Finding the right funding is one of the first big decisions you’ll face when starting a business. Many new business owners explore startup grants and loans as a way to secure the capital needed to launch and grow. These funding options can help you cover key expenses like equipment, marketing, and operations.

Finding the right funding is one of the first big decisions you’ll face when starting a business. Many new business owners explore startup grants and loans as a way to secure the capital needed to launch and grow. These funding options can help you cover key expenses like equipment, marketing, and operations.

However, not every funding source works the same way. Grants provide funds you don’t have to repay, but they’re often competitive and restricted in use. Loans offer more flexibility but require repayment, typically with interest. Therefore, understanding how each works helps you make better financial decisions for your business.

Additionally, each funding type has different application requirements. You’ll need to present a clear business plan, financial projections, and possibly personal financial details. Therefore, organizing your documents early can save time and reduce stress during the application process.

Furthermore, receiving funding is only the beginning. Once approved, you’ll need to manage those funds carefully. Creating a detailed budget and tracking spending will help you use resources wisely. Therefore, staying disciplined with your finances supports both short-term progress and long-term sustainability.

Starting a business is challenging, but having the right funding in place can make the process more manageable. With a clear understanding of your options and a solid plan in hand, you’ll be better positioned to move forward with confidence.

What Are Startup Grants and Loans?

Starting a new business often requires significant capital, and understanding the available funding options is essential. Two primary sources of financing are startup grants and loans, each with distinct characteristics.

Startup grants are funds provided by governments, corporations, or foundations to support specific business initiatives. Unlike loans, grants do not require repayment, making them highly attractive to entrepreneurs. However, they are typically competitive and come with stringent eligibility criteria and usage guidelines. Recipients may need to report on how the funds are utilized to ensure compliance with the grant’s objectives.

In contrast, startup loans are borrowed funds that businesses must repay over time, usually with interest. These loans can be obtained from banks, credit unions, or other financial institutions. Lenders assess the borrower’s creditworthiness and business plan to determine eligibility. While loans increase a company’s debt, they provide immediate capital without diluting ownership.

Choosing between grants and loans depends on your business’s specific needs and circumstances. Grants offer “free” money but are challenging to secure and often have restrictions on fund usage. Loans are more accessible but require repayment with interest, impacting cash flow. Evaluating both options will help you determine the best approach to finance your startup.

Pros and Cons of Grants vs. Loans for Startups

When launching a startup, securing adequate funding is a pivotal step. Two primary avenues are available: grants and loans. Grants are funds provided by governments, corporations, or nonprofits that do not require repayment. They are typically designated for specific projects or purposes and come with stringent eligibility criteria. Conversely, loans involve borrowing a sum of money from financial institutions or lenders, which must be repaid with interest over an agreed-upon period. Loans offer flexibility in usage but necessitate a commitment to regular repayments.

Understanding the key differences between startup grants and loans is essential for making informed financial decisions. Grants provide non-repayable funds, alleviating the burden of debt. However, they are highly competitive and often have specific usage restrictions. Loans, while requiring repayment with interest, offer quicker access to funds and can be utilized for a broader range of business needs. Assessing your startup’s immediate financial requirements, long-term goals, and ability to meet repayment obligations will guide you in choosing the most suitable funding option.

Types of Startup Grants Available to Entrepreneurs

Securing funding is a pivotal step in launching a new business, and understanding the available options is essential. Two primary avenues entrepreneurs explore are startup grants and loans. Grants are funds provided by government agencies, private companies, or nonprofit organizations that do not require repayment. They are often awarded based on specific criteria, such as industry focus, demographic targets, or innovative potential. For instance, the Small Business Innovation Research (SBIR) program offers grants to small businesses engaging in federal research and development with commercialization potential.

Conversely, loans involve borrowing capital that must be repaid over time, typically with interest. Financial institutions, including banks and credit unions, provide loans to startups they deem creditworthy. The approval process usually assesses factors like the entrepreneur’s credit history, business plan viability, and projected financial performance. While loans require repayment, they often offer more substantial funding amounts compared to grants.

Understanding the differences between startup grants and loans is crucial for making informed financing decisions. Grants provide debt-free capital but are highly competitive and may come with usage restrictions. Loans offer more immediate funding but necessitate a clear repayment strategy and accrue interest. Evaluating your business’s needs, eligibility, and long-term financial outlook will guide you in choosing the most suitable funding route.

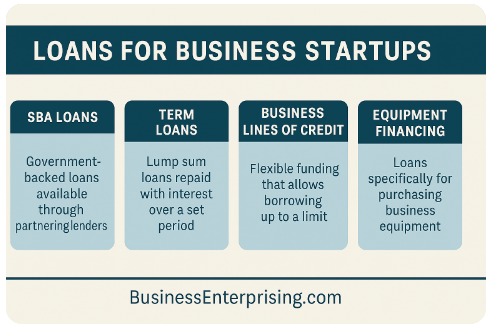

Loan Options for New Business Owners

Securing financing is a significant step for new business owners. Various loan options are available to support your startup’s financial needs. Understanding these options can help you make informed decisions about funding your business.

SBA microloans offer up to $50,000 to help small businesses start and expand. These loans are administered by nonprofit community-based organizations experienced in lending and business assistance. The average microloan is about $13,000. Funds can be used for working capital, inventory, supplies, furniture, fixtures, and equipment. However, you cannot use them to pay existing debts or purchase real estate.

Business lines of credit provide flexible funding, allowing you to draw funds as needed up to a predetermined limit. You pay interest only on the amount you use. This option is suitable for managing cash flow, purchasing inventory, or covering unexpected expenses. Some financial institutions offer secured lines of credit for startups, requiring a refundable security deposit equal to the credit limit.

Online lenders have emerged as accessible sources of funding for startups. They offer various loan products with streamlined application processes and faster approval times compared to traditional banks. For instance, some online lenders provide term loans up to $250,000 with repayment terms up to 24 months. These loans can be used for diverse business needs, including expansion, equipment purchases, and working capital.

When exploring startup grants and loans, it’s essential to assess your business’s specific needs, financial situation, and eligibility for each funding type. Consulting with financial advisors or utilizing resources from the U.S. Small Business Administration can provide further guidance tailored to your circumstances.

How to Qualify and Apply for Startup Funding

Securing funding for your startup involves understanding the qualifications and application processes for various financing options. Both startup grants and loans require thorough preparation and attention to detail.

Assess Your Financial Needs and Eligibility

Begin by evaluating how much capital you need and the purpose it will serve. This clarity helps in selecting the appropriate funding type and informs potential funders of your business’s requirements. Lenders and grant providers often assess both personal and business credit scores to gauge creditworthiness. A higher credit score can improve your chances of approval and may lead to more favorable terms. Conversely, a lower score might necessitate exploring alternative financing options.

Prepare Essential Documentation

Gathering the necessary documents is a critical step. Lenders typically require personal and business tax returns from the past two to three years, financial statements, legal documents, and business licenses. Having these documents organized and up-to-date can streamline the application process and demonstrate your business’s readiness.

Research Funding Sources

Identifying the right funding sources is vital. Traditional banks, online lenders, government programs, and nonprofit organizations offer various startup grants and loans. Each has specific eligibility criteria and application procedures. Understanding these nuances enables you to tailor your application to meet their expectations.

Craft a Compelling Application

A well-prepared application should clearly articulate your business plan, financial projections, and how the funds will be utilized. Emphasize your business’s potential for growth and repayment capacity. Address any potential concerns proactively to strengthen your case.

Engage with Funders

Building relationships with potential funders can provide insights into their priorities and increase your application’s visibility. Attend networking events, seek introductions, and maintain open communication throughout the application process.

By diligently preparing and strategically approaching the application process, you can enhance your prospects of securing startup grants and loans that align with your business objectives.

Tips for Managing Funds After Approval

Securing funding marks a significant milestone for your startup. However, managing these funds effectively is essential to foster growth and sustainability. To achieve this, develop a comprehensive budget that outlines your projected income and expenses. This financial plan serves as a roadmap, helping you allocate resources efficiently and identify potential financial challenges early on. Regularly reviewing and adjusting your budget ensures alignment with your business objectives and market conditions.

Implementing a robust expense management system is equally important. Utilize tools or software to meticulously track every dollar spent, providing real-time insights into your cash flow. This practice not only aids in monitoring expenditures but also enforces spending policies and prepares you for audits. Establishing clear expense policies and approval processes promotes accountability and transparency within your team.

Additionally, setting aside a contingency fund is prudent. Allocating a portion of your budget, typically 5-10%, for unforeseen expenses creates a financial cushion. This reserve enables you to handle unexpected challenges without jeopardizing your operations. Strategically managing your startup grants and loans through diligent budgeting, expense tracking, and contingency planning positions your business for long-term success.

Conclusion

Securing funding is a significant step toward launching and growing your business. However, what you do after receiving funds matters just as much. Whether you choose startup grants and loans, the way you manage them will impact your progress. Therefore, it’s important to treat all funding as a tool, not a solution on its own.

Additionally, having a plan helps you avoid missteps. You can allocate resources wisely and stay focused on your goals. However, flexibility is equally important. Business needs can shift, and your spending plan should adjust with them. Therefore, track your use of funds and revisit your budget regularly.

Furthermore, maintaining clear records shows professionalism and builds trust with lenders or grant providers. This habit also prepares you for future funding needs. Therefore, document all expenses and store files in one secure location. This organization will help you stay compliant and ready for audits or renewals.

Using your funds well also builds confidence in your leadership. Funders often review how previous funding was handled. Therefore, spending wisely now can support future funding success. Strong financial habits set the stage for sustainable growth and long-term stability.

Starting and running a business involves ongoing decisions. Startup funding is only the beginning. Therefore, invest time into managing resources carefully and making strategic choices. When you do, you give your business a better chance at lasting success.