiness plays a key role. If you’ve built a solid credit history and have a track record of timely payments, lenders are more likely to approve your loan application. It’s important to assess your financial health and the potential risks involved. With the right preparation and the right timing, a loan can help your business grow to the next level.

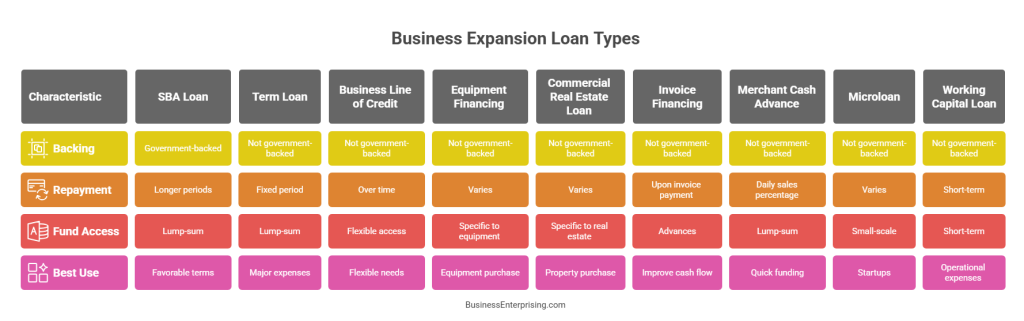

Types of Loans Available for Small Business Expansion

When planning for growth, it’s helpful to understand the different types of loans available to your business. Small business loans for expansion come in several forms, each with different uses and terms. If you’re looking for government-backed funding, SBA loans can be a solid option. These loans typically offer longer repayment terms and competitive interest rates. However, the approval process can take time, so be prepared.

Another option is a traditional term loan. These loans give you a lump sum of money that you repay over a set period. If your expansion needs include large one-time expenses, term loans may fit your plans. Additionally, business lines of credit offer more flexibility. You can access funds as needed and only pay interest on the amount you use.

Therefore, if your business needs new machinery or tools, equipment financing may be appropriate. This type of loan is tied directly to the equipment you’re purchasing. It often requires less paperwork and may come with favorable rates. However, the equipment typically acts as collateral.

Each loan type has pros and cons. You should consider how quickly you need the funds and what your repayment capacity looks like. Also, factor in how each option aligns with your overall expansion goals. Choosing the right loan can make a big difference in how smoothly your business grows.

How to Qualify for a Small Business Expansion Loan

Qualifying for a loan starts with understanding what lenders look for. They want to see a strong credit profile and solid business history. Most lenders prefer a personal credit score above 680. However, some may work with lower scores if other areas are strong. Therefore, it’s important to review your credit report before applying.

Lenders will also want to see a detailed business plan. This shows them how you’ll use the funds and repay the loan. Your plan should clearly outline your expansion strategy, projected revenue, and expected costs. Additionally, financial statements help support your case. These include balance sheets, income statements, and cash flow reports. Lenders use this data to assess your ability to repay debt.

Another factor is collateral. You may be asked to pledge assets like equipment, property, or inventory. This gives lenders more security. However, some loan programs do not require collateral if your credit and revenue are strong. Still, having assets to offer can improve your chances.

It also helps to show consistent revenue growth. If your business shows a stable and upward financial trend, lenders are more likely to approve you. Additionally, prepare to share tax returns, bank statements, and ownership documents. These support your application and reduce questions from the lender.

Applying for small business loans for expansion takes preparation. But when you meet the basic requirements, your chances increase. Focus on building a strong financial foundation before you apply. That effort pays off when it’s time to grow.

How to Use Loan Funds Strategically for Growth

Qualifying for a loan starts with understanding what lenders look for. They want to see a strong credit profile and solid business history. Most lenders prefer a personal credit score above 680. However, some may work with lower scores if other areas are strong. Therefore, it’s important to review your credit report before applying.

Lenders will also want to see a detailed business plan. This shows them how you’ll use the funds and repay the loan. Your plan should clearly outline your expansion strategy, projected revenue, and expected costs. Additionally, financial statements help support your case. These include balance sheets, income statements, and cash flow reports. Lenders use this data to assess your ability to repay debt.

Another factor is collateral. You may be asked to pledge assets like equipment, property, or inventory. This gives lenders more security. However, some loan programs do not require collateral if your credit and revenue are strong. Still, having assets to offer can improve your chances.

It also helps to show consistent revenue growth. If your business shows a stable and upward financial trend, lenders are more likely to approve you. Additionally, prepare to share tax returns, bank statements, and ownership documents. These support your application and reduce questions from the lender.

Applying for small business loans for expansion takes preparation. But when you meet the basic requirements, your chances increase. Focus on building a strong financial foundation before you apply. That effort pays off when it’s time to grow.

Pros and Cons of Using Debt to Finance Expansion

Once you receive funding, it’s important to use the money wisely. You want every dollar to move your business forward. Many owners use small business loans for expansion to open a second location. If you’ve outgrown your current space, adding a new site can boost sales and reach new customers.

However, physical growth is just one option. You may choose to hire new staff instead. More employees can improve service, reduce burnout, and free you to focus on strategy. Additionally, adding inventory is another smart way to use your loan. If demand is rising, having more stock on hand helps you meet customer needs.

Upgrading outdated equipment is also worth considering. New tools can increase productivity and lower repair costs. Therefore, it’s often better to invest now than deal with breakdowns later. You might also use the funds to invest in software or systems that help your operations run more smoothly.

Before spending, review your business plan. Think about how each purchase supports your long-term goals. Avoid using funds on expenses that won’t directly lead to growth. Additionally, track how each investment performs over time. This helps you make better choices if you seek future funding.

Using loan funds well takes planning and discipline. When done right, these investments help your business grow steadily. Small business loans for expansion are powerful tools—but only when used with purpose.

Tips for Comparing Lenders and Securing the Best Terms

Before choosing a lender, take time to compare the full cost of borrowing. Interest rates vary, so check both fixed and variable rates. A lower rate can save you a lot over time. However, watch for fees that may raise your total repayment amount. These can include origination charges, application fees, or prepayment penalties.

Additionally, look closely at the loan term. Shorter terms often mean higher monthly payments but less interest overall. Longer terms lower your payment but increase total costs. Therefore, match the term to your cash flow. You want a payment schedule that fits your budget.

Repayment options also matter. Some lenders allow early payments without penalty. Others may offer flexible schedules or seasonal payments. If your income varies, flexibility can be helpful. However, read the fine print so you know exactly what’s expected of you.

You should also check the lender’s reputation. Fast approval is helpful, but clear communication is just as important. Additionally, ask questions about support during the life of the loan. If problems arise, you’ll want a lender that’s easy to reach and fair to work with.

When shopping for small business loans for expansion, don’t rush. A little research can make a big difference. Compare multiple offers, and always read the full agreement. By doing this, you protect your business and set yourself up for smarter growth.

Conclusion

Growing your business takes careful planning, and funding can play a key role in that process. Small business loans for expansion offer a practical way to access the capital you need. However, taking on debt comes with responsibility. You must weigh the risks and understand the terms before you move forward.

Additionally, you should have a clear plan for how to use the funds. Every dollar should support a goal that moves your business ahead. Therefore, it’s important to track performance and adjust your spending if needed. Loan funds should never cover everyday shortfalls. Instead, they should push you toward growth.

Comparing lenders helps you make smarter decisions. Interest rates, fees, and repayment terms vary. Take time to review offers in full. Additionally, be ready to present strong financials when you apply. Lenders want to see that your business is stable and likely to grow.

Your decision should also match your risk tolerance. Some businesses can handle larger loans and faster growth. Others may benefit from a smaller, more manageable step forward. However, don’t borrow more than you can repay comfortably. The goal is long-term success, not short-term pressure.

Expanding a business takes effort and discipline. With the right loan and a thoughtful plan, you can grow with confidence. Keep your goals clear, your numbers honest, and your spending focused. That approach can help you make the most of your loan and build a stronger future.