Running a business always involves risk. Markets shift, costs rise, and customer habits change. Surviving economic downturns depends on how you respond. Therefore, planning ahead gives you a better chance to stay steady when things slow down. You can’t control outside conditions, but you can control your decisions.

Running a business always involves risk. Markets shift, costs rise, and customer habits change. Surviving economic downturns depends on how you respond. Therefore, planning ahead gives you a better chance to stay steady when things slow down. You can’t control outside conditions, but you can control your decisions.

Many businesses struggle because they wait too long to act. However, small problems become harder to fix when ignored. Additionally, missing early signs can lead to deeper losses. You need to stay alert, think clearly, and move with purpose. These habits help you stay strong during uncertain times.

Operational strength starts with daily habits. Therefore, you should watch your numbers, review your processes, and talk openly with your team. Additionally, listen to your customers. They often feel change before it shows up in your reports. This feedback helps you adjust without guessing.

Clear thinking and steady action often matter more than big ideas. You don’t need perfect timing or flawless plans. However, you do need to stay committed to practical steps that support your goals. Additionally, the ability to adapt gives you an edge over competitors who stay rigid.

Economic pressure forces hard choices. Still, you have more control than you think. Therefore, build smart habits now that support long-term success. When conditions shift, you’ll be ready to protect your business and continue serving your market.

Understanding the Impact of Difficult Economic Times

Economic hardship affects more than your bottom line. It shifts how you spend, what you prioritize, and where you take risks. You might feel pressure to cut costs or delay important projects. However, these choices often create new challenges later. Business owners tend to freeze spending, which can reduce visibility and shrink future revenue.

Your customers are feeling it too. As prices rise and budgets tighten, people change buying habits. Therefore, products or services that were once steady sellers may slow down. Additionally, payment delays and credit concerns can interrupt cash flow. You need to watch these patterns closely and stay flexible.

Many companies respond by focusing on their core offers. This makes sense when you need to protect margins and control expenses. However, holding onto outdated methods can limit your growth. You must stay open to practical shifts that support your goals. Additionally, reevaluating suppliers, contracts, and staff costs helps protect your financial base.

Surviving economic downturns depends on clear thinking and practical planning. You don’t need a complete overhaul, but you do need to act with purpose. Consistent communication, small operational improvements, and measured investment can keep you moving forward. Therefore, avoid waiting too long before making hard decisions.

Additionally, remind yourself that hard times are temporary. While you cannot control the economy, you can control how your business responds. Rely on data, protect your team, and stay focused on your goals. This approach helps you avoid panic and make smart, steady progress even during uncertain times.

Decreased Consumer Spending:

During a recession, consumers tend to tighten their belts, leading to decreased spending on non-essential goods and services. This reduction in demand can impact sales and revenue for businesses across various sectors.

Cash Flow Constraints:

With declining sales and potential delays in receivables, maintaining healthy cash flow becomes challenging. Cash flow constraints can hinder a company’s ability to meet its financial obligations, such as payroll, rent, and supplier payments.

Operational Disruptions:

Recessions can lead to disruptions in supply chains, workforce availability, and overall business operations. Companies may face challenges in sourcing materials, managing inventory, and maintaining production levels.

Increased Competition:

As businesses scramble to maintain market share during tough times, competition can intensify. Companies need to find ways to differentiate themselves and retain customer loyalty.

Financial Uncertainty:

Uncertainty about future economic conditions can lead to cautious spending and investment decisions. Businesses may delay or cancel planned expansions, investments, or new product launches.

Strategies for Surviving Economic Downturns

Economic downturns hit hard and fast. You may not get much warning, but you still have options. Acting quickly matters. Cutting unnecessary spending is often the first step. However, be careful not to cut too deep. You need to keep key operations moving to stay in business.

Therefore, review your current expenses and find savings that don’t harm your core business. Focus on what directly supports sales, cash flow, or customer trust. Additionally, look at renegotiating terms with vendors or adjusting payment schedules. These small changes can protect your liquidity without creating long-term damage.

You also need to stay in close contact with your customers. Their needs may shift as budgets shrink. However, people still spend on products that solve problems or offer real value. Keep your messaging clear and honest. Additionally, update your offers if needed. This shows you’re paying attention and willing to adapt.

Surviving economic downturns requires more than short-term fixes. You need a plan that covers both immediate needs and future growth. Therefore, protect your cash, stay flexible, and take time to think before making big moves. Additionally, focus on internal efficiency. Better systems now can pay off when the market turns.

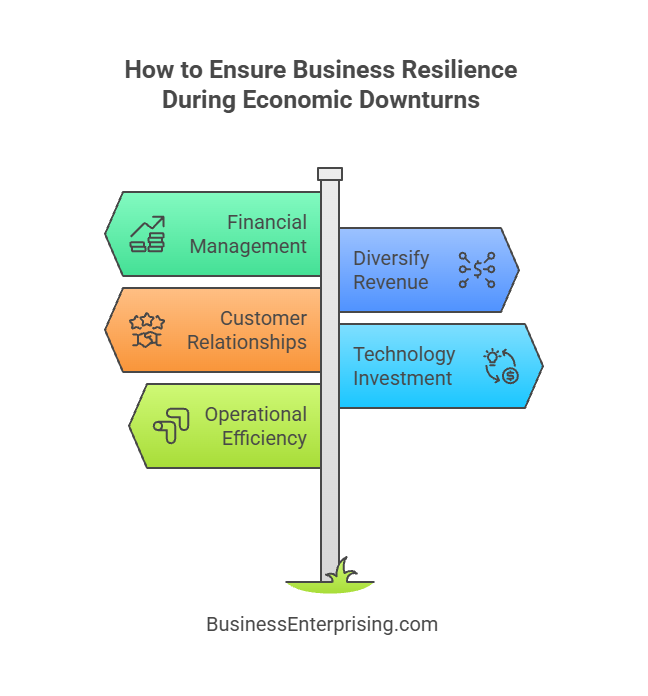

You won’t control the economy, but you can control your response. Keep your team focused, your spending smart, and your goals realistic. These steps don’t guarantee fast recovery, but they make sure you’re still here when conditions improve. To navigate economic downturns successfully, businesses should adopt a multifaceted approach that includes financial management, operational efficiency, and strategic innovation.

Strengthen Financial Management

Good financial management starts with clarity. You need to know where your money goes and how much is coming in each month. Many business owners skip this step, but that choice creates risk. Without clear numbers, you make guesses instead of decisions.

Therefore, begin by reviewing your current financial reports. Focus on cash flow, expenses, and debt. Additionally, set up a basic system for tracking revenue sources. You don’t need advanced software to improve visibility. Simple reports and regular updates can go a long way. However, make sure you check them often and act on what you see.

Managing expenses matters more than usual during slow periods. Therefore, cut or pause anything that doesn’t support your short-term goals. Additionally, look at vendor contracts, staffing levels, and recurring charges. Each area offers chances to reduce waste without affecting quality. You want to stay lean without putting operations at risk.

Strong financial habits also help with long-term planning. When you track trends over time, you see what’s working and what’s not. This gives you time to adjust before bigger problems arise. Additionally, it prepares you for surviving economic downturns by making your business less reactive and more resilient.

You don’t need a finance degree to do this well. What matters is consistency, accuracy, and follow-through. Therefore, schedule time each week to review your numbers. Use those insights to make smart, forward-looking choices. Over time, this builds a stable foundation that can support future growth without unnecessary stress.

Enhance Cash Flow Management:

Monitor cash flow closely and implement measures to improve liquidity. Negotiate extended payment terms with suppliers, offer early payment discounts to customers, and manage inventory levels efficiently to free up cash.

Build a Financial Cushion:

Establish a reserve fund to provide a financial buffer during tough times. Setting aside a portion of profits during prosperous periods can help businesses weather economic downturns.

Reduce Unnecessary Expenses:

Conduct a thorough review of operational expenses and identify areas where cost savings can be achieved. Focus on eliminating non-essential expenditures and optimizing resource allocation.

Diversify Revenue Streams

Relying on one income source puts your business at risk. When demand drops, your entire operation feels the pressure. Therefore, diversifying revenue streams helps reduce that risk. You gain more stability and create new growth options at the same time.

Start by reviewing your current products or services. Look for small adjustments that add value without raising costs. Additionally, think about new markets you can reach with minimal effort. These might include different customer types or new platforms. However, test ideas before investing heavily. You want to learn fast and adjust early.

Some companies create digital products or offer online services. Others add consulting, maintenance, or training to existing sales. These add-ons can bring in steady income with lower overhead. Additionally, subscriptions and memberships work well if you provide consistent value. Keep the structure simple and easy to manage over time.

Surviving economic downturns often depends on having more than one way to earn. Therefore, spreading out your revenue reduces pressure when one stream slows down. It also gives you flexibility when market needs shift. Additionally, different streams can support each other and build overall stability.

You don’t need to create something new from scratch. Start with what you know, then look for natural extensions. Keep costs low and track your results closely. This approach keeps your business balanced and less dependent on any one income source.

Expand Product or Service Offerings:

Explore opportunities to diversify your product or service portfolio. Introducing new offerings can help tap into different market segments and reduce dependency on a single revenue stream.

Enter New Markets:

Consider expanding into new geographic regions or customer demographics. Diversification can help mitigate the impact of an economic downturn in one market by leveraging opportunities in others.

Enhance Customer Relationships

Customer relationships often determine how well your business holds up under pressure. Therefore, keeping clients engaged should remain a daily focus. You gain more than sales when people trust your business. You build loyalty that lasts through slow periods and market shifts.

Start by listening more than you speak. Your customers will often tell you what they need, if you make time to ask. Additionally, respond quickly and clearly to questions or concerns. Small efforts here can make a big difference. However, avoid overpromising. Be clear about what you can deliver and when.

Consistency builds trust. Therefore, follow through on your commitments, even when things get tight. People remember how they were treated when times were hard. Additionally, offer value in ways that matter to them. You don’t need discounts. Instead, offer helpful service, timely updates, or honest advice.

Maintaining strong relationships also helps with planning. Happy customers provide feedback, referrals, and repeat business. Additionally, they help you see changes before they affect your bottom line. Therefore, make room in your schedule to check in with long-time clients.

Strong customer ties are key to surviving economic downturns. When people feel connected to your business, they’re more likely to stay loyal. Additionally, they’re more willing to forgive small mistakes or delays. Focus on clear communication, useful service, and steady follow-up. These habits will help your business hold its ground through difficult times.

Focus on Customer Retention:

Retaining existing customers is often more cost-effective than acquiring new ones. Implement loyalty programs, provide exceptional customer service, and engage with customers regularly to build strong relationships.

Understand Customer Needs:

Conduct market research to understand how economic conditions are affecting your customers. Tailor your offerings and marketing strategies to address their evolving needs and preferences.

Invest in Technology and Innovation

Investing in technology often feels like a luxury during lean times. However, smart tools can help you work faster and save money. Even small improvements can make a difference when margins are tight. Therefore, choose solutions that directly support your day-to-day operations.

Start by reviewing where time or money is lost. Additionally, ask your team where systems break down or repeat work happens. These are good places to apply automation or better tools. However, you don’t need large platforms or complex systems. Many simple options can improve accuracy and reduce errors.

Technology also helps you respond to change. When conditions shift, you need fast access to data. Therefore, tools that track performance or customer trends are worth the cost. Additionally, cloud-based services make it easier to work from anywhere and share updates in real time.

You should also consider innovation as part of your regular planning. This doesn’t mean chasing trends or guessing what’s next. Instead, look at how your current process can be improved. Small updates to products, services, or delivery methods can add real value. Additionally, they show your customers that you’re thinking ahead.

Surviving economic downturns often requires more than cutting costs. It demands better ways to deliver value without increasing effort. Therefore, use technology and innovation to protect what works and improve what doesn’t. Keep your choices practical, measured, and focused on results that support long-term success.

Adopt Technology Solutions:

Embrace digital transformation to enhance efficiency and reduce costs. Implement automation, data analytics, and cloud-based solutions to streamline operations and improve decision-making.

Foster Innovation:

Encourage a culture of innovation within your organization. Develop new products, services, or business models that can provide a competitive edge and drive growth during challenging times.

Optimize Operational Efficiency

Operational efficiency means doing more with less. You reduce waste, save time, and improve results without extra effort. Therefore, small changes can create strong results. You don’t need a full overhaul to see better performance.

Start by reviewing daily processes. Identify steps that take too long or involve repeated work. Additionally, ask your team where things slow down or go off track. These gaps are where improvements can begin. However, avoid changing everything at once. Focus on one or two areas and make steady updates.

You can often improve output by using better tools or adjusting workflows. Therefore, look at how tasks are assigned and completed. Additionally, limit unnecessary steps or approvals. When work flows faster, your team becomes more productive and focused. These changes also reduce stress and improve accountability.

Efficiency also helps when times get tight. By cutting waste early, you avoid deeper cuts later. Additionally, strong operations protect your bottom line. This is one reason why optimizing systems supports surviving economic downturns. You keep control of your costs and improve your ability to adapt.

Measure progress with simple metrics. Look for gains in time, cost, or output. Then use that data to guide future changes. You don’t need to chase perfection. Instead, build a habit of looking for small wins. Over time, these steps lead to more stable and profitable operations.

Improve Supply Chain Management:

Strengthen relationships with suppliers and explore alternative sourcing options to mitigate supply chain disruptions. Implement inventory management practices to balance supply and demand effectively.

Enhance Workforce Flexibility:

Develop a flexible workforce strategy that can adapt to changing business needs. Consider cross-training employees, implementing remote work policies, and utilizing temporary or freelance talent as needed.

Maintain Clear Communication

Clear communication keeps your team focused and your clients informed. During periods of stress, silence causes confusion and weakens trust. Therefore, make regular updates part of your routine. Speak plainly, stay consistent, and don’t leave room for guesswork.

Start by sharing key goals and timelines. Your staff needs to understand what matters most and why. Additionally, create a space for questions and feedback. People want to feel heard, especially when things are changing. However, avoid long meetings or vague language. Clear, short updates work better and waste less time.

When your message is consistent, people stay aligned. This lowers mistakes and improves results. Additionally, regular check-ins give you early warnings before problems grow. Therefore, encourage two-way communication with your team, vendors, and clients. Simple updates build stronger working relationships and help everyone adjust faster.

You also need a plan for external messaging. If your business changes hours, pricing, or services, say so early. Additionally, post updates in places your customers already use. Keep the message short and easy to understand. Over time, this builds trust and shows that you care about their experience.

Maintaining good communication plays a key role in surviving economic downturns. When people know what to expect, they stay calm and cooperative. Therefore, stay visible, speak clearly, and follow through on what you say. This approach helps you lead through uncertainty and stay in control of the narrative.

Communicate Transparently with Stakeholders:

Maintain open lines of communication with employees, customers, suppliers, and investors. Transparency fosters trust and ensures that stakeholders are informed about the company’s plans and challenges.

Provide Leadership and Support:

Demonstrate strong leadership by guiding your team through uncertainty. Offer support, provide clear direction, and keep morale high to maintain productivity and engagement.

Monitor and Adapt to Market Trends

Markets never stay still for long. What worked last year may not work tomorrow. Therefore, you need to track changes early. Paying attention to shifts helps you make better decisions before issues grow. Additionally, it gives you time to adjust without rushing.

Start by watching customer behavior. Are people buying less, asking different questions, or choosing new options? These signals matter. However, don’t rely only on sales data. Feedback from staff, vendors, and competitors also helps. Therefore, collect input from multiple sources and check it regularly. This gives you a clearer view of what’s changing.

Trends often start small, then build over time. You don’t need to react to everything. However, when patterns repeat, take them seriously. Additionally, look for connections between outside events and your business results. Economic news, industry changes, and social habits can all shape demand.

Responding to trends doesn’t mean chasing fads. You should make simple changes that align with what your market expects. Adjust your offers, improve your service, or explore new channels. Additionally, test small changes before making big moves. This gives you time to see what works without wasting resources.

Monitoring trends plays a role in surviving economic downturns. It helps you stay ready rather than surprised. Therefore, stay alert, adapt quickly, and base your actions on facts. This approach keeps your business steady, even when conditions shift fast.

Stay Informed:

Keep abreast of economic indicators, industry trends, and competitor activities. Regularly review market conditions and adjust your strategies accordingly.

Be Agile and Flexible:

Develop the ability to pivot quickly in response to changing circumstances. Agility allows businesses to seize opportunities and address challenges proactively.

Case Studies: Companies Surviving Economic Downturns

Apple Inc.: During the 2008 financial crisis, Apple continued to innovate by launching the iPhone 3G and the App Store. The company’s focus on innovation and expanding its product ecosystem helped it thrive and grow market share despite the economic downturn.

Netflix: Netflix navigated the 2008 recession by transitioning from a DVD rental model to a streaming service. By leveraging technology and adapting its business model, Netflix not only survived but also positioned itself as a leader in the entertainment industry.

Procter & Gamble: Procter & Gamble (P&G) focused on maintaining strong customer relationships and investing in marketing during the 2008 recession. The company continued to innovate and introduce new products, which helped it retain market share and emerge stronger.

Conclusion

Economic challenges test more than your numbers. They test your ability to stay focused, take action, and keep moving forward. Therefore, your mindset and daily habits matter. You don’t need to predict everything, but you do need to prepare.

Additionally, steady attention to key areas can make your business stronger. Whether you reduce waste, expand your income, or improve communication, each step adds value. However, you must keep reviewing and adjusting. What works now might not work next quarter. Therefore, stay flexible and willing to rethink your approach when needed.

Surviving economic downturns is not about luck. It’s about doing the right things, over time, even when things get tight. Additionally, it means acting early instead of waiting too long. You can’t always avoid hardship, but you can avoid being caught off guard.

Focus on what you can control. That includes your spending, your team, and the way you serve your customers. Therefore, stay committed to small, smart changes that improve results. Even when growth feels slow, consistency helps build long-term strength.

You don’t have to do everything at once. Start with one step, test it, then build from there. Additionally, keep your priorities clear and your decisions practical. With the right habits, you can stay stable during tough times and be ready when conditions improve.