Starting your own business is a big decision. However, understanding the business startup process helps you make smarter choices from the beginning. Many people get stuck before they even start. Therefore, breaking things into clear steps can make the process easier to manage.

Starting your own business is a big decision. However, understanding the business startup process helps you make smarter choices from the beginning. Many people get stuck before they even start. Therefore, breaking things into clear steps can make the process easier to manage.

You probably have more questions than answers at first. That’s normal. Additionally, it’s important to take time to plan before making commitments. Jumping in too fast can lead to costly mistakes. However, doing the groundwork now saves you time and money later.

Also, each new business requires different steps. Some businesses need little more than a name and a service. Others involve permits, equipment, or outside funding. Therefore, it’s smart to assess your needs early and write things down. A simple plan gives you direction and helps you stay focused.

Additionally, early research can reveal better options than you expected. For example, you may find cheaper tools or learn about funding you didn’t know existed. Also, talking to other business owners can provide valuable advice. People who have done it before often share insights you won’t find elsewhere.

The more informed you are, the more confident you’ll feel. That confidence helps you move from planning into action. Therefore, take time to learn before rushing ahead. With a thoughtful approach, you can avoid common mistakes and build something stable from day one.

Starting doesn’t mean doing everything at once. It means taking the next right step based on what you’ve learned. And then moving forward, one choice at a time.

What is the first step in starting a business?

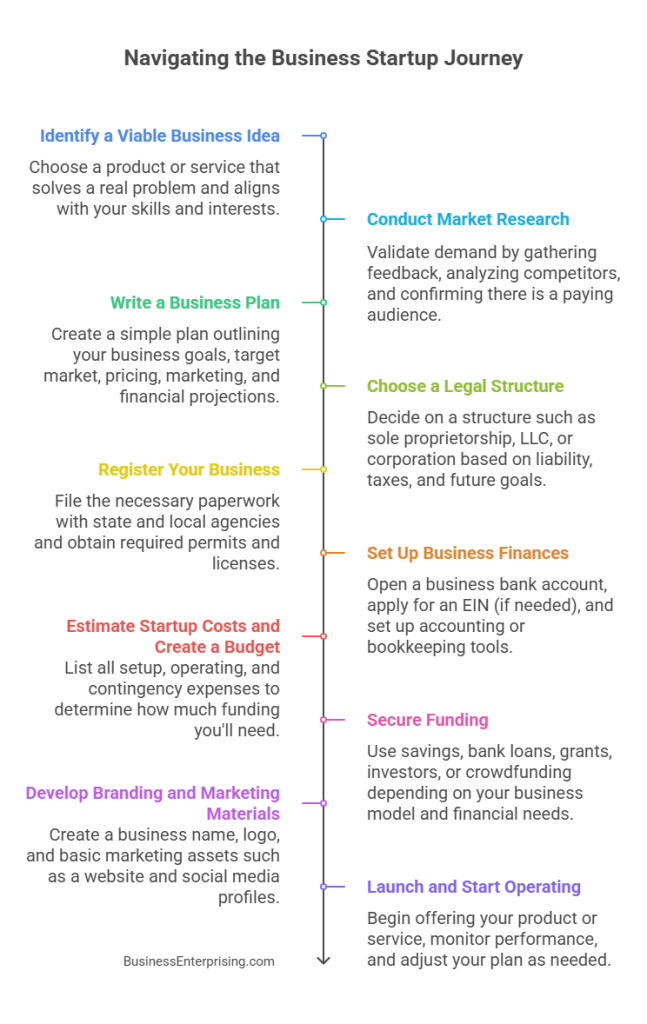

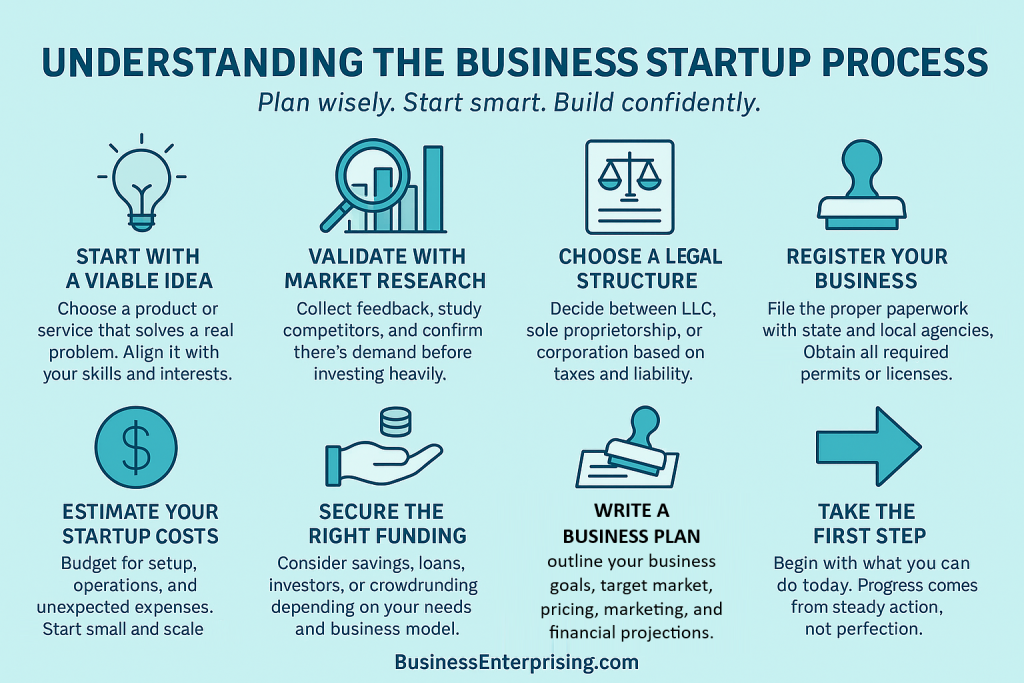

The first step is identifying a viable business idea and validating it through market research.

Starting a business begins with one simple but essential action—choosing the right idea. You need to focus on a product or service that solves a clear problem. Ideally, it should also align with your interests and skills. However, personal passion alone isn’t enough. You must validate your idea before moving forward.

This is where market research comes in. Research helps you understand who your potential customers are and what they actually need. Therefore, gather data from real people through surveys, interviews, or test campaigns. Also, study your competition to see how they position themselves and what gaps you could fill. Doing this early helps you avoid costly mistakes down the line.

Additionally, it’s helpful to estimate the size of your market. A small local demand may not support long-term growth. But a larger, unmet need offers more opportunity. However, don’t confuse interest with demand. People may like an idea but still not pay for it. So test your offer with a real price and real audience if you can.

Understanding the business startup process requires more than enthusiasm. You need real proof that people will pay for what you plan to offer. That’s why validation is more important than a logo or website at this stage. Also, use this time to refine your idea based on feedback. Each round of input helps shape a better version of your business.

By keeping your approach focused and grounded in research, you set a strong foundation. Additionally, you lower your risk and gain confidence before investing time and money. Starting with the right idea—and proving it works—is the smartest move you can make.

Do I need a business plan?

Yes, a business plan is essential for guiding strategy and attracting investors or securing loans.

Writing a business plan might feel like extra work, but it serves a real purpose. It helps you organize your ideas and see your business clearly. More importantly, it gives you a strategy for moving forward with purpose. Without it, you risk making expensive mistakes or losing direction.

A solid plan outlines what you will sell, who you will sell to, and how you will operate. Additionally, it forces you to think through costs, pricing, and expected revenue. These numbers may change over time, but starting with a rough forecast gives you a baseline. Therefore, it’s easier to adjust as your business grows.

If you plan to raise money, a business plan is often required. Investors and lenders want to know you’ve thought things through. However, even if you’re funding the business yourself, a plan keeps you grounded. It’s easy to get distracted or second-guess yourself without a clear roadmap.

Understanding the business startup process means knowing how each step connects. Your business plan ties everything together. Additionally, it helps you measure progress and spot issues early. If something doesn’t work, you can go back to the plan and revise it.

Keep your plan simple but complete. Include only what you need to explain your business and support your goals. Also, review and update it regularly. A business plan isn’t something you write once and forget. It’s a tool to guide your decisions.

Starting without a plan is like taking a trip without directions. You might get somewhere, but not where you intended. Therefore, take the time to write it down. You’ll think more clearly and act with more confidence.

What type of legal structure should I choose?

The best legal structure depends on liability, tax implications, and your long-term goals—common options include LLC, sole proprietorship, and corporation.

Choosing the right legal structure is one of the first serious decisions you’ll need to make. It affects your taxes, paperwork, and personal risk. While there’s no one-size-fits-all answer, you can make a smart choice by weighing the basics. Each option comes with its own pros and cons.

A sole proprietorship is the simplest choice. However, it leaves you personally responsible for any debts or legal issues. An LLC offers more protection while keeping your setup flexible. Additionally, it allows profits to pass through to your personal tax return. Therefore, it’s a popular pick for small business owners.

If you plan to raise money or add shareholders, you might consider a corporation. It offers strong liability protection and is seen as more formal. However, it also requires more paperwork and separate tax filings. Therefore, it’s usually better for companies aiming to grow fast or operate in high-risk industries.

Understanding the business startup process means thinking through the long-term impact of your structure. You may start small but plan to expand. Additionally, different structures come with different rules for ownership, taxes, and decision-making. Choosing wrong now could make things harder later.

Also, think about how you want to be taxed. Some structures give you options. Others don’t. However, this decision isn’t permanent. You can change later, but it takes effort and time. So it’s best to start with a structure that fits your goals.

By comparing your liability risk, tax preferences, and growth plans, you’ll narrow your options quickly. Then you can choose the one that fits your situation best.

How much money do I need to start?

Startup costs vary widely, so you should create a detailed budget that includes setup, operating, and contingency expenses.

Figuring out how much money you need to start a business depends on the type of business you plan to run. Some ideas require little more than a laptop and a service to offer. Others may need equipment, inventory, or a physical location. However, every business should begin with a detailed budget.

Start by listing your setup costs. These might include licenses, branding, and legal fees. Additionally, you’ll need to think about early operating costs. Rent, utilities, supplies, and payroll can add up quickly. Therefore, make sure you include at least three to six months of expenses.

It’s also smart to set aside extra for unexpected issues. Something will likely cost more than you planned. However, that doesn’t mean you need a huge amount of cash on day one. You can often start small and scale as you go. Additionally, you may be able to delay some purchases until your business begins generating revenue.

Understanding the business startup process means thinking ahead and being realistic with money. Many new business owners underestimate what they’ll need. Therefore, review your budget carefully before spending or committing to anything. Also, talk to someone who has experience in your industry.

You don’t need to have everything figured out immediately. But having a clear idea of your startup costs gives you direction. Additionally, it makes it easier to secure funding if needed. When you know your numbers, you can make smarter decisions. That alone puts you ahead of many first-time founders.

Where can I get funding for my business?

Common funding sources include personal savings, bank loans, angel investors, venture capital, and crowdfunding.

Finding money to start your business can feel like a challenge. However, you have several options depending on your needs and goals. Many people begin with personal savings to avoid taking on debt. Others look for help from friends or family.

Additionally, bank loans remain a common way to fund a startup. These usually require a strong credit score and a solid plan. However, you may prefer outside investors who offer capital in exchange for equity. Angel investors and venture capital firms both fit this model, though their expectations can vary widely.

If you want to test your idea publicly, crowdfunding might be a good option. Platforms let you raise funds from many small backers. Therefore, this method can also help validate your product before launch. Also, some grants exist for certain industries, but competition is usually high.

Understanding the business startup process means knowing how each funding source fits your plan. You’ll need to think about the tradeoffs. For example, debt means fixed payments, while equity means giving up partial ownership. Additionally, you should consider how much control you want to keep.

Therefore, be honest about your needs and risk tolerance. Create a plan that fits your situation and avoids overcommitting early. Also, prepare a short pitch that explains your idea clearly. This helps when applying for loans or talking to investors.

Choosing the right funding source isn’t just about the money. It’s also about how it shapes your business going forward. Take your time and ask questions before deciding.

Do I need to register my business?

Yes, you must register your business with state and local authorities to operate legally and obtain necessary licenses or permits.

Registering your business is not just a formality. It’s a legal step that makes your business official in the eyes of the state. Without it, you may face fines or miss out on contracts and funding opportunities. Therefore, it’s worth doing early in the process.

The registration process depends on your location and business structure. However, most businesses need to register with both state and local agencies. Additionally, you may need specific licenses or permits to operate legally. These vary based on your industry, so check carefully before launching anything publicly.

Understanding the business startup process includes knowing what paperwork is required. Also, your registration determines your tax obligations and legal protections. For example, registering as an LLC offers more legal separation than operating as a sole proprietorship. Therefore, it’s a key step for protecting your personal assets.

Additionally, you’ll likely need a federal tax ID number. This is used for hiring employees or opening a business bank account. However, some sole proprietors can use their Social Security number if allowed. Each situation is different, so you’ll want to confirm what applies to you.

Also, some locations require zoning approval, even for home-based businesses. Therefore, talk to your local city or county office if you’re unsure. Taking a little time now can help you avoid larger problems later.

When your business is registered, it sends a clear signal that you’re serious. It also sets the foundation for taxes, banking, and contracts. Make it one of your first steps.

Conclusion

Starting a business takes more than just an idea. You need to make thoughtful decisions and take practical steps to move forward. Each choice you make early on can affect how smoothly things go later. Therefore, take your time and ask questions along the way.

Understanding the business startup process helps you avoid common mistakes. It also makes it easier to plan, budget, and take action with confidence. Additionally, you’ll feel more prepared when challenges come up. Starting strong gives you a better chance to build something that lasts.

However, don’t feel pressured to get everything perfect. Most successful businesses make adjustments over time. Also, no one expects you to know everything on day one. You can learn as you go while staying focused on your goals. Therefore, stay flexible but stay committed.

Additionally, talk to other business owners when possible. Their feedback can help you make better decisions. Also, writing things down helps you stay organized and track your progress. These simple habits can make a big difference in how things turn out.

You don’t need a perfect plan, but you do need a clear one. Therefore, take what you’ve learned and put it into action. Focus on what matters and keep moving forward. Each step brings you closer to something real.

Starting a business is challenging, but it doesn’t have to be overwhelming. Keep your goals in mind and your process simple. With consistency and clarity, you’ll set yourself up for long-term success.